As we are in financial year 2025-26, many Indians look to optimize tax savings while growing their wealth. With options ranging from ELSS and PPF to NPS, health insurance, and more, understanding which tools work best for your financial goals can be overwhelming. We also need to look the old tax regime and new tax regime while making investments and saving income tax. In this fully updated guide for Best Tax-Saving Investments for FY 2025–26, you’ll understand various options to save income tax using old and new tax regime.

- Understanding the Tax Landscape & FY 2025-26 Key Updates

- New Tax Regime – No Tax up to 16 Lakh Video

- New Tax Regime Investment Options to Save Income Tax

- Section 80C Investments (Up to ₹1.5 Lakh)

- Section 80CCD(1B), 80CCD(2) — NPS for Retirement & Extra Deduction

- Section 80D & Other Deductions (Beyond 80C)

- Side-by-Side Comparison Table of All Investments

- Sample Portfolios Based on Age & Risk Profile

- Case Study: ₹10 Lakh Salary—Maximizing ₹2.25 L Deduction

- Frequently Asked Questions

- Conclusion

Understanding the Tax Landscape & FY 2025-26 Key Updates

- New Regime now offers zero income tax up to ₹12 lakh/year income. Yet investment still adds value beyond tax-saving — for wealth, security, retirement.

- TDS limits doubled on interest for senior citizens (₹1 lakh from previous ₹50 k) — relevant for FD, SCSS investors.

- Budget extended time limit for ITR corrections to 4 years — helpful to update tax planning retrospectives.

New Tax Regime – No Tax up to 16 Lakh Video

Watch more Videos on YouTube Channel

New Tax Regime Investment Options to Save Income Tax

Before moving towards the list of Investment options, we will see which of them and other deductions will be allowed in new tax regime, since new regime is the one with low tax slab rates:

- Standard Deduction of Rs. 75,000 available for salaried employees

- Deduction for employer’s contribution in NPS Account under Section 80CCD(2)

- Home Loan Interest amount under Section 24 in case of let-out property

- Deduction of amount paid or deposited in Agniveer Corpus Fund under Section 80CCH(2)

- Transport allowance can be claimed in case of specially-abled person

- Conveyance allowance for employees received to meet conveyance expenditures

- Compensation received for cost of travel or tour

- Daily Allowance received as compensation for cost of living in some other place compared to regular place of working

- Gifts up to Rs. 5000

- Exemption on voluntary retirement 10(10C), gratuity u/s 10(10) and Leave encashment u/s 10(10AA)

Above are the options available to save income tax with new tax regime, no other deductions are applicable when you select new tax regime.

Let us now discuss the list of Investment options mostly available with old tax regime.

Section 80C Investments (Up to ₹1.5 Lakh)

🟢 ELSS (Equity Linked Savings Scheme)

- Lock-in: 3 years (shortest under 80C), great liquidity

- Returns: Historically 10–15% p.a. – potential to beat inflation if held for long term

- Tax treatment: Long Term Capital Gains (LTCG) above ₹1.25 lakh taxed at 12.5%

- Pros: Highest growth potential, SIP or lump-sum flexibility

- Cons: Market risk, not ideal for risk-averse investors

- Tip: Beginning-of-year investing avoids last-minute rush Jan–Mar crowding

🟢 PPF (Public Provident Fund)

- Lock-in: 15 years (extendable)

- Returns: 7.1% compounding annually; fully tax-exempt (EEE)

- Pros: Government-backed safety, partial withdrawals from year 7, loan facility available

- Cons: Long lock-in, low returns compared to equities

🟢 NSC (National Savings Certificate)

- Lock-in: 5 years

- Returns: 7.7%; interest is taxable but eligible under 80C if reinvested

- Pros: Government guarantee, ideal for conservative investors

- Cons: No liquidity, TDS on interest

🟢 Tax-Saver Fixed Deposits (FDs)

- Lock-in: 5 years

- Returns: ~6–9%; senior citizen small finance banks may offer up to 9.1% (e.g., Suryoday SFB)

- Pros: Fixed return, simple, low risk

- Cons: Interest taxable; inflation may reduce real return

🟢 SCSS (Senior Citizen Savings Scheme)

