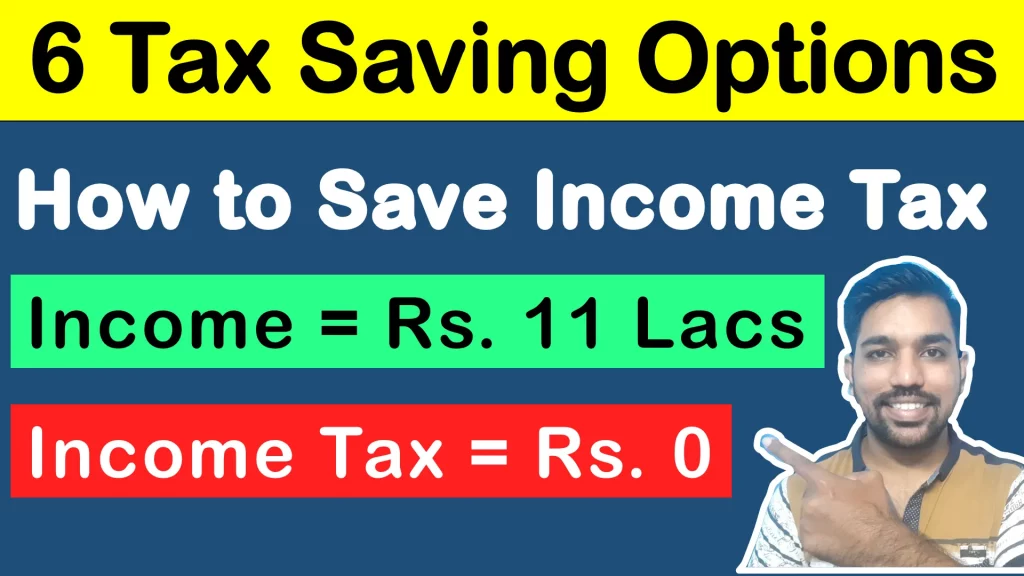

One of the most asked questions on internet is How to Save Income Tax in India? Whether a person is a salaried employee or a businessman, do we have enough options to save income tax for everyone? Let’s understand in this article.

You can Save Income Tax in India by making investments under some popular sections that will allow you to make deductions under Old Tax Regime. Top 6 Tax saving sections or options include Section 80C and sections other than 80C like Section 80CCD(1B), Standard Deduction, Section 10, Section 24 and Section 80D which we will see in detail. Overall, you DON’T have to pay any income tax on income up to Rs. 12 lakh in a financial year if you use maximum limits under these deduction sections.

Remember, you need to get your taxable income below Rs. 5 lakh to pay Zero Income Tax with the help of Tax Rebate u/s 87A of Rs. 12,500. The investments you have to make to reduce your taxable income is allowed only in Old Tax Regime.

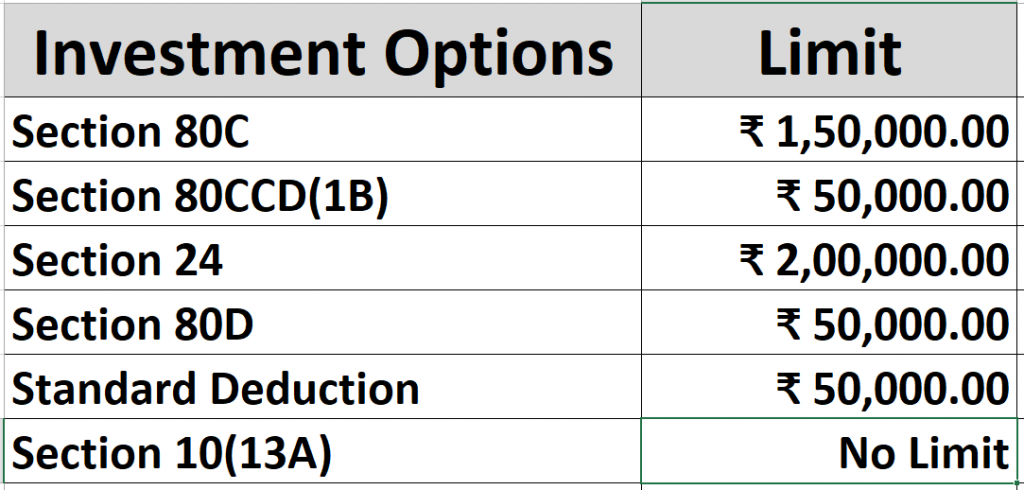

Below is the summary of various sections with limits:

How to Save Income Tax in India Video

There are various options to Save Income Tax in India including Section 80C, Section 80CCD(1B), Section 10 (13A), Section 80D, Section 24 and Standard Deduction (applicable to Employees and Pensioners)

Let’s see all these sections one by one.

Section 80C

Maximum Limit in Financial Year: Rs. 1,50,000

Section 80C is one of the popular sections to save Income Tax in India that includes various schemes such as Employee Provident Fund, Public Provident Fund, 5 Year Fixed Deposits, ELSS in Mutual Funds, home loan principal repayment, Life insurance premiums, etc.

Section 80C provides you maximum deduction of Rs. 1,50,000 in order to save your income tax in a financial year. Also, these deductions are only applicable when you choose old tax regime to calculate your income tax. That means these deductions are not allowed in new tax regime.

Below are some details about these schemes:

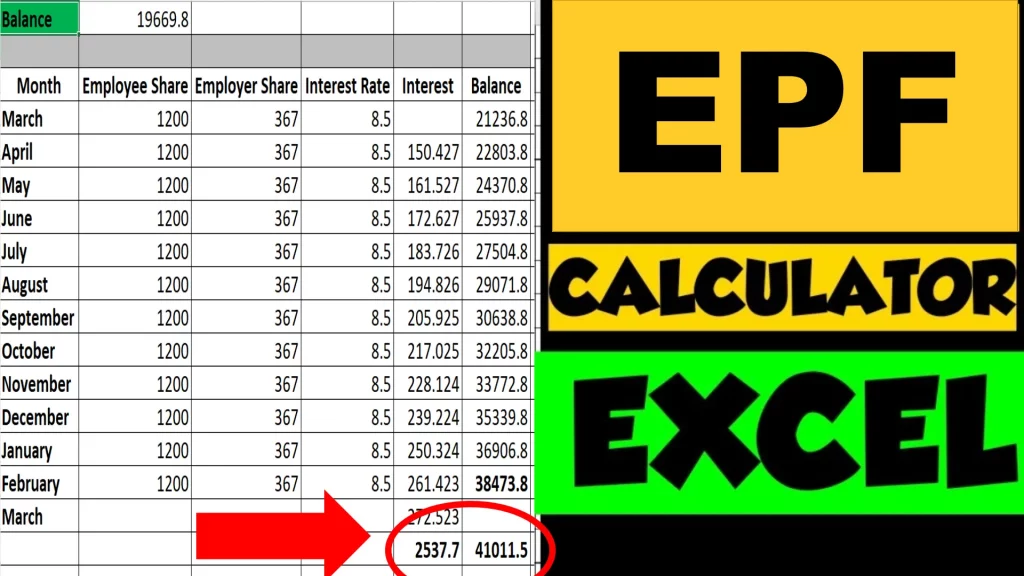

Employee Provident Fund (EPF)

The Employees Provident Fund (EPF) is a savings scheme introduced under the Employees Provident Fund and Miscellaneous Act, 1952. It is administered and managed by the Central Board of Trustees that consists of representatives from three parties, namely, the government, the employers and the employees.

The Employees Provident Fund Organization (EPFO) assists this board in its activities. EPFO works under the direct jurisdiction of the government and is managed through the Ministry of Labor and Employment.

EPF scheme aims at promoting savings to be used post-retirement by various employees all over the country. Employees Provident Fund or EPF is a collection of funds contributed by the employer and their employee regularly on a monthly basis. The employer and employee contribute 12% each of the employee’s salary (basic + dearness allowance) to the EPF. These contributions earn a fixed level of interest set by the EPFO. The amount of interest to be received on the deposit along with the total accumulated amount is totally tax-free, i.e. the employee may withdraw the entire fund without worrying about paying any kind of tax on it, if total years of service is more than 5 years.

