Do you have a life Insurance? If you are the only bread earner, it’s important for you to have a life insurance to cover your family with financial stability after any mishap with you. This will help your family members to pay back the loan amount taken or as a source of regular income for them. We will see the types of life insurance in this post that you can select from.

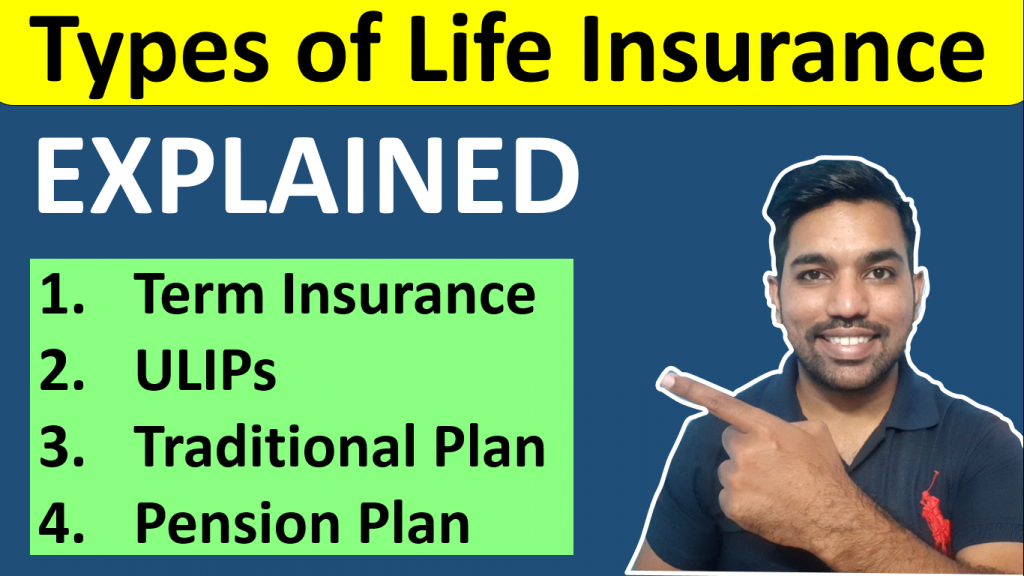

The 4 Types of Life Insurance include Term Life insurance, Unit Linked Insurance Plan (ULIP), Traditional Insurance Plan and Pension Insurance Plans. Out of all these, term life insurance plan is the pure insurance plan you can buy to have maximum sum assured benefit and minimum premium payment to be paid.

Let us discuss each of them in detail.

Term Insurance

- Term Insurance is a type of Life Insurance plan that provides financial assistance to family members after sudden death of the bread earner

- If you have a liability like home loan, car loan or any other loans, term insurance helps the family members of deceased to pay back the remaining debts

- This helps in financial support for the non earning family members

There are 2 types of Term Insurance you can buy:

1. With return of premium:

- However, the one feature that sets it apart from the regular term insurance plans is the survival benefit.

- Some other add-on benefits associated with this plan include disability benefit, accidental death benefit, and protection against critical illness.

2. Without return of premium:

- Term plans are pure life insurance products that offer life coverage for a specified tenure or term.

- In the event of the policyholder’s unfortunate demise during the policy term, the nominee receives the sum assured payout.

- Term plans enable policyholders to secure their family’s financial future.

Watch below video to know more about income tax saving options:

Watch more Videos on YouTube Channel

Unit Linked Insurance Plans (ULIP)

ULIP is a type of life insurance plan which provides you benefit of growth of your investment amount along with life cover option.

This happens by way of investing part of your invested amount under life insurance option and remaining under funds which provides Market growth which an investor can choose based on his/her risk taking ability.

- Investor will not be ask to pay any tax subject to conditions of section 10(10d) on maturity benefits received .

- ULIP generally has a lock in period in which investor cannot break the investment and if investor wishes to surrender will have to bear the penalty and chargers.

- ULIP helps you to finance your long term goals like taking your dream house, children higher abroad education, marriage etc.

- It is necessary to remain invested for long time duration to get higher returns.

- It also offers you flexible options of investing in high, medium and low risk investment options via different funds available in same plan.

- ULIPs are also used to provide payouts to their beneficiaries following their uncertain death.