- Eligibility: Age ≥ 60 years

- Lock-in: 5 years (extendable)

- Returns: 8.2% p.a.; quarterly payout

- Pros: Excellent for post-retirement income, safe, government-backed

- Cons: Interest above ₹1 lakh taxable; cap ₹30 lakh investment

🟢 Sukanya Samriddhi Yojana (SSY)

- Eligibility: Girl child <10 years

- Lock-in: Until daughter turns 21 or marries (after 18)

- Returns: 8.2%, tax-exempt (EEE)

- Pros: Safe for long-term goals like higher education or marriage

- Cons: Long horizon, specific to daughters

🟢 EPF (Employees’ Provident Fund)

- Mandatory: 12% of basic salary contribution by employee + employer

- Returns: 8–8.5% (tax-free if >5-year tenure)

- Pros: Automatic deduction, employer contribution counts under 80C

- Cons: Only for salaried employees, lower liquidity before retirement

🟢 ULIPs (Unit Linked Insurance Plans)

- Lock-in: 5 years

- Returns: Market-linked; partial switching allowed

- Tax: Death benefit & maturity exempt under Sec 10(10D) if norms met

- Pros: Combines life cover + investment flexibility

- Cons: High charges; returns depend on market; complex structure

🟢 Life Insurance Premiums

- Use-case: Essential for risk coverage; combine term plans with separate investments for clarity

🟢 Education Fees & Tuition (for up to 2 children)

- Tax Benefit: Deduction under 80C for tuition fees of full-time education in India

- Note: Only tuition; not uniforms, books, transport

Section 80CCD(1B), 80CCD(2) — NPS for Retirement & Extra Deduction

🟢 National Pension System (NPS)

- Section 80CCD(1): Part of ₹1.5 L limit

- Section 80CCD(1B): Additional ₹50,000 deduction—exclusive only to NPS

- Section 80CCD(2): Employer contributions (10–14% salary) are also deductible (exempt even under new regime)

- Returns: Market-linked; approx. 8–12% p.a. depending on equity/debt mix; 60% corpus withdrawal tax-free, annuity for rest

- Pros: Great for long-term retirement, tax deduction, flexibility in investment allocation

- Cons: Locked until age 60; annuity rules

Section 80D & Other Deductions (Beyond 80C)

🟢 Health Insurance (Section 80D)

- Up to ₹25,000 for self + family

- Additional ₹25,000 for parents <60; ₹50,000 if parents ≥60

- Tip: Buy before March 31 for FY benefit

🟢 Home Loan Interest & Principal

- Principal: Under 80C (up to ₹1.5 lakh)

- Interest: Section 24(b) up to ₹2 lakh (self-occupied); extra ₹50k under 80EE/80EEA for first-time buyers

🟢 Education Loan Interest (Section 80E)

- Deduction for interest paid; no upper limit; valid for 8 years

🟢 House Rent Allowance (HRA, Sec 10(13A))

- Deduction based on rent paid vs salary components; especially useful for those living in rented accommodation

🟢 Interest on Savings (80TTA / 80TTB)

- 80TTA: Deduction up to ₹10,000 on interest from savings accounts for non-senior citizens

- 80TTB: Up to ₹50,000 for senior citizens (includes deposit interest)

🟢 Donations & Disability Relief

- 80G: Donations to approved charities (50% or 100%)

- 80DD/80DDB/U: Deduction for mental disability (up to ₹75k or ₹1.25L), specified illnesses, general disability

🟢 HUF Structure

- HUF (Hindu Undivided Family) income and investments are taxed separately; can be leveraged for tax efficiency in families with ancestral property/assets