The accrued amount may also be withdrawn by the nominee or the legal heir of the employee post his death or can be withdrawn by the employee himself post-resignation.

Dearness Allowance: This amount is added to the employee’s basic salary due to rising. This allowance is different in different states. It is a relief given to employees to tackle ill-effects of inflation.

DOWNLOAD EPF INTEREST EXCEL CALCULATOR

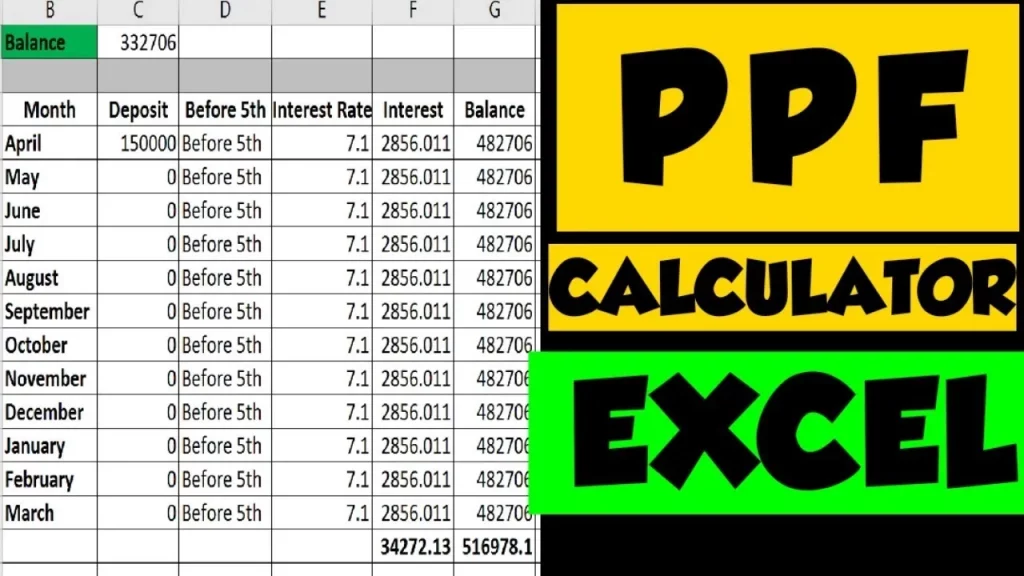

Public Provident Fund (PPF)

- PPF or Public Provident Fund is a savings scheme offered by the Government of India

- PPF has a lock-in period of 15 years

- Minimum deposit amount in a FY to keep your PPF account active is Rs. 500

- Maximum deposit amount for which you can earn interest in PPF account is Rs. 1,50,000

- The interest on the account is paid by the government of India and is set every quarter. PPF Interest amount is also tax-free

- PPF interest is calculated every month and is compounded annually

- The applicable PPF interest rate for October to December 2021, has been fixed at 7.1% annually

- PPF or Public Provident Fund falls under EEE category (Exempt, Exempt, Exempt), which means, the Deposits, Interest and Maturity Amounts are all exempted from Income Tax

- Partial withdrawals are allowed in PPF account

- Loan facility is also available in PPF account

You can read more about Public Provident Fund here.

DOWNLOAD PPF EXCEL CALCULATOR

5 year Fixed Deposits

- Fixed Deposit (FD) is also called as Time Deposit, is a type of Deposit that helps you prepare for your future goals

- You deposit a principal amount decided by you and you receive quarterly interest which is paid to you after FD maturity in case of cumulative FD, or your receive regular payouts in case of non-cumulative FD

- Fixed deposits have higher interest rates compared to Savings or Recurring Deposits interest rates

- Higher interest rates makes FD more attractive

Read more about Fixed Deposits here.

DOWNLOAD FIXED DEPOSIT EXCEL CALCULATOR

Apart from these, you can use Life insurance premiums and Home Loan repayments as deductions to Save Income Tax in India.

Love Reading Books? Here are some of the Best Books you can Read: (WITH LINKS)

Section 80CCD(1B)

Maximum Limit in Financial Year: Rs. 50,000

Section 80CCD(1B) includes NPS which is National Pension Scheme as the scheme that offers additional Rs. 50,000 as maximum deduction under old tax regime.

