A Life Term Insurance Plan is a pure protection policy that provides financial coverage to your family in case of your untimely demise during the policy term. It offers high coverage at affordable premiums and is one of the most essential tools for long-term financial security.

- What is Life Term Insurance Plan?

- Key Features of Term Insurance

- How Term Insurance Works?

- Conditions and Eligibility to buy Life Term Insurance

- Who Should Buy Term Insurance?

- Benefits of having Life Term Insurance

- Types of Life Term Insurance

- Term Insurance vs Other Life Insurance Plans

- How to select Good Life Term Insurance Plan?

- Frequently Asked Questions:

What is Life Term Insurance Plan?

- Term life Insurance plan is the most simplest and affordable form of life insurance plan from other Types of Life Insurance which provides financial protection to the family of life insured at the most affordable rates.

- These policies offers only guaranteed death benefit and does not have any feature of a savings component.

- In case of death of the insured individual during the policy term, the death benefit is paid by the company to its nominee.

- The sum assured amount is paid out to the nominee in case of the death of the person insured during the term of the policy.

Key Features of Term Insurance

| Feature | Description |

| 🔒 Death Benefit | Lump sum paid to nominee on policyholder’s death during the term |

| 💰 Affordable Premiums | Lower cost compared to other life insurance plans |

| 📈 High Coverage | Coverage up to ₹1 crore or more |

| 🧾 Tax Benefits | Deductions under Section 80C and 10(10D) |

| 🔁 Flexible Payout Options | Lump sum, monthly income, or staggered payouts |

| 📅 Policy Term | Ranges from 5 to 40 years or till age 99 |

| 🔄 Return of Premium Option | Refund of premiums if policyholder survives the term |

| 🧍♂️ Health-Based Discounts | Lower premiums for non-smokers and healthy individuals |

ALSO READ: How to Build Wealth on Rs. 10000 Salary

Let us now understand How Term Life Insurance Works.

How Term Insurance Works?

A term life insurance policy is the simplest / purest form of life insurance : You pay a premium for a period of time – typically between 10 and 30 years or as you choose – and if you die during that time a cash benefit is paid to your family (or anyone else you name as your nominee).

- Filling out the proposal form :

You need to disclose the following information in the term plan application form:

– past or current medical history

– current health conditions

– lifestyle habits

– age

– annual income

– nature of your profession

Factors that can increase the premium amount include:

– A higher age

– Unhealthy habits like smoking

– Risk-prone hobbies like skydiving

– Hazardous professions

– Chronic health problems

- Decide your life cover: Your coverage should be enough to meet your dependents’ current living expenses and future needs. Children’s college fees, children marriage, spouses’ old-age needs, and pending liabilities are some of the factors to consider.

- Assigning a nominee: Life assured need to name the person who will receive his/her term plan’s monetary benefits. It should be an immediate family member who will take care of his/her dependents.

Conditions and Eligibility to buy Life Term Insurance

- Education Qualification: The minimum education qualification required to buy a term life insurance plan is graduation. However, this may vary from insurer to insurer.

- Citizenship: Anyone residing in India can buy term insurance. The term insurance eligibility remains the same if he shifts abroad for academics or work purposes after the purchase. However, NRIs or PIOs can also enjoy the benefits of a term insurance plan in India.

ALSO READ: Why Term Life Insurance is Better than Money Back Plans

Who Should Buy Term Insurance?

| Life Stage | Why It’s Needed |

| Young Professionals | Lock in low premiums early |

| Married Individuals | Protect spouse and future children |

| Parents | Secure children’s education and lifestyle |

| Loan Holders | Cover liabilities like home or personal loans |

| Business Owners | Protect business continuity and family income |

Benefits of having Life Term Insurance

Term insurance plans offer financial security for the entire family in case of the unfortunate death of the policyholder. Also, he/she can get optional coverage for critical illnesses or accidental death. Policy holder is covered for a long duration, while the premiums are affordable.

Term insurance offers multiple benefits to customers. Here are a few you should be aware of:

- Payout of Sum Insured – In case of the unfortunate demise of the person insured, the family members will receive the sum assured as a payout. The policyholder can choose for this payout to be in the form of a lump sum, an income that is either monthly or annual, a combination of lump sum and income or an increasing income at the inception. This will help take care of financial needs and household expenses among other costs.

- Critical Illness Coverage – In case optional Critical Illness Coverage is included in your term insurance plan, you will get a lump sum payout upon diagnosis of any critical illness that is covered in the plan.

- Accidental Death Benefit – You can add the Accidental Death Benefit to your term insurance plan. This will offer protection against any mishaps in the future.

- Coverage for Terminal Illnesses -Term insurance plans can give you lump sum payouts in case of diagnosis of terminal illnesses such as AIDS.

- Safety for loans and other assets: Another benefit of a term insurance plan is that it makes it easier for you to take out a personal, car or home loan. Term insurance plans act as safety for a loan, i.e, in case of an emergency or untimely death, the family can repay the loan using the term insurance death benefit pay-out and rid themselves of any debt. Thus, term life insurance policies can help take care of your debt without burdening your family or affecting their lifestyle.

ALSO READ: Types of General Insurance in India

Types of Life Term Insurance

Below are some of the types of Life Term Insurance:

Without return of premium term insurance

This is also know as Level Term Insurance plan. The basic and the simple form of term life insurance is known as a without return of premium term insurance or level term plan. In this plan, the sum assured chosen at the inception of the policy remains same throughout the policy term. The death benefit is paid to the nominees in case something happens to the policyholder or Life assured. Premium paid by the policy holder is very minimal and affordable to policyholder on annual basis.

With return of premium term insurance

Life Term plan with return of premium is a popular type of plan that offers back all the premiums paid by the policyholder if they survive after the policy term is over. premium paid by policyholder is high as compared to without return of premium term life insurance.

Term plan with riders

Term plan with riders comes with various rider options such as accidental death cover, critical illness cover, loss of employment cover, accidental disability benefit rider, permanent disability cover, waiver of premium rider, income benefit rider, and many more such riders which can be opted along with normal term life insurance by paying very less premium amount.

One time premium term life insurance plans

Also known as Single premium term insurance plans, can offer the convenience of a one-time payment. It is very much suitable option for those individuals who have a lump sum money or who wishes to pay one time or are uncertain about their ability to make regular premium payments. Benefits of taking single premium term insurance is that it is very much convenient, affordable, no risk of policy lapse and most important tax benefits.

Renewable Term life insurance plans

Renewable term life insurance plans give the policyholder right to renew their existing term insurance for another period when a term ends, regardless of the state of health. With each new term the premium is increased.

Term Insurance vs Other Life Insurance Plans

| Criteria | Term Insurance | Endowment Plan | ULIP |

| Purpose | Pure protection | Protection + savings | Protection + investment |

| Premium | Low | Moderate to high | High |

| Maturity Benefit | No (unless ROP) | Yes | Yes |

| Returns | None | Guaranteed | Market-linked |

| Flexibility | High | Moderate | High |

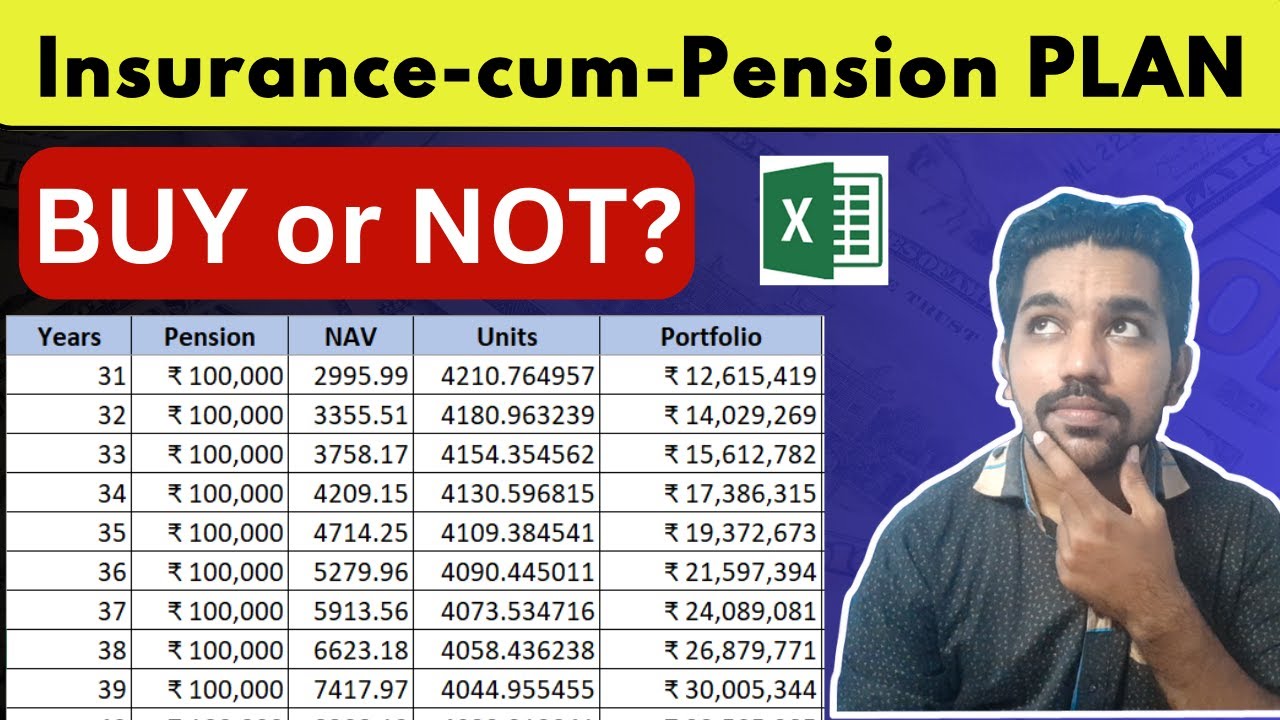

Harsh Truth of Insurance cum Pension Plans Video

Watch more Videos on YouTube Channel

How to select Good Life Term Insurance Plan?

Term insurance is a type of life insurance which offers financial coverage against the unfortunate demise of the life insured during the policy term. It is a cost-effective way to provide financial protection for your family members and loved ones. Life insurance provides peace of mind and tax benefits to the policy holder. Keeping your loved ones safe and protected against unfortunate events and circumstances is the utmost priority of any individual. One of the first steps is understanding how to choose term insurance for your family members. An individual can secure his / her family members future effectively when he/she make a wise decision of buying a term life insurance policy .

Few tips while choosing good term insurance policy:

- Analyze Your Income:

One of the common concern among every individual people is how to decide term insurance amount that will be enough for his/her family members or loved ones. It is advisable to analyses your own income to get a more practical picture of it. When an individual can evaluate or analysis his/ her limitations of income, that is the best time one can invest better. - Look at the Existing Liabilities:

Debts , borrowing and other liabilities are other important factors in the process of choosing good term life insurance. In many scenario life assured has an existing loans and in their absence it is a burden on dependents of policy holder if there is no existing term life insurance plans to repay those loans.

It is painful for any of us to think of our loved ones bearing the burden of debt repayment without any adequate support. Hence, it is crucial to understand how to choose best term plan by carefully considering the debts and liabilities in life. - Check Claim Settlement Ratio of the Insurer:

The ratio defines the percentage of claims successfully settled by an insurance company compared to the total number of claims received by them in a financial year. It reveals the capacity of an insurance provider to keep their promise of providing financial support in times of need, hence it is very important to check claim settlement ratio while purchasing the term life insurance plans.

In case you need assistance or guidance in buying the best Life Insurance for you, please Fill this Form to get more information.

Some more Reading:

Frequently Asked Questions:

What does a term insurance do?

Term Insurance helps you to provide financial cover for your family in case of your sudden death. You pay the low premium amount compared to other money back plans every year and are assured of a predefined sum up to the policy term. The financial cover provided by the insurance company helps your family to cover for remaining debt and other payables or expenses to be covered in your absence.

Is Term Insurance a good option?

Yes Term Life Insurance is one of the best options if you are looking to cover your family financially in case of your sudden death, with minimum premium amount to be paid every year. Moreover, this premium amount once set, will not increase throughout the term of the policy till it is active.

Do we get the premiums back in Term Insurance?

There is a type of term insurance that returns your premiums paid, but this term insurance comes with higher premium payment compared to the term insurance with low premium payments. So yes you can get the premiums back in term life insurance with return of premium feature.

Which insurance company is best for term plan?

Some of the best insurance companies are ICICI Life, HDFC Life Max Life, etc from where you can buy term life insurance offline or online

Is 50 lakh term insurance enough?

It depends on your financial goals and the amount of debt you have taken. If you need to make a payment of Rs. 20 Lakh than Rs. 50 lakh cover sounds to be a good option that will cover for your debts as well as providing financial stability to your family after your demise. But in case your current debt is around Rs. 70 to rs. 80 Lakh, you need to consider term life insurance of at least Rs. 1 crore or more.

Can I take 2 term insurance?

Yes multiple term insurance against the same policyholder is allowed

What is a good term insurance amount?

Good amount will depend on your total debt and your family’s lifestyle. Add up all the debt in the form of loans and other payables and consider the monthly expenses of your family. At least 5 years expenses must be covered for your family after your demise. Add all the numbers to get the good amount for term insurance.

For example, if your total debt is Rs. 20 lakh and monthly expenses is Rs. 20,000 for your family, considering inflation of 5%, total expenses for 5 years will be around Rs. 13.30 Lakh, which makes total of Rs. 33.30 Lakh. So having Rs. 50 lakh as life cover will cover for all these expenses along with a margin of safety.

Save Home Loan Interest Amount!

Use Home Loan Excel Calculator that will help you to Save Interest Amount on Home Loan EMI.

Click below button to download Home Loan EMI and Prepayment Calculator in Excel:

Watch how Home Loan Calculator in Excel Works

Income Tax Calculator App – FinCalC

For Income Tax Calculation on your mobile device, you can Download my Android App “FinCalC” which I have developed for you to make your income tax calculation easy.

What you can do with this mobile App?

- Calculate Income Tax for FY 2025-26 and previous FY 2024-25

- Enter estimated Investments to check income tax with Old and New Tax Regime

- Save income tax details and track regularly

- Know how much to invest more to save income tax

- More calculators including PPF, SIP returns, Savings account interest and lot more

Save Home Loan Interest Amount!

Use Home Loan Excel Calculator that will help you to Save Interest Amount on Home Loan EMI.

Click below button to download Home Loan EMI and Prepayment Calculator in Excel:

Watch how Home Loan Calculator in Excel Works

Income Tax Calculator App – FinCalC

For Income Tax Calculation on your mobile device, you can Download my Android App “FinCalC” which I have developed for you to make your income tax calculation easy.

What you can do with this mobile App?

- Calculate Income Tax for FY 2025-26 and previous FY 2024-25

- Enter estimated Investments to check income tax with Old and New Tax Regime

- Save income tax details and track regularly

- Know how much to invest more to save income tax

- More calculators including PPF, SIP returns, Savings account interest and lot more

Use Popular Calculators:

- Income Tax Calculator

- Home Loan EMI Calculator

- SIP Calculator

- PPF Calculator

- HRA Calculator

- Step up SIP Calculator

- Savings Account Interest Calculator

- Lump sum Calculator

- FD Calculator

- RD Calculator

- Car Loan EMI Calculator

- Bike Loan EMI Calculator

- Sukanya Samriddhi Calculator

- Provident Fund Calculator

- Senior Citizen Savings Calculator

- NSC Calculator

- Monthly Income Scheme Calculator

- Mahila Samman Savings Calculator

- Systematic Withdrawal Calculator

- CAGR Calculator

I’d love to hear from you if you have any queries about Personal Finance and Money Management.

JOIN Telegram Group and stay updated with latest Personal Finance News and Topics.

Download our Free Android App – FinCalC to Calculate Income Tax and Interest on various small Saving Schemes in India including PPF, NSC, SIP and lot more.

Follow the Blog and Subscribe to YouTube Channel to stay updated about Personal Finance and Money Management topics.

Use Popular Calculators:

- Income Tax Calculator

- Home Loan EMI Calculator

- SIP Calculator

- PPF Calculator

- HRA Calculator

- Step up SIP Calculator

- Savings Account Interest Calculator

- Lump sum Calculator

- FD Calculator

- RD Calculator

- Car Loan EMI Calculator

- Bike Loan EMI Calculator

- Sukanya Samriddhi Calculator

- Provident Fund Calculator

- Senior Citizen Savings Calculator

- NSC Calculator

- Monthly Income Scheme Calculator

- Mahila Samman Savings Calculator

- Systematic Withdrawal Calculator

- CAGR Calculator

I’d love to hear from you if you have any queries about Personal Finance and Money Management.

JOIN Telegram Group and stay updated with latest Personal Finance News and Topics.

Download our Free Android App – FinCalC to Calculate Income Tax and Interest on various small Saving Schemes in India including PPF, NSC, SIP and lot more.

Follow the Blog and Subscribe to YouTube Channel to stay updated about Personal Finance and Money Management topics.