Every financial year based on your income, you need to pay income tax as well. By either choosing Old Tax Regime or New Tax Regime, we can calculate our income tax and pay accordingly while filing ITR (Income Tax Return) before the month of July every year. But do we have the liberty to save income tax? How to Save Tax if income is above Rs. 5 Lakhs. Let us understand this.

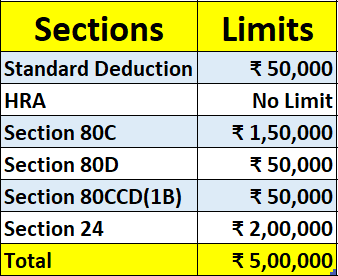

We can save tax if our income goes above Rs. 5 Lakhs in a financial year by using these tips – Standard Deduction (Rs. 50,000), HRA (House Rent Allowance), Section 80C (Rs. 1.5 Lakhs), Section 80D (Rs. 50,000), Section 80CCD(1B) (Rs. 50,000), Section 24 (Rs. 2 Lakhs). We can also claim HRA and Home loan deductions together if both the properties are in different cities.

How to Save Tax on Salary above 5 Lakhs Video

Watch more Videos on YouTube Channel

The options mentioned help you to save income tax based on Old Tax Regime. New Tax Regime does not allow these deductions to save income tax except Standard Deduction of Rs. 75,000.

Also, your aim must be to get your taxable income below Rs. 5 Lakhs in financial year, by making various investments. This will help you to get Tax Rebate under Section 87A to pay ZERO income tax. With new tax regime, taxable income up to Rs. 7 lakh will have zero income tax to be paid.

Let us understand all these options with their limits in financial year one at a time.

Standard Deduction

- Standard Deduction is a flat deductions of Rs. 50,000 – available for salaried employees and pensioners. For new tax regime, this limit is Rs. 75,000 for salaried employees

- You need to deduct this amount from your Gross Income to calculate Taxable income (on which income tax will be calculated)

- Formula to Calculate Taxable Income = Gross Income – Standard Deduction – Investments made for Deductions

- If this Taxable Income is below Rs. 5 Lakhs in financial year, you need not have to pay any tax based on Old Tax regime – using Tax Rebate under Section 87A

ALSO READ: How can I calculate my Income Tax [Examples]