You can easily open NPS account online and start contributing towards your pension plan easily.

NPS online contribution Demo Video

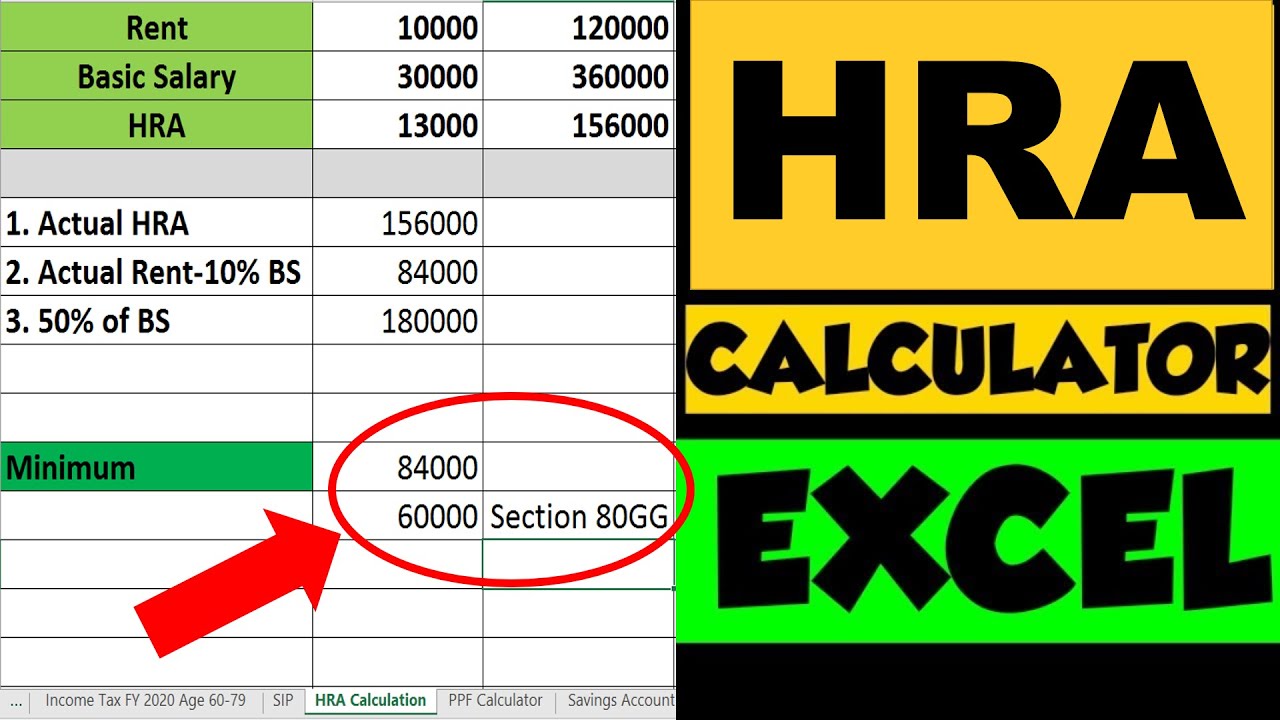

Section 10 (13A)

Maximum Limit in Financial Year: Depends on Basic Salary and HRA component

Section 10 (13A) includes HRA exemption deduction that helps in saving income tax. The HRA component you receive in your salary in each financial year is taxable, which can be claimed if you are staying on rent.

You need to provide rent receipts and must have online transactions of rent payments to claim HRA exemption in case rent is above Rs. 1 lac in a Financial Year.

Things to know about HRA

- HRA exemption limit is calculated based on your Basic Salary, HRA component and the rent you pay (calculations below)

- HRA exemption in new tax regime is not allowed since new tax regime contains reduced Tax slab rates. No deductions are allowed in new tax regime

- To claim HRA, PAN card of landlord is required only when you pay a total rent of more than Rs. 1 Lac in a Financial Year.