Use Income Tax Calculator:

Advantages of ULIP:

- ULIPs provide both investment and insurance benefits

- In ULIP amount is invested in equity, debt, or a combination of both

- ULIP helps in building wealth over long term.

- Depending upon the market situation and investors investment objective and goals, ULIP provides an option to switch between funds within same plan and as a result, investors can switch funds without terminating their insurance plans and with no fees and charges.

- The investments under ULIP plans are completely managed by dedicated fund managers which are appointed by the respective insurance company. Thus, there is no need to track the investments on your own.

Disadvantages of ULIP:

- Although ULIP give high return, high flexibility it does have certain disadvantages unlike fund management charges, fund allocation charges, mortality charges , policy administration charges are among high with ULIP plans.

- Returns are totally based on market performance hence no assurance of returns.

- Investor cannot touch invested amount or withdraw before lock in period is over .in case he/ she wishes to withdraw, have to pay exist fees and charges.

ALSO READ: Mutual Fund Returns Calculator for 10 Years

Traditional or Guaranteed Insurance Plans

- Traditional life insurance plan is another investment options with guaranteed maturity.

- It provides sum assured and guaranteed amount along with bonus( If declared by company) at an the time of maturity to policy holder.

- It has various options like money back , whole life, endowment insurance options with risk cover, high income return, safety of principal amount invested and tax benefits.

- Traditional insurance plans are considered risk-free because it offers fixed returns in case of death or maturity .

- Another advantage of investing in traditional or guaranteed plan is that in these plans very limited portion of investors amount is invested in equity market and hence probability of loosing principal amount is very low.

- Unlike ULIP, premature withdrawal is normally not allowed in the case of traditional insurance plans. in case policy is surrendered then policy holder needs to pay surrender charges.

- Unlike ULIP, policy holder does not have options to switch funds within plan.

ALSO READ: Rs. 1000 SIP Returns Calculation for 15 Years

Benefits of Traditional Insurance Plan:

Maturity return benefits

In traditional insurance plans investor receives lump sum amount at the time of maturity basis amount invested by him/her in form of premium .

Income tax benefits

The premiums paid for the traditional policy are eligible for tax deductions of up to Rs 1.5 lakh per annum under Section 80C of the Income Tax Act and at the same time maturity/ death benefit are exempted from tax under sec 10(10d).

Death benefit

Death benefit is the amount of claim paid to the nominee/beneficiary under the life insurance policy after the life insured passes within the policy term. It is the lump sum amount that a nominee receives when the life insured dies within the policy period.

The amount received can be used for paying off any unpaid debts and liabilities. It can also be used by the family members to continue manage their lifestyle expenses. The important benefit is that the death benefit received by nominee is totally exempted from tax.

Additional rider cover

In Traditional insurance plan investor can take additional riders like Accidental rider, critical illness, permanent disability rider etc. It helps to increase total protection pool.

Riders are additional benefits that can be bought and can be added to a basic life insurance policy.

Risk free investment

Amount invested in traditional insurance plan are risk free because an investors already have an idea of how much amount he/she will receive and when. It helps investor to plan their future in a better way. this type of investment are called as risk free investment because risk is completely borne by insurance company.

Guaranteed benefits

Traditional Insurance Plans offers guaranteed return benefits hence no risk or tension to investors to loose his / her capital invested.

Types of Traditional Life insurance plan:

Money back:

- A Money back investment plan is offered by an insurance company that pays pre- determined% of sum assured to the investor or policy holder at specific interval of time which is called as survival benefits. An investor can use these survival benefits to meet his/ her various financial goals.

- Money back insurance plans offers the policyholder the dual benefit of life coverage and regular cash inflows.

Whole Life:

- Whole life insurance gives an investor a life cover for a lifetime (up to 100 years of age in some policies). In case of the demise of the policyholder, the nominee receives a death benefit along with bonuses, if any declared by insurance company.

- If the life assured dies before the age of 100 years, the nominee receives the sum assured. However, if the life assured survives after the age of 100 years, the insurance company pays the matured endowment coverage to the life insured.

Endowment Insurance Plan:

- Endowment insurance Plans are a combination of insurance and investment. The insured will get a lump-sum along with bonuses on policy maturity( after a specific term) or on death.

- Most of the cases maturity happens in 10, 15 or 20 years of policy term or up to certain age limit. Sometime even in case of critical illness also policies are paid out.

- Endowment plans are designed to provide an investor long term savings. This savings allow an investor to plan their future goals.

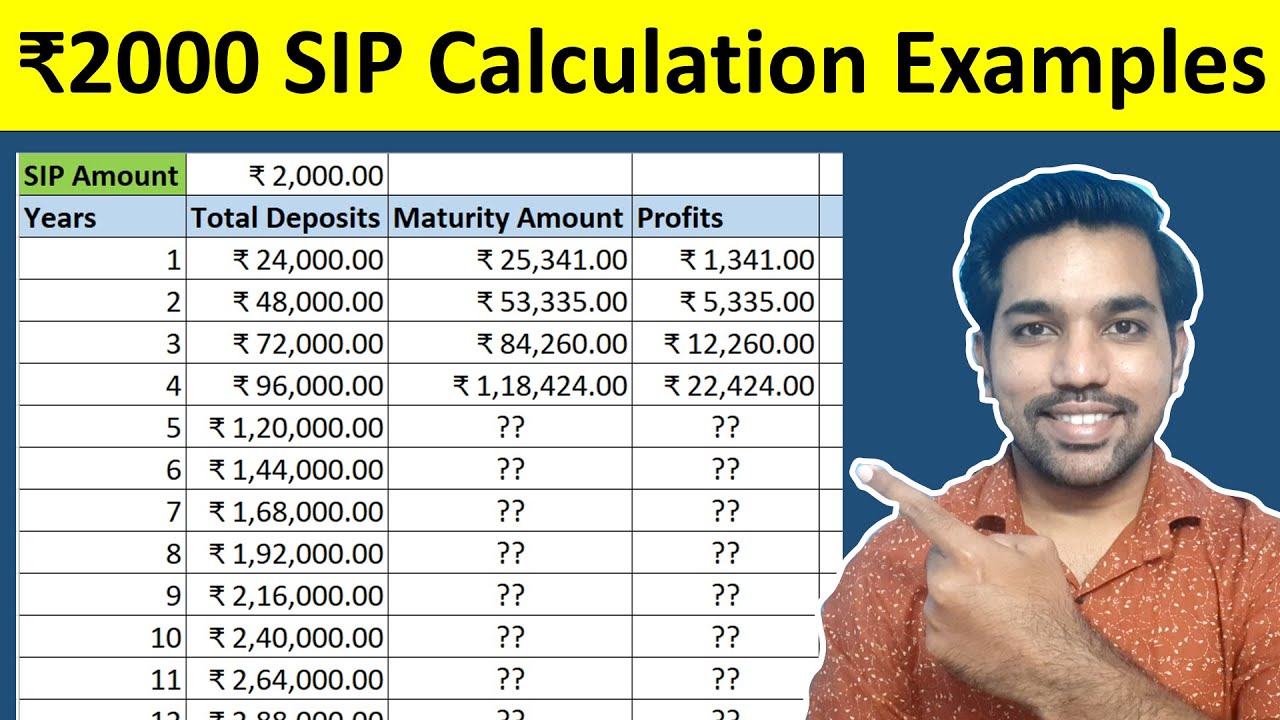

Returns with Rs. 2000 SIP for 15 Years Video:

Pension Insurance Plans

- A pension plan or annuity plan is a financial tool that enables an investor to accumulate funds for his/her golden years. This plan provides income to an policy holder after retirement.

- This plan provides guaranteed income to the policy holder for the rest of his/her life after retirement.

- The amount invested by the policy holder is further invested by the insurance company to generate returns throughout the investment years and once the policy holder reached the retirement age pension payout starts.

- In addition to the retirement benefits the pension plans or annuity plans also provide life cover benefits. In case if the policy holder passes away during the policy term. Nominee receive death claim amount and if the policy holder or a life insured reached retirement age then he/she starts getting pension or annuity annually, half yearly, monthly modes basis options chosen by him/her.

ALSO USE: Senior Citizen Saving Scheme Calculator

Importance of Retirement Plan or Pension Plan or Annuity Plan

Based on your current lifestyle and expenses and considering future expenses and lifestyle it is very important to seat and decide about investment in life insurance retirement plans or pension plans. It is important to start investing in pension plan because:

- It is a good practice or a disciplinary action to start investing in a regular mode today for planning retirement goals nd future expenses.

- It also helps in providing life cover or protection to your family and future saving for your retirement.

- One should always invest in a pension plan which provides guaranteed income after retirement to meet financial goals and various other expenses.

- One should always start planning his/ her retirement as soon as they start earning.

ALSO READ: How to Invest in NPS Online

How do pension plan work?

One should always invest in pension plan so that they have sufficient and stable income once reaching retirement age.

However It is also important to know to understand as to how does these pension or Annuity or retirement plan works?

Unlike other life insurance investments, in pension plan also the investor needs to pay premium and once the premium payment term is over an investor is liable to receive pension benefits.

However investor can either:

- Withdraw the entire pension amount in one go

- Can purchase an annuity plan or

- Withdraw partial pension amount and use the remaining amount to invest in annuity plan.

Investor also has an option to take pension plan on both single life or joint life. Option to take immediate or deferred annuity is also available.

Conclusion

So it is important for you to buy a life insurance cover based on the factors mentioned above. You can select any one or two life insurance options to help your family members in providing financial stability after any mishap.

In case you need assistance or guidance in buying the best Life Insurance for you, please Fill this Form to get more information.

Some more Reading:

- Rs. 1000 in Sukanya Samriddhi Yojana

- PPF vs Mutual Funds Which is Better

- Why Home Loan Tenure Increases with Interest rate

Frequently Asked Questions

What are the 2 main types of life insurance?

The 2 main types of life insurance are term life insurance and money back insurance plans. In term life insurance, you get pure life insurance and there is no return of premiums except in return of premium term insurance.

On other side there are multiple plans under money back insurance that gives you returns along with life cover.

What is the basic type of life insurance?

The basic type of life insurance is term life insurance in which you pay the premium amount to get life cover. The premium amount is usually low for pure term life insurance.

What is called life insurance?

Life insurance is a product provided by life insurance companies or banks to provide you life cover. This helps your family members with financial stability such as regular income or paying back the pending loan amount in case of any mishap with you.

Which Life Insurance if Best for you?

It depends on your goals and investment strategy. If you want pure life insurance than go for term life insurance with low premiums, but you want to make investments along with having a life cover than you should opt for money back life insurance.

Save Home Loan Interest Amount!

Use Home Loan Excel Calculator that will help you to Save Interest Amount on Home Loan EMI.

Click below button to download Home Loan EMI and Prepayment Calculator in Excel:

Watch how Home Loan Calculator in Excel Works

Income Tax Calculator App – FinCalC

For Income Tax Calculation on your mobile device, you can Download my Android App “FinCalC” which I have developed for you to make your income tax calculation easy.

What you can do with this mobile App?

- Calculate Income Tax for FY 2025-26 and previous FY 2024-25

- Enter estimated Investments to check income tax with Old and New Tax Regime

- Save income tax details and track regularly

- Know how much to invest more to save income tax

- More calculators including PPF, SIP returns, Savings account interest and lot more

Use Popular Calculators:

- Income Tax Calculator

- Home Loan EMI Calculator

- SIP Calculator

- PPF Calculator

- HRA Calculator

- Step up SIP Calculator

- Savings Account Interest Calculator

- Lump sum Calculator

- FD Calculator

- RD Calculator

- Car Loan EMI Calculator

- Bike Loan EMI Calculator

- Sukanya Samriddhi Calculator

- Provident Fund Calculator

- Senior Citizen Savings Calculator

- NSC Calculator

- Monthly Income Scheme Calculator

- Mahila Samman Savings Calculator

- Systematic Withdrawal Calculator

- CAGR Calculator

I’d love to hear from you if you have any queries about Personal Finance and Money Management.

JOIN Telegram Group and stay updated with latest Personal Finance News and Topics.

Download our Free Android App – FinCalC to Calculate Income Tax and Interest on various small Saving Schemes in India including PPF, NSC, SIP and lot more.

Follow the Blog and Subscribe to YouTube Channel to stay updated about Personal Finance and Money Management topics.