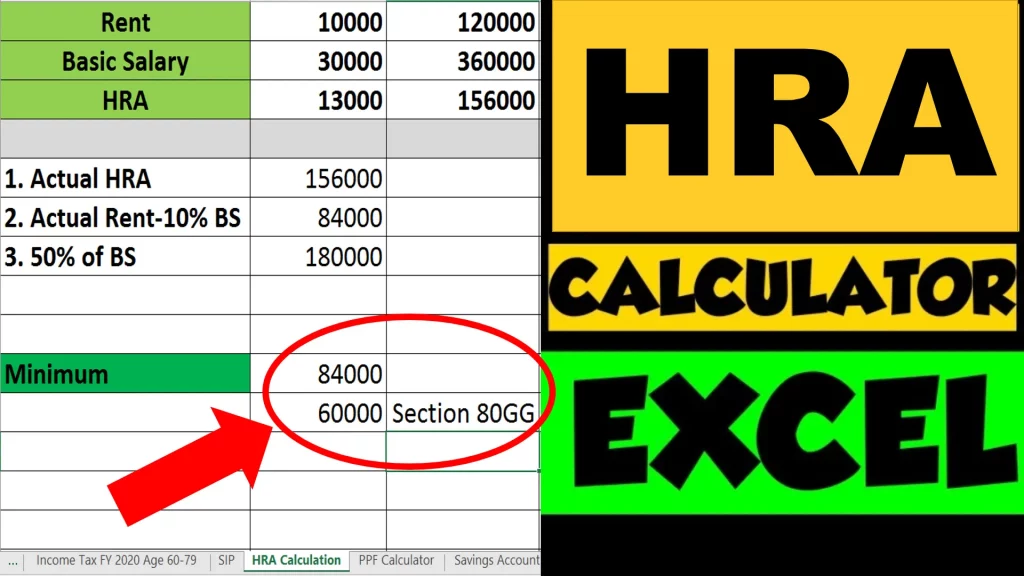

HRA – House Rent Allowance

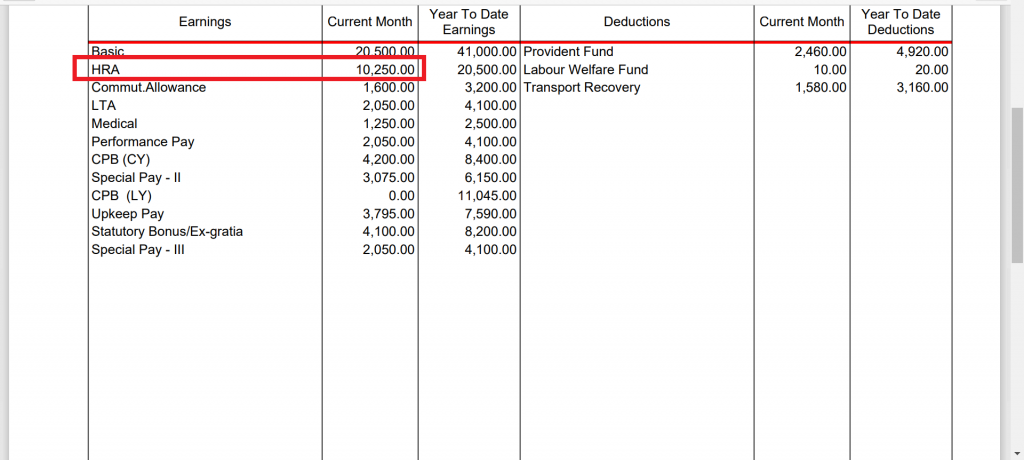

- HRA or House Rent allowance is the component of your Salary Payslip

- You can see the HRA component in below payslip example

- This HRA component is the allowance given to you to meet your house rent expenses

- In case you live in your own house and don’t stay on rent, you cannot claim this amount and this entire HRA amount in financial year becomes taxable.

- But if you live in rented accommodation, you can claim this HRA amount based on certain HRA calculations:

Minimum of below 3 calculations:

– Actual HRA amount received

– House Rent in FY minus 10% Basic Salary

– 40% Basic Salary (non metro city) or 50% Basic Salary (metro city) - Minimum amount from above mentioned calculations will be used for you to claim HRA.

- You can also use HRA calculator to calculate how much HRA you can claim in financial year.

ALSO READ: How HRA Exemption is Calculated [Examples]

Can we claim HRA without staying on Rent?

According to Income Tax Act, it is not specified that actually you need to stay on rent – but you should be transferring the rent amount every month and at least submit declaration to your employer that you stay on rent.

So this can help us paying rent to our parents and claim the same HRA if we had stayed on rent.

While paying rent to your parents and claiming HRA, there are certain things you must remember:

- The house must be in the name of your parent

- You should have the proof that you are actually paying the rent

- Submit declaration to your employer that you stay on rent and will be paying rent of specific amount every month for the entire financial year

Can we claim both HRA and Home Loan Deductions?

Yes, both HRA and home loan deductions can be claimed in a financial year, provided the rent you pay for the property and your own property for which you have taken loan are in different cities.

Love Reading Books? Here are some of the Best Books you can Read: (WITH LINKS)

Section 80C

- Section 80C is the popular section among tax payers to save income tax.

- Maximum Rs. 1.5 Lakhs can be claimed as deduction with Section 80C in a financial year

- The schemes include Employee provident fund, Public Provident Fund, Life Insurance Premiums, Equity Linked Saving Scheme (ELSS), 5 Year Fixed Deposits and many more.

- You can check the complete list of Section 80C deductions here.

Section 80D

- Section 80D is for claiming your medical insurance premiums

- If you have medical insurance and pay premiums every year, you can claim the amount under Section 80D

- For non senior citizens, the limit is Rs. 25,000 every year

- For senior citizens, the limit is Rs. 50,000 every year

- You can even have medical insurance for your parents and claim according to the limits mentioned based on the age groups

- Medical insurance premiums for self, spouse and children are also allowed to be claimed

ALSO READ: Deductions Allowed for Tax Payers

Section 80CCD(1B)

- Section 80CCD(1B) is for claiming your investments in NPS – National Pension Scheme

- It has the limit of claiming Rs. 50,000 in financial year when you invest in NPS. This limit is above and over Section 80C we have seen above

- You can easily open NPS account by watching this demo video

- NPS has two types of account – Tier 1 and Tier 2

- Tier 1 helps in saving for your retirement and is long term, which helps in tax saving as well

- Tier 2 is for short term and you can deposit your amount in this category for short term without any tax benefits

NPS Scheme Explained Video

Watch more Videos on YouTube Channel

Section 24

- Section 24 helps is claiming your home loan EMI interest component, that you pay every month

- While the principal component can be claimed under Section 80C with Rs. 1.5 Lakhs limit in financial year, interest component that you pay can be claimed under Section 24 with Rs. 2 Lakhs limit in financial year.

- You can easily download the Income Tax Certificate from your loan account, to get the details of how much principal and interest components you have paid for the entire financial year.

- There are other Home Loan Tax Benefits as well which you can read

- Just using the home loan for tax benefits and taking advantage of maximum limits of Section 24 is not wise. Remember you are paying the interest component to claim this amount, which will not come back to you

- So in case of thinking to take loan to claim such tax benefits is not the best option.

- If you already have home loan, you should be thinking to close it as soon as possible

- This can be done by making home loan prepayments, which will help you to close your home loan before time.