- HRA exemption without PAN is applicable only when total rent paid in FY is less than Rs. 1 Lac, or monthly rent paid is less than Rs. 8,333

- HRA exemption section is Section 10 (13a)

- HRA exemption without rent receipt is not possible since rent receipt are the proof that you pay rent. It is better to ask landlord to provide you rent receipt

- HRA exemption without HRA component in salary is also possible if you claim deduction under Section 80GG

- Remember, HRA exemption can be claimed only under Old Tax regime. HRA exemption under New Tax Regime is not allowed

You can read more about HRA exemption here.

HRA exemption Calculator Video

DOWNLOAD HRA EXEMPTION EXCEL CALCULATOR

Section 80D

Maximum Limit in Financial Year: Rs. 50,000

Section 80D includes medical insurance that you pay in a financial year. You can claim the medical insurance premiums paid to insure yourself, spouse, children and parents as deductions in old tax regime.

The limits are based on age groups. If your age is below 60 years (non senior citizens) than you get maximum Rs. 25,000 as deduction and another Rs. 25,000 for your non senior citizens parents.

In case of senior citizens, the maximum limit reaches to Rs. 1,00,000 (Rs. 50,000 for self, family and Rs. 50,000 for parents)

Section 24

Maximum Limit in Financial Year: Rs. 2,00,000

Section 24 includes the home loan interest component paid by you in the financial year when you take a housing loan. The home loan principal repayment is covered in Section 80C whereas the home loan interest component is covered in this Section 24.

You can also know how home loan EMI is calculated with principal and interest components here.

Also, in case you want to reduce the home loan interest to be paid by you, you can make loan prepayments to save home loan interest. It is better to reduce loan tenure compared to loan EMI due to reasons mentioned in this home loan prepayment article.

Home Loan Prepayment Video

DOWNLOAD HOME LOAN EMI CALCULATOR

Standard Deduction

Maximum limit: Rs. 50,000

This is a flat deduction available to only employees and pensioners. This deduction is applied on gross income to calculate taxable income apart from the other investment options mentioned above in this article.

How to Calculate Taxable Income Video

Conclusion

Above mentioned sections are some of the popular sections we can use to save income tax. It is very important to plan your investments and take decisions accordingly to choose between old tax regime or new tax regime.

Old tax regime allows you to save income tax with the help of deductions you can claim, where as new tax regime contains minimum number of deductions along with reduced tax slab rates.

Some more Reading:

- Income Tax Calculation Examples

- Deductions And Exemptions Allowed in New Tax Regime

- Rs. 2000 PPF Interest Calculation for 15 Years

Save Home Loan Interest Amount!

Use Home Loan Excel Calculator that will help you to Save Interest Amount on Home Loan EMI.

Click below button to download Home Loan EMI and Prepayment Calculator in Excel:

Watch how Home Loan Calculator in Excel Works

Income Tax Calculator App – FinCalC

For Income Tax Calculation on your mobile device, you can Download my Android App “FinCalC” which I have developed for you to make your income tax calculation easy.

What you can do with this mobile App?

- Calculate Income Tax for FY 2025-26 and previous FY 2024-25

- Enter estimated Investments to check income tax with Old and New Tax Regime

- Save income tax details and track regularly

- Know how much to invest more to save income tax

- More calculators including PPF, SIP returns, Savings account interest and lot more

Use Popular Calculators:

- Income Tax Calculator

- Home Loan EMI Calculator

- SIP Calculator

- PPF Calculator

- HRA Calculator

- Step up SIP Calculator

- Savings Account Interest Calculator

- Lump sum Calculator

- FD Calculator

- RD Calculator

- Car Loan EMI Calculator

- Bike Loan EMI Calculator

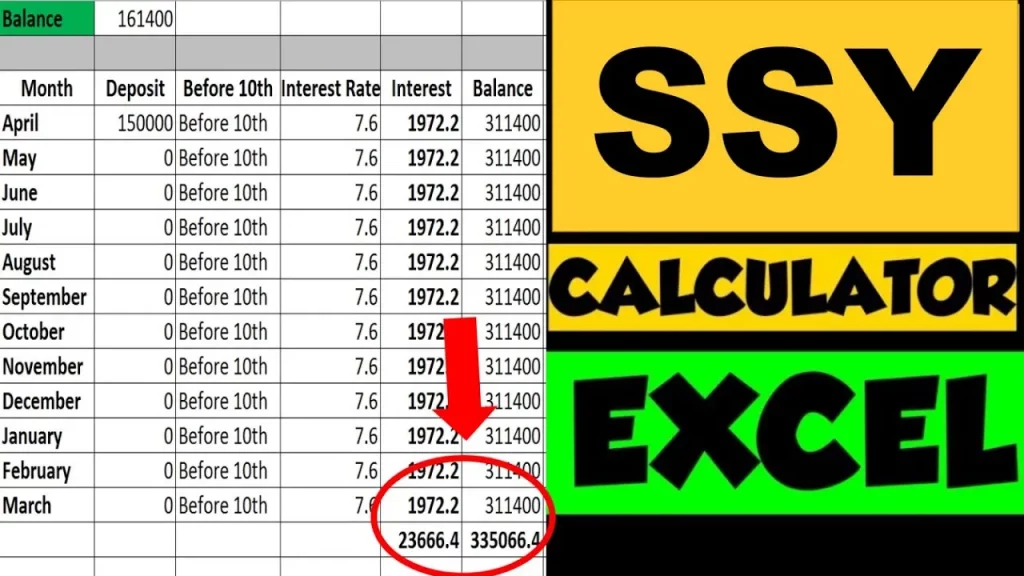

- Sukanya Samriddhi Calculator

- Provident Fund Calculator

- Senior Citizen Savings Calculator

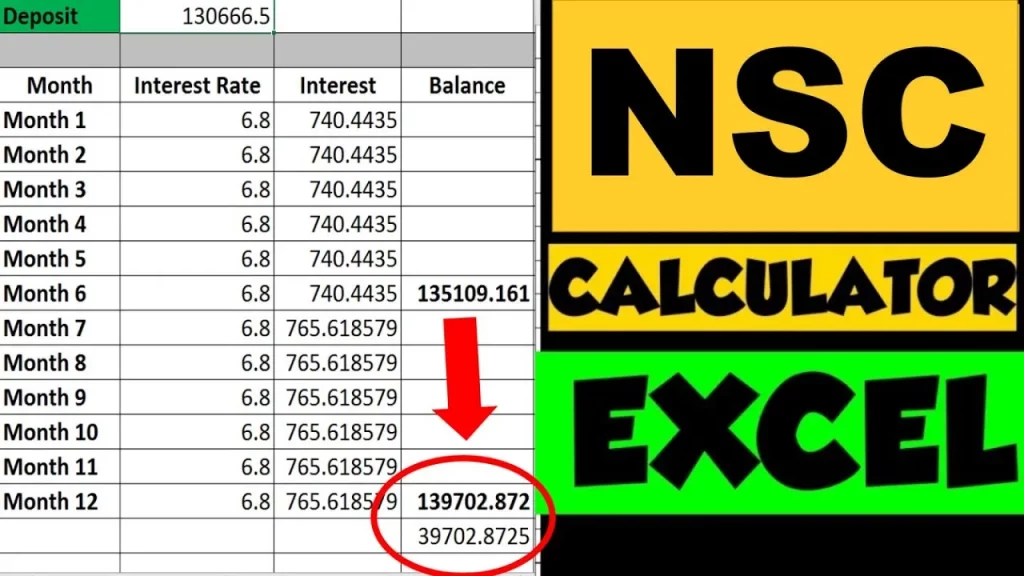

- NSC Calculator

- Monthly Income Scheme Calculator

- Mahila Samman Savings Calculator

- Systematic Withdrawal Calculator

- CAGR Calculator

I’d love to hear from you if you have any queries about Personal Finance and Money Management.

JOIN Telegram Group and stay updated with latest Personal Finance News and Topics.

Download our Free Android App – FinCalC to Calculate Income Tax and Interest on various small Saving Schemes in India including PPF, NSC, SIP and lot more.

Follow the Blog and Subscribe to YouTube Channel to stay updated about Personal Finance and Money Management topics.