If you are a home owner and already paying EMI for your Home Loan, Home Loan Part Payments can be a game changer for you that can help to achieve financial freedom before time. It should be everyone’s goal to be debt free and take less or no stress in terms of finances. Home Loan Part Payments is a way to close your home loan before time by making extra payments apart from the home loan EMIs. Home Loan Part Payments reduce the principal amount from your loan balance, thus reducing the interest amount you have to pay and the loan tenure as well.

Now, while making the part payments, you have 2 options – reduce EMI or tenure. Reducing tenure will save you more interest compared to reducing EMI, since reducing tenure reduces the duration for which the loan will be paid.

- Home Loan Part Payments Video using Excel Calculator

- Understanding Home Loan Part Payments: Beyond Your EMI

- The Critical Choice: Reduce Tenure, Not EMI – Why it Matters

- Using Tax Benefits with Your Home Loan

- The Power of Home Loan Excel Calculator: Visualize Your Savings

- Frequently Asked Questions (FAQ)

- Conclusion: Take Control of Your Home Loan

Below is the video to understand Home Loan Part Payments

Home Loan Part Payments Video using Excel Calculator

Understanding Home Loan Part Payments: Beyond Your EMI

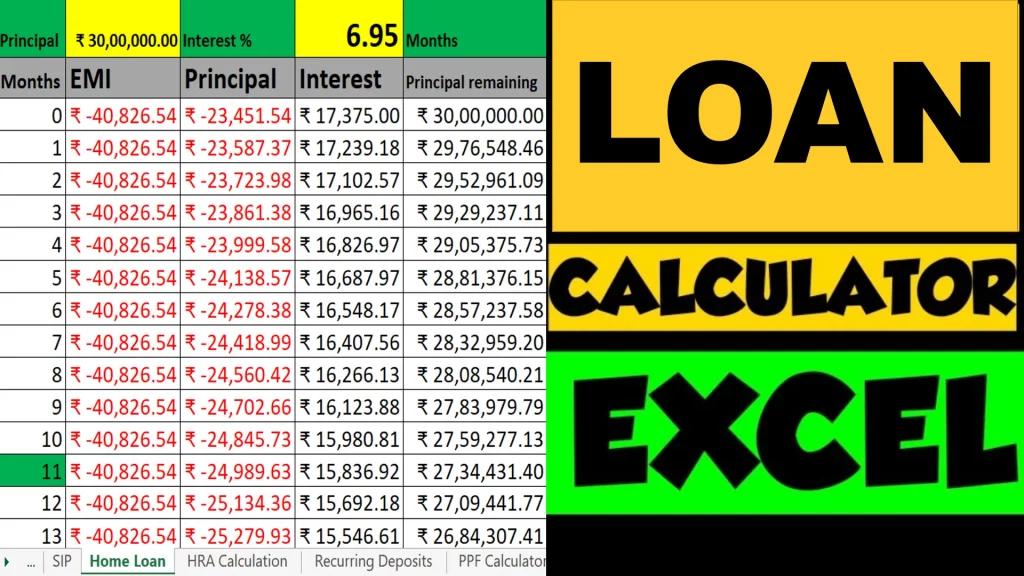

Your monthly EMI (Equated Monthly Installment) is a structured payment that comprises two key components: the principal amount, which directly reduces your outstanding loan, and the interest amount, which is the bank’s profit for lending you the money. Over the life of a long-term home loan, the total interest paid can be substantial and can delay your financial freedom..

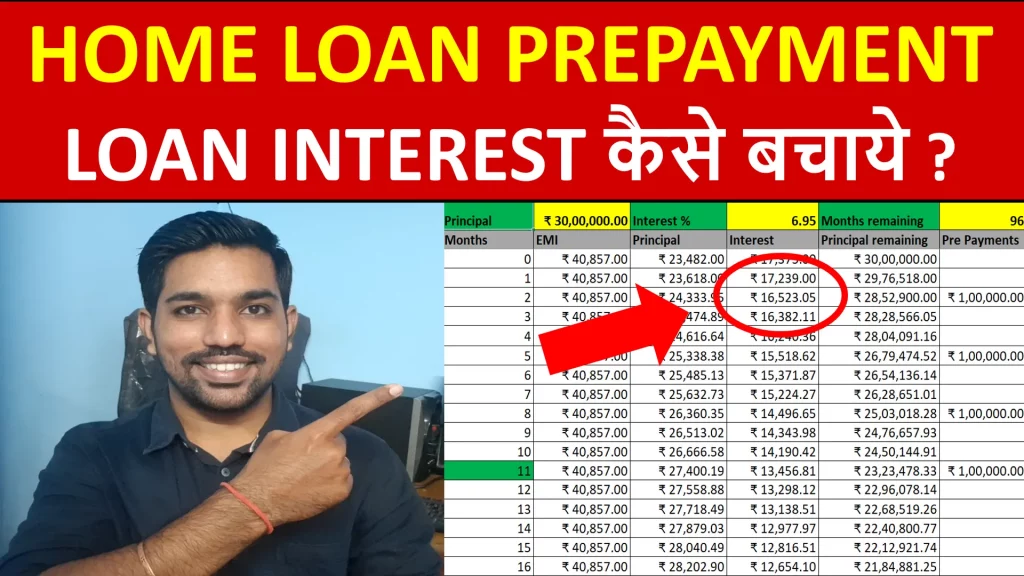

A home loan part payment is an additional lump sum payment you make directly towards your principal balance. By reducing the principal, you effectively lower the remaining loan balance on which your interest is calculated. This simple act has a cascading effect, leading to significant interest savings over the remaining loan tenure. It’s a proactive approach to debt management that puts you in control, and help you to achieve financial freedom by closing your home loan before time.