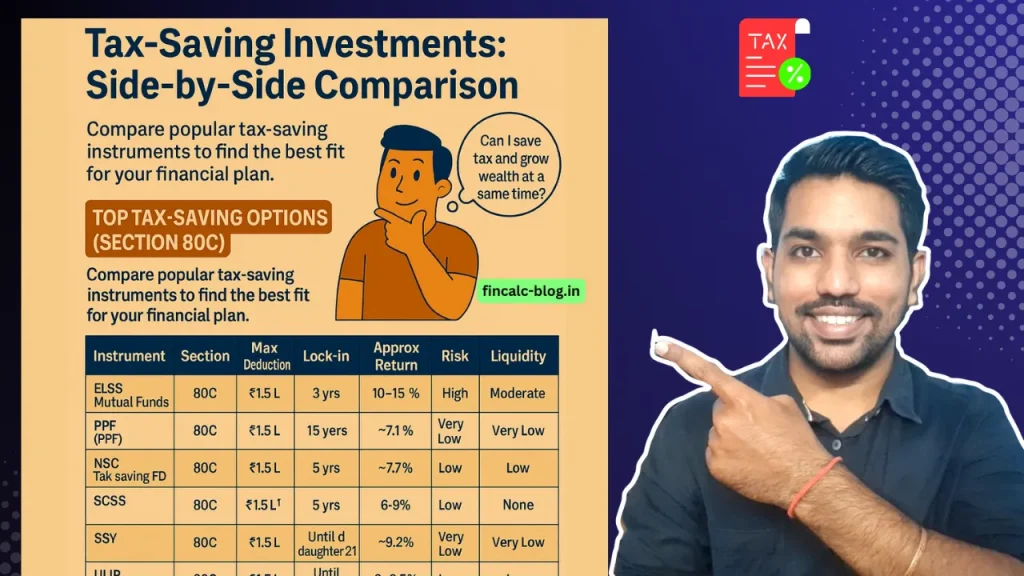

Side-by-Side Comparison Table of All Investments

| Instrument | Section | Max Deduction | Lock-in | Approx Return | Risk | Liquidity |

|---|---|---|---|---|---|---|

| ELSS | 80C | ₹1.5L | 3 yrs | 10–15% p.a. | High | Moderate |

| PPF | 80C | ₹1.5L | 15 yrs | ~7.1% | Very Low | Very Low |

| NSC | 80C | ₹1.5L | 5 yrs | ~7.7% | Low | Low |

| Tax-saving FD | 80C | ₹1.5L | 5 yrs | 6–9% | Low | None |

| SCSS | 80C | ₹1.5L¹ | 5 yrs | ~8.2% | Very Low | Low |

| SSY | 80C | ₹1.5L | Until daughter 21 | ~8.2% | Very Low | Very Low |

| EPF | 80C | ₹1.5L | Until retirement | ~8–8.5% | Low | Low |

| ULIP | 80C | ₹1.5L | 5 yrs | Market-linked | Moderate–High | Low |

| Life Insurance | 80C / 10(10D) | ₹1.5L | – | – | Low | N/A |

| NPS | 80CCD(1B) | ₹2L total | Until 60 yrs | ~8–12% | Moderate | None |

| Health Insurance | 80D | ₹25–₹75k | Annual | N/A | N/A | N/A |

| Home Loan (interest) | 24(b)/80C/80EE | ₹2.5L total | Varies | N/A | N/A | N/A |

SCSS deductible under 80C within existing ₹1.5 L limit; max ₹30 L total investment can be made

Sample Portfolios Based on Age & Risk Profile

👶 Young (20–35 yrs), High Growth

- ELSS ₹1.0L via SIP (80C)

- NPS Tier I ₹50k (80CCD(1B))

- Budget health insurance ₹15k (80D)

- EPF contributions auto deduction

Why: High equity exposure, early compounding, retirement cushion

👨👩👧 Middle-aged (35–55 yrs), Moderate Growth + Safety

- ELSS ₹50k + PPF ₹50k (80C)

- NPS ₹50k

- Health insurance ₹25k + parents ₹25k (80D)

- Home loan interest claim ₹2L (if applicable)

Why: Balanced risk, mid/long-term planning, family protection

👵 Senior Citizens (55+ yrs), Low Risk + Income

- SCSS ₹15L

- PPF ₹1.5L (if still eligible)

- NPS ₹50k (if not locked earlier)

- Health insurance ₹50k (self + parents)

- Tax-saving FD ₹2L

Why: Income, tax efficiency, low risk, liquidity for medical

Case Study: ₹10 Lakh Salary—Maximizing ₹2.25 L Deduction

Scenario: Salaried person, age ~30, ₹10 L annual income, wants ₹2.25 L deduction

- ELSS via SIP ₹80k → growth potential (+ tax saving)