How to Save Tax on Salary of Rs. 10 Lakhs

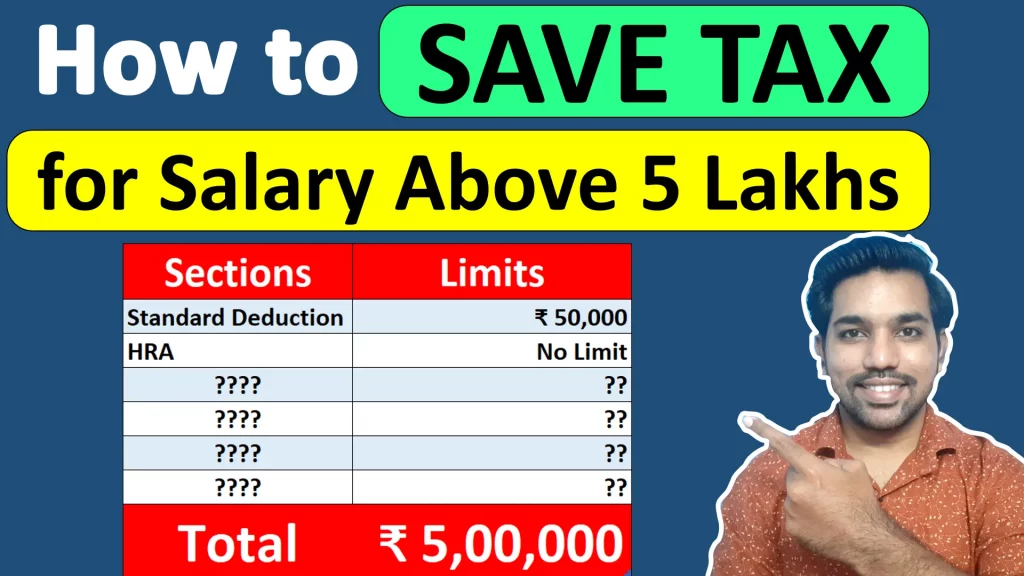

We have seen above options with their limits. If we add all the limits, it comes to Rs. 5 Lakhs, in which HRA is not included since it’s limit depends on your income and house rent amount you pay every month.

We have also considered Section 24 – home loan interest component, which might not be applicable to you if you don’t pay home loan EMIs. So you can replace this home loan interest component with HRA component by paying rent to your parents.

So considering Rs. 5 Lakhs as total deduction limit, according to old tax regime, your taxable income will be:

- Taxable Income = Gross Income – Deductions

- Taxable Income = Rs. 10,00,000 – Rs. 5,00,000

- Taxable Income = Rs. 5,00,000

And when your taxable income is Rs. 5 Lakhs or less, you get Tax Rebate under Section 87A, according to which you get rebate of Rs. 12,500. So tax on Rs. 5 Lakhs income is Rs. 12,500 (based on 5 % slab of old tax regime), which is cancelled by this tax rebate.

You can also use Income Tax Calculator to check you income tax on your income and investments.

Conclusion

So these are some of the options to save tax on salary. If someone asks you how to save tax on salary in a financial year when they have less time remaining to make investments (before march), you can share the below table with them:

Remember that these options are available only with Old Tax Regime. With new tax regime there are no deduction options available to save tax on your salary or income except standard deduction of Rs. 75,000.

So get your taxable income below Rs. 5 Lakhs with old tax regime or below 7 lakh with new tax regime in financial year and pay zero income tax.

Some more Reading:

- Important Facts about Income Tax Calculation

- Income Tax TDS Deduction Calculation on Salary

- Rs. 2000 SIP vs Step up SIP Returns Calculation

Save Home Loan Interest Amount!

Use Home Loan Excel Calculator that will help you to Save Interest Amount on Home Loan EMI.

Click below button to download Home Loan EMI and Prepayment Calculator in Excel:

Watch how Home Loan Calculator in Excel Works

Income Tax Calculator App – FinCalC

For Income Tax Calculation on your mobile device, you can Download my Android App “FinCalC” which I have developed for you to make your income tax calculation easy.

What you can do with this mobile App?

- Calculate Income Tax for FY 2025-26 and previous FY 2024-25

- Enter estimated Investments to check income tax with Old and New Tax Regime

- Save income tax details and track regularly

- Know how much to invest more to save income tax

- More calculators including PPF, SIP returns, Savings account interest and lot more

Use Popular Calculators:

- Income Tax Calculator

- Home Loan EMI Calculator

- SIP Calculator

- PPF Calculator

- HRA Calculator

- Step up SIP Calculator

- Savings Account Interest Calculator

- Lump sum Calculator

- FD Calculator

- RD Calculator

- Car Loan EMI Calculator

- Bike Loan EMI Calculator

- Sukanya Samriddhi Calculator

- Provident Fund Calculator

- Senior Citizen Savings Calculator

- NSC Calculator

- Monthly Income Scheme Calculator

- Mahila Samman Savings Calculator

- Systematic Withdrawal Calculator

- CAGR Calculator

I’d love to hear from you if you have any queries about Personal Finance and Money Management.

JOIN Telegram Group and stay updated with latest Personal Finance News and Topics.

Download our Free Android App – FinCalC to Calculate Income Tax and Interest on various small Saving Schemes in India including PPF, NSC, SIP and lot more.

Follow the Blog and Subscribe to YouTube Channel to stay updated about Personal Finance and Money Management topics.