Debt Mutual Funds are mutual funds that invest your money in debt instruments like corporate bonds, government securities, treasury bills, commercial papers and other money market instruments. They are less risky in nature compared to equity mutual funds, and can give returns anywhere between 6% to 10% based on the type of debt mutual fund you are investing in. Like other mutual funds, Debt Funds are not completely risk free and returns are not always guaranteed. They aim to provide stable returns with lower risk compared to equity funds. Taxation on Debt Mutual Funds is very simple – add the profits in your income and calculate tax as per your income tax slab rates.

Let us understand more about Debt Mutual Funds in detail.

- What is Debt Mutual Funds?

- How Debt Mutual Funds work?

- Types of Debt Mutual Funds

- Summary Table of Debt Mutual Funds

- Debt Mutual Funds Benefits

- Taxation on Debt Mutual Funds

- Returns on Debt Mutual Funds

- Who Should Invest in Debt Mutual Funds?

- Conclusion

- Frequently Asked Questions

- What is a debt mutual fund?

- Can I invest in debt funds via SIP?

What is Debt Mutual Funds?

- Debt Mutual Funds are one of the Types of Mutual Funds that helps you invest in Debt instruments

- These Debt instruments include corporate bonds, government securities, commercial papers, treasury bills (T-Bills) and other money market instruments

- These funds are less risky in nature compared to equity mutual funds, because the main aim of these funds is to protect the capital of investor while providing steady interest rates over a period of time

- The funds are borrowed by companies or entities with a promise of pre decided interest rate

- The returns in Debt Funds can range between 6% to 10% based on the type of Fund selected

- The securities that the Debt Funds invest in has an associated credit rating. Higher the credit rating meaning the fund is less risky and on the other hand, if the fund invest in low rating securities than they are more risky in nature.

- So it is better to check the credit ratings of the instruments in debt funds to know about the risk factor of that fund

How Debt Mutual Funds work?

The working of Debt Funds is quite simple:

- Every Debt Mutual Fund is allocated a fund manager

- The fund manager decides to invest in the securities with required credit rating in order to provide decent returns to the investors and at the same time, protect the capital invested by investor

- When the fund manager invests in securities that have high credit rating, which means the company pays back the interest promised on time, such funds are having low risk in nature

- Where as if there are many securities in Debt Funds having low credit rating, which means the company is not well known for paying back the interest promised, such mutual funds have more risk

- When the interest rate regime is on the higher side and is expected to increase more, the fund manager tries to invest in short term debt instruments

- And when the interest rate regime is on the lower side and expected to decrease with time, the fund manager tries to invest in long term debt instruments

Types of Debt Mutual Funds

There are various types of Debt Mutual Funds which are classified based on the time period for which they invest in debt instruments. Let us now understand each of them in detail:

Dynamic Bond Funds

Dynamic Bond funds are the type of Debt Fund that invest in a mix of low and high credit rating debt instruments. As the name suggest, they have dynamic, meaning a mix of debt instruments which invest in both short term and long term debt instruments and provide average returns on investments

Income Funds

Income funds generally focuses on consistency of returns on investments and usually invest in long term debt instruments. These are less risky compared to dynamic bond fund. The maturity period of debt instruments these funds invest in can range between 5 years to six years, in order to provide consistent returns from investment. Income funds provide regular income and are also called regular income mutual funds.

Short Term Debt Funds

Short Term and Ultra short term Debt Fund invest in short term debt instruments that have the maturity period between 1 year to 3 years. These are good for conservative investors who don’t want to take much risk and need their capital to be protected.

Liquid Funds

Liquid Mutual Funds invests in debt instruments with maturity not more than 91 days. So for your very short term goals of 3 months, you can park your money in liquid funds compared to keeping it in savings account, to earn you better returns from Liquid mutual fund. Some companies also provide instant redemption in case you need the funds for emergency.

Gilt Funds

Gilt funds invest in government securities and are less risky in nature, since government will not default on the payment of interest on the borrowed capital to meet their needs. So Gilt funds are ideal for risk-averse investors to get fixed income from investments

Credit Opportunities Fund

Credit opportunities fund tries to invest in low credit rating debt instruments in an attempt to maximize the returns from investments. These are more risky in nature since they invest in debt instruments of companies having low credit rating, but the returns can be on the higher side compared to other debt funds

Fixed Maturity Plans

Fixed maturity plans are the type of Debt Mutual Fund that invest in debt instruments having fixed maturity period. These are closed ended funds and often have lock in period of months or years. These invests in fixed income instruments like corporate bonds or government securities. You invest during the initial phase and than have a lock in period based on the debt instruments elected. It is similar to investing in fixed deposits while getting better returns for the risk taken.

