While you are paying Home Loan EMI or planning to buy new house on Home Loan, it is very important to know some Home Loan Repayment Tips and strategies so that you can close your home loan before time instead of paying EMI for long term in your life. Imagine how great you would feel if you close your home loan before time and enjoy the rest of your life stress-free without having to necessarily work to pay the home loan EMIs. We will see some best ways to repay home loans.

Let us understand 5 Home Loan Repayment Tips in detail:

1. Make Home Loan Prepayments

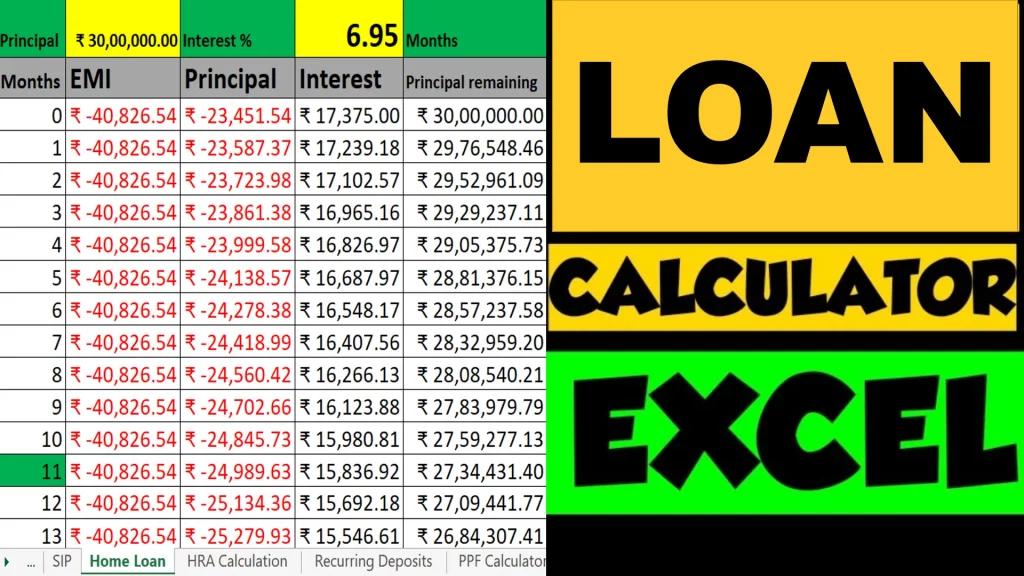

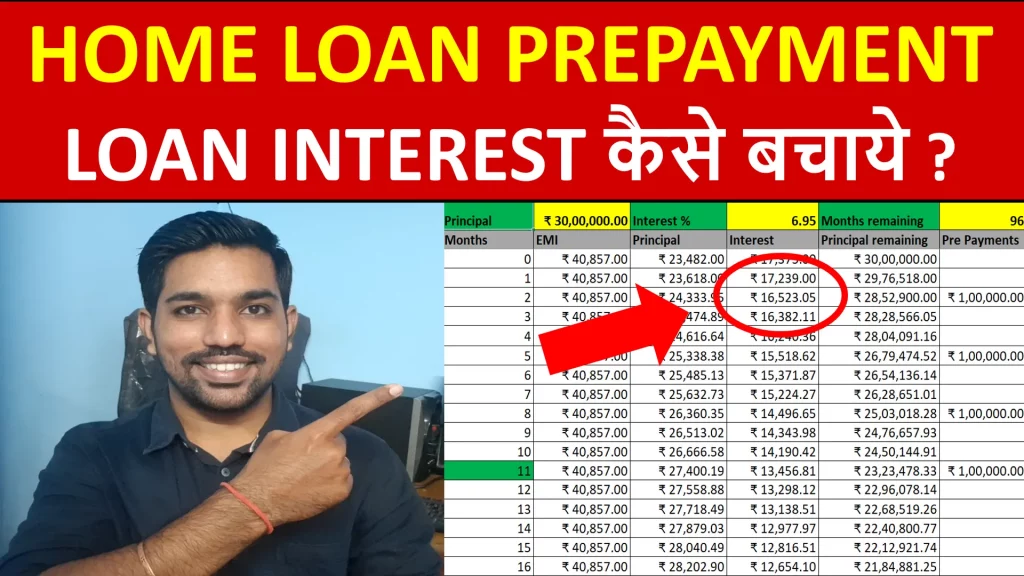

Home Loan Prepayments is a way to reduce the remaining principal balance on your home loan. The idea is to accumulate some amount while you are paying EMI every month, and once required amount is accumulated (at least 2-3 months of your EMI amount), you deposit this amount to your bank or financial institution from where you have taken home loan.

This amount will than be reduced from your principal balance remaining in your home loan, thus reducing the interest amount you have to pay in your loan EMI. It also helps to close your loan before time if you choose to reduce tenure.

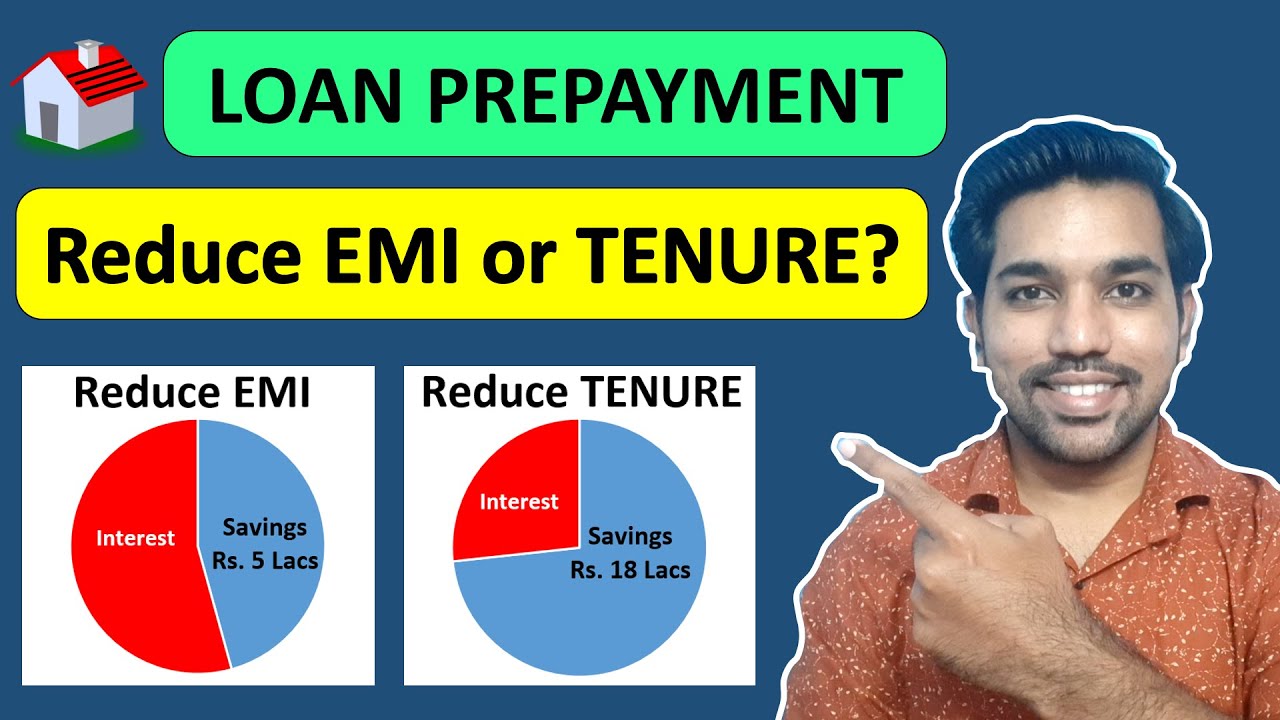

While making prepayments, you have 2 options:

- Reduce Loan Tenure or

- Reduce Loan EMI

It is better to reduce loan tenure to save maximum interest on your home loan and also to close your loan before time.

Watch below video to understand more about Home loan Prepayments:

Home Loan Prepayment Video

Watch more Videos on YouTube Channel

2. Keep Loan Interest Rate Low

While opting for home loan to buy your dream house, it is very important that you check the interest rates on home loan in all possible banks and financial institutions. Since you will be paying home loan EMIs for coming many years of your life, due diligence must be done from your side to save maximum of the interest amount on loan.

Home Loan interest rate plays a crucial role in knowing how much total interest you will have to pay throughout the loan tenure.

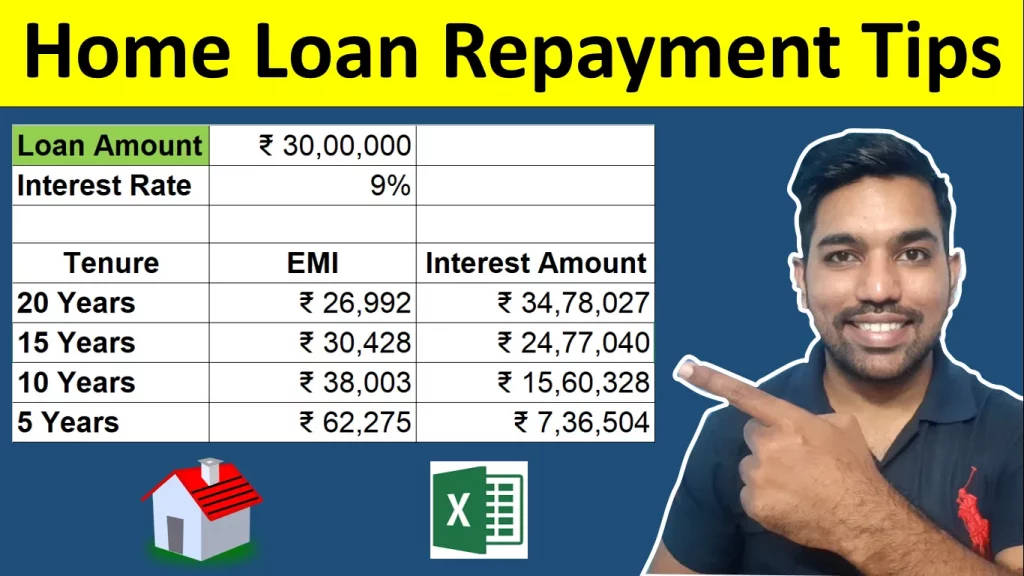

For example, on home loan of Rs. 30,00,000 for 10 years, below are the loan EMI of various loan interest rates:

- Total Interest Paid at Interest Rate of 9.5%: Rs. 16,58,312

- Total Interest Paid at Interest Rate of 9.0%: Rs. 15,60,328

- Total Interest Paid at Interest Rate of 8.5%: Rs. 14,63,485

- Total Interest Paid at Interest Rate of 8.0%: Rs. 13,67,793

As seen above, lower the interest rate, total interest to be paid by you on your home loan throughout the tenure will be less, and this is how the interest amount can be saved by you in long term on your home loan.

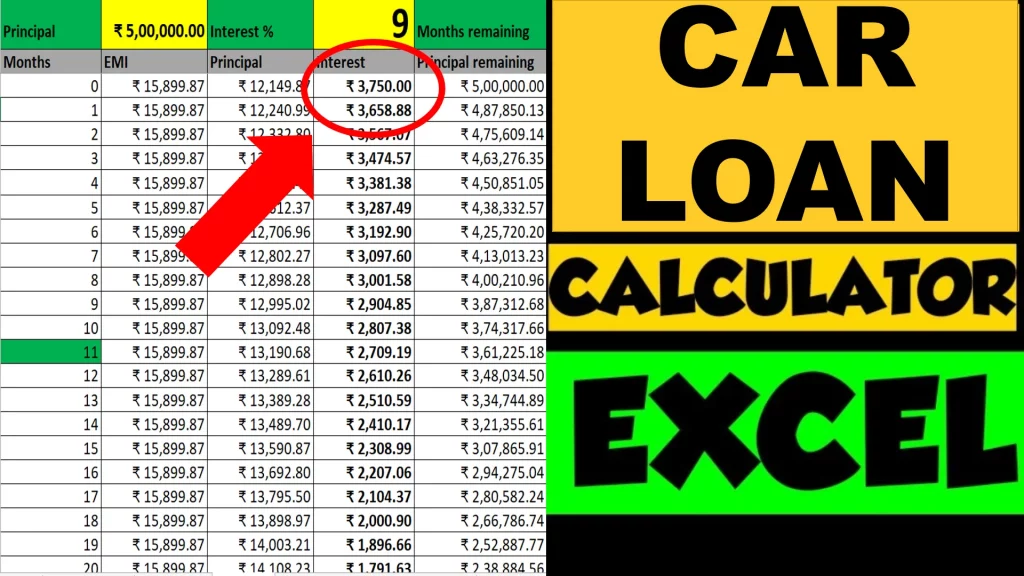

Use Home Loan EMI Calculator here:

3. Keep Loan Tenure Low

Similar to interest rate, the lower the tenure, less interest amount will have to be paid by you throughout the loan tenure.

Let us take the same example as above of Rs. 30,00,000 loan at 9% interest rate. Below is the total interest to be paid on different loan tenure:

- Total Interest Paid with 15 Years Tenure: Rs. 24,77,040

- Total Interest Paid with 12 Years Tenure: Rs. 19,16,293

- Total Interest Paid with 10 Years Tenure: Rs. 15,60,328

So as seen above, the total interest amount to be paid decreases with the decrease in loan tenure. Please make note that the EMI amount will increase with the decrease in loan tenure so you have to set the loan tenure accordingly to afford the monthly Loan EMI to be paid.

4. Never miss Loan EMI Payments

Loan EMI need to be paid every month and you should never miss any home loan EMI for the due date.

Make sure you have sufficient balance in your bank account for auto debit of the loan amount, so that you don’t have to pay any penalties on late EMI payments.

5. Tax Benefits on Home Loan

You get Tax Benefits on your Home Loan under Section 80C and Section 24(b). Below are the tax deduction limits for FY 2025-26 with Old Tax Regime:

- Section 80C: Rs. 1,50,000

- Section 24(B): Rs. 2,00,000

Based on Section 80C, you get tax deduction on the principal portion of your loan EMI. Where as based on Section 24(b), you are eligible to claim up to Rs. 2,00,000 as interest amount in home loan EMI in financial year.

Please note that these deductions are available in old tax regime. New tax regime have less number of deductions to be claimed.

Conclusion

So these are some of the Home Loan Repayment tips that you should know. Below is the summary:

- Make Home Loan Prepayments

- Keep Interest Rate Low

- Keep Home Loan Tenure Low

- Never Miss EMI Payments

- Tax Benefits on Home Loan EMI Payments

Some more Reading:

- Variable Rate Home Loan Calculation

- Home Loan Mistakes to Avoid

- Buy vs Rent a House Calculator [Excel]

Save Home Loan Interest Amount!

Use Home Loan Excel Calculator that will help you to Save Interest Amount on Home Loan EMI.

Click below button to download Home Loan EMI and Prepayment Calculator in Excel:

Watch how Home Loan Calculator in Excel Works

Income Tax Calculator App – FinCalC

For Income Tax Calculation on your mobile device, you can Download my Android App “FinCalC” which I have developed for you to make your income tax calculation easy.

What you can do with this mobile App?

- Calculate Income Tax for FY 2025-26 and previous FY 2024-25

- Enter estimated Investments to check income tax with Old and New Tax Regime

- Save income tax details and track regularly

- Know how much to invest more to save income tax

- More calculators including PPF, SIP returns, Savings account interest and lot more

Use Popular Calculators:

- Income Tax Calculator

- Home Loan EMI Calculator

- SIP Calculator

- PPF Calculator

- HRA Calculator

- Step up SIP Calculator

- Savings Account Interest Calculator

- Lump sum Calculator

- FD Calculator

- RD Calculator

- Car Loan EMI Calculator

- Bike Loan EMI Calculator

- Sukanya Samriddhi Calculator

- Provident Fund Calculator

- Senior Citizen Savings Calculator

- NSC Calculator

- Monthly Income Scheme Calculator

- Mahila Samman Savings Calculator

- Systematic Withdrawal Calculator

- CAGR Calculator

I’d love to hear from you if you have any queries about Personal Finance and Money Management.

JOIN Telegram Group and stay updated with latest Personal Finance News and Topics.

Download our Free Android App – FinCalC to Calculate Income Tax and Interest on various small Saving Schemes in India including PPF, NSC, SIP and lot more.

Follow the Blog and Subscribe to YouTube Channel to stay updated about Personal Finance and Money Management topics.