- PPF ₹50k → safe long-term reserve

- NPS ₹50k → extra ₹50k deduction

- Health insurance ₹15k → covers self + family

- Employer EPF ₹1.2 L included, interest tax-free

- Result: ₹1.85 L under 80C+80CCD + ₹15k under 80D → ~₹2 L deductions

Tax saved: ~₹60k–₹70k depending on slab; plus long-term wealth building. With new tax regime, no income tax to be paid without any investments.

Frequently Asked Questions

Q1. What’s the best tax-saving investment for FY 2025-26?

Answer: Depends on your profile. ELSS for maximum growth, PPF or SCSS for safety, NPS for retirement + extra ₹50k deduction.

Q2. Can I invest in multiple instruments and still claim full ₹1.5 L?

Yes—you can split across PPF, ELSS, NSC, FD, ULIPs, SSY, EPF, etc., up to ₹1.5 L combined under 80C.

Q3. Should I switch to new tax regime?

Even under new regime (No Tax up to ₹12 L), investing in NPS, PPF, health insurance, and retirement tools still adds wealth & protection even without deduction—don’t drop proven tools if you can afford to invest.

Q4. When should I invest to maximize returns?

Start early (April–June) to benefit from rupee-cost averaging, market cycles, and avoid Q4 rush.

Q5. What happens to PPF after 15 years?

You can withdraw fully or extend in 5-year blocks. Loans allowed after year 3, partial withdrawal after year 7.

Q6. How to choose between SCSS vs FD for seniors?

SCSS offers ~8.2% (govt-backed) vs FD up to 7.5%; choose based on liquidity and comfort with small-bank deposits.

Conclusion

- Fully utilize ₹1.5 L under Section 80C with a smart mix suited to your risk & goals

- Add NPS ₹50k extra for retirement & additional deductions

- Secure health insurance—tax benefit + family protection

- Combine instruments—ELSS for growth, PPF/SCSS for safety, ULIP/life-insurance for cover

- Plan early, not only in March—rupee-cost averaging matters

Some more Reading:

- How to Pay Off 25 Year Loan in 10 Years

- Types of Mutual Funds in India

- 4 Signs that you are Doing Well Financially

Save Home Loan Interest Amount!

Use Home Loan Excel Calculator that will help you to Save Interest Amount on Home Loan EMI.

Click below button to download Home Loan EMI and Prepayment Calculator in Excel:

Watch how Home Loan Calculator in Excel Works

Income Tax Calculator App – FinCalC

For Income Tax Calculation on your mobile device, you can Download my Android App “FinCalC” which I have developed for you to make your income tax calculation easy.

What you can do with this mobile App?

- Calculate Income Tax for FY 2025-26 and previous FY 2024-25

- Enter estimated Investments to check income tax with Old and New Tax Regime

- Save income tax details and track regularly

- Know how much to invest more to save income tax

- More calculators including PPF, SIP returns, Savings account interest and lot more

Use Popular Calculators:

- Income Tax Calculator

- Home Loan EMI Calculator

- SIP Calculator

- PPF Calculator

- HRA Calculator

- Step up SIP Calculator

- Savings Account Interest Calculator

- Lump sum Calculator

- FD Calculator

- RD Calculator

- Car Loan EMI Calculator

- Bike Loan EMI Calculator

- Sukanya Samriddhi Calculator

- Provident Fund Calculator

- Senior Citizen Savings Calculator

- NSC Calculator

- Monthly Income Scheme Calculator

- Mahila Samman Savings Calculator

- Systematic Withdrawal Calculator

- CAGR Calculator

I’d love to hear from you if you have any queries about Personal Finance and Money Management.

JOIN Telegram Group and stay updated with latest Personal Finance News and Topics.

Download our Free Android App – FinCalC to Calculate Income Tax and Interest on various small Saving Schemes in India including PPF, NSC, SIP and lot more.

Follow the Blog and Subscribe to YouTube Channel to stay updated about Personal Finance and Money Management topics.