So these are some of the types of debt funds. Below is the table showing summary of types of debt mutual funds:

Summary Table of Debt Mutual Funds

| Fund Type | Description | Ideal For |

|---|---|---|

| Liquid Funds | Invest in instruments with ≤91 days maturity | Emergency corpus, short-term |

| Overnight Funds | Invest in 1-day maturity instruments | Ultra-short holding |

| Ultra Short Duration | Maturity between 3–6 months | Low-risk short-term goals |

| Low Duration Funds | Maturity between 6–12 months | Stable short-term returns |

| Short Duration Funds | Maturity between 1–3 years | Moderate risk investors |

| Medium Duration Funds | Maturity between 3–4 years | Balanced risk-return |

| Long Duration Funds | Maturity >7 years | Long-term conservative investors |

| Gilt Funds | Invest in government securities only | Zero credit risk seekers |

| Corporate Bond Funds | ≥80% in high-rated corporate bonds | Safety + returns |

| Credit Risk Funds | ≥65% in lower-rated bonds | High-risk, high-return seekers |

| Banking & PSU Funds | ≥80% in bonds from banks/PSUs | Safety-focused investors |

| Dynamic Bond Funds | Flexible maturity based on interest rate outlook | Interest rate speculators |

| Floater Funds | ≥65% in floating rate instruments | Interest rate hedge |

Debt Mutual Funds Benefits

Let us now go through some of the Benefits of Debt Funds:

- Low Risk Mutual Funds: Since Debt Funds invest in debt instruments, they are having less risk compared to equity mutual funds. But they are more risky than Fixed Deposits since they also invest in some low credit rating debt instruments

- Returns: You can get better returns while investing in Debt Mutual Funds compared to Savings Account or Fixed Deposits

- Cost: The expense ratio, that is the cost taken by fund manager of mutual fund to manage your fund is low in Debt Funds compared to Equity Mutual funds

- Financial Goals: You can meet your short term to medium term goals between 3 months to 3 years based on the types of Debt Mutual Fund selected for investment, and have better returns than simply parking your money in savings account. So you can achieve your short term and medium terms goals using Debt Funds

Taxation on Debt Mutual Funds

There are two types of capital gains when investing in Debt Funds:

- Short Term Capital Gains (STCG): When the holding period of Debt Funds is 3 years or less

- Long Term Capital Gains (LTCG): When the holding period of Debt Funds is more than 3 years

After 1st April 2023, both STCG and LTCG will be taxed as per your slab rates after adding profits from Debt Mutual Funds in your income. This taxation is purely for Debt Funds, have less than 35% allocation in equity.

In case the fund contains equity portion between 35% to 65% of total assets, than for STCG, the tax will be as per slab rate and for LTCG, tax will be 20% with indexation benefit. So it depends on the composition of the mutual fund.

In short, after 1st April 2023, all gains from Debt Mutual Funds will be taxed as per the income tax slab rates.

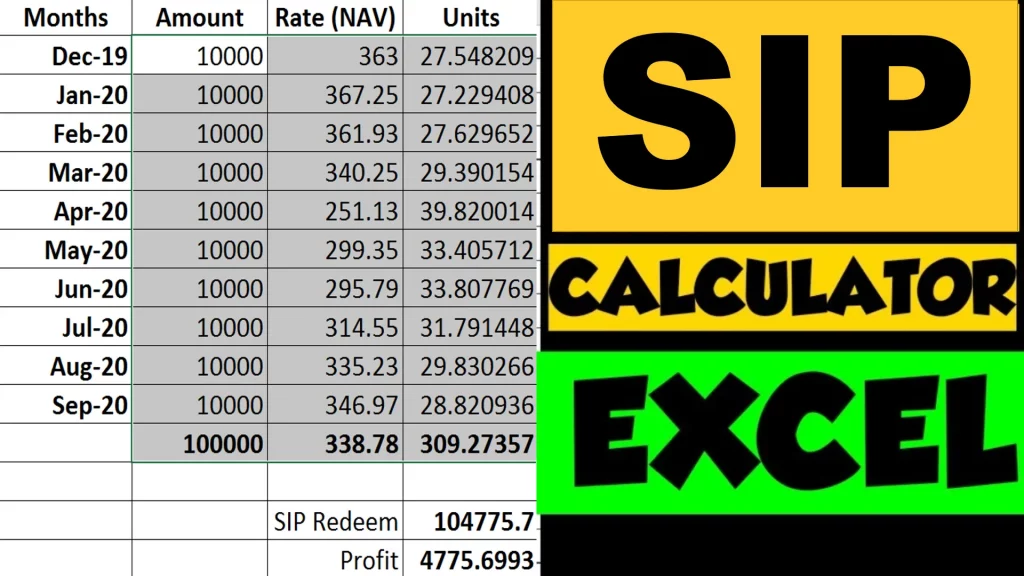