ALSO USE: Home Loan EMI Calculator

The Critical Choice: Reduce Tenure, Not EMI – Why it Matters

When you make a part payment, your bank will typically present you with two options:

- Reducing Your EMI: This option lowers your monthly payment, providing immediate relief to your budget. While this might seem appealing, it generally keeps your original loan tenure intact, meaning you’ll still pay interest for the same duration. Paying the interest for same duration must be highlighted here, since “time is money“. The overall interest savings with this option are considerably less, compared to the other option discussed below.

- Reducing Your Loan Tenure: This is the most financially sane choice. By keeping your EMI the same (or even slightly increasing it if feasible), you dramatically shorten the time it takes to repay your loan. This strategy maximizes your interest savings because you’re paying off the principal faster, thereby reducing the period over which interest accrues. You give less time for your home repayment, and you will save more on the interest part.

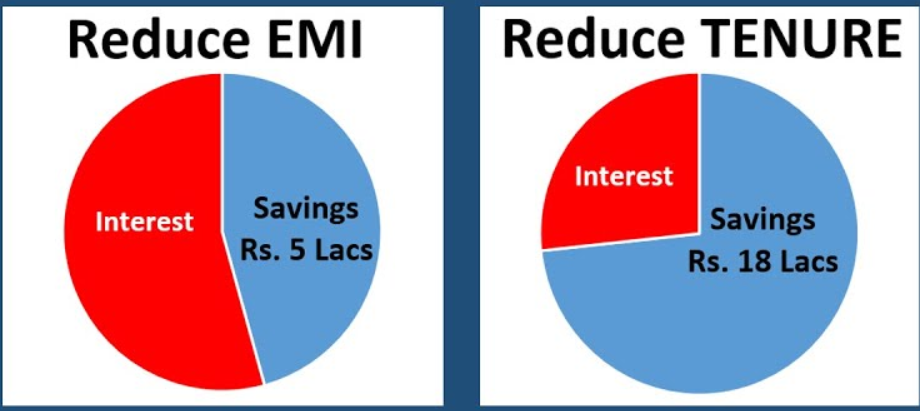

Consider this illustrative example: a ₹25 lakh home loan with a 15-year tenure at an 8.5% interest rate. If you make two ₹5 lakh part payments, one in the 6th month and another in the 12th month, choosing to reduce your loan tenure could result in total savings of ₹2,25,000 and shorten your loan by approximately a year. In stark contrast, opting to reduce your EMI with the same part payments would yield significantly lower savings, around ₹88,881. The power of reducing tenure is undeniable when it comes to long-term financial gains.

Below is the infographic that shows high savings with reducing tenure compared to reducing EMI:

ALSO READ: Home Loan Repayment Tips

Using Tax Benefits with Your Home Loan

While strategizing for part payments, don’t forget the valuable tax benefits associated with home loans in India:

- Section 80C: The principal amount of your home loan repaid during a financial year is eligible for a deduction of up to ₹1.5 lakh under the old tax regime.

- Section 24: The interest paid on your home loan can be claimed as a deduction up to ₹2 lakh.

These tax benefits, combined with a disciplined part payment strategy, can further enhance your financial well-being.

Section 24 is also applicable with new tax regime if the property is a let out property.

The Power of Home Loan Excel Calculator: Visualize Your Savings

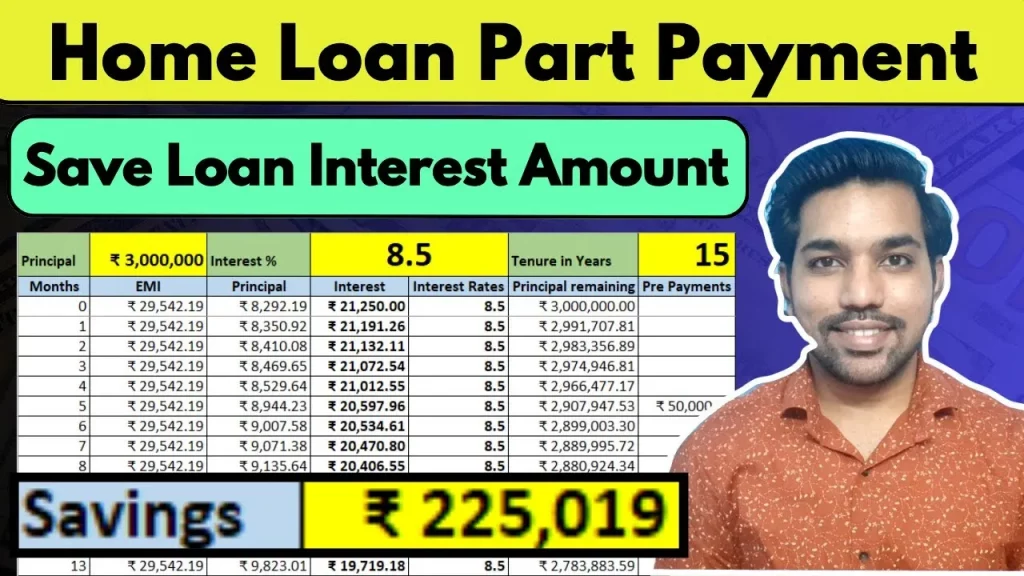

Now comes the most important part – how you can save interest on your home loans and makes calculations as per the video mentioned above? Understanding the precise impact of your part payments can be complex. This is where a dedicated Excel calculator becomes an invaluable tool. Such a calculator allows you to:

- Analyze potential savings: See exactly how much interest you can save with different part payment amounts and frequencies.

- Projecting tenure reduction: Understand how each part payment shortens your loan duration.

- Break down EMI components: Get a clear picture of the principal and interest portions of your monthly payments.

- Adjust for interest rate changes: Updates with fluctuating interest rates to see their effect on your loan.

Tools like these empower you to make data-driven decisions and gain a clear understanding of your home loan repayment journey. You can download home loan Part payment excel calculator using below button:

Frequently Asked Questions (FAQ)

What is the primary benefit of making home loan part payments?

The primary benefit is significantly reducing the total interest you pay over the loan tenure and shortening the time it takes to become debt-free and achieve financial freedom. This also reduces your financial stress by reducing the loan tenure.

Should I reduce my EMI or my loan tenure after a part payment?

It is generally more beneficial to reduce your loan tenure. This strategy leads to much greater overall interest savings compared to reducing your EMI. Since reducing tenure reduces the time period for which you pay the home loan, this significantly reduces the overall interest amount you need to pay.

Are there any tax benefits associated with home loan part payments?

While part payments directly reduce principal, the principal amount repaid through your regular EMIs and part payments are eligible for deduction under Section 80C, and the interest paid is deductible under Section 24. So yes, the part payments can provide you Section 80C benefits.

How can an Excel calculator help with home loan part payments?

An Excel calculator helps you visualize and calculate the impact of part payments on your interest savings, loan tenure, and EMI breakdown, enabling better financial planning.

Conclusion: Take Control of Your Home Loan

Home loan part payments are a powerful, yet often underutilized, tool for accelerating your path to financial freedom. By understanding the mechanics of part payments, prioritizing tenure reduction, and leveraging available tools like Excel calculators, you can significantly reduce your interest burden and achieve your dream of a debt-free home much sooner. It’s a smart financial move that empowers you to take control of one of your biggest liabilities and build a more secure financial future.

Some more Reading:

- 7 Home Loan Mistakes you should avoid

- Fixed vs Floating Interest Rate Home Loan Which is Better

- Why Home Loan Tenure increases automatically

Save Home Loan Interest Amount!

Use Home Loan Excel Calculator that will help you to Save Interest Amount on Home Loan EMI.

Click below button to download Home Loan EMI and Prepayment Calculator in Excel:

Watch how Home Loan Calculator in Excel Works

Income Tax Calculator App – FinCalC

For Income Tax Calculation on your mobile device, you can Download my Android App “FinCalC” which I have developed for you to make your income tax calculation easy.

What you can do with this mobile App?

- Calculate Income Tax for FY 2025-26 and previous FY 2024-25

- Enter estimated Investments to check income tax with Old and New Tax Regime

- Save income tax details and track regularly

- Know how much to invest more to save income tax

- More calculators including PPF, SIP returns, Savings account interest and lot more

Use Popular Calculators:

- Income Tax Calculator

- Home Loan EMI Calculator

- SIP Calculator

- PPF Calculator

- HRA Calculator

- Step up SIP Calculator

- Savings Account Interest Calculator

- Lump sum Calculator

- FD Calculator

- RD Calculator

- Car Loan EMI Calculator

- Bike Loan EMI Calculator

- Sukanya Samriddhi Calculator

- Provident Fund Calculator

- Senior Citizen Savings Calculator

- NSC Calculator

- Monthly Income Scheme Calculator

- Mahila Samman Savings Calculator

- Systematic Withdrawal Calculator

- CAGR Calculator

I’d love to hear from you if you have any queries about Personal Finance and Money Management.

JOIN Telegram Group and stay updated with latest Personal Finance News and Topics.

Download our Free Android App – FinCalC to Calculate Income Tax and Interest on various small Saving Schemes in India including PPF, NSC, SIP and lot more.

Follow the Blog and Subscribe to YouTube Channel to stay updated about Personal Finance and Money Management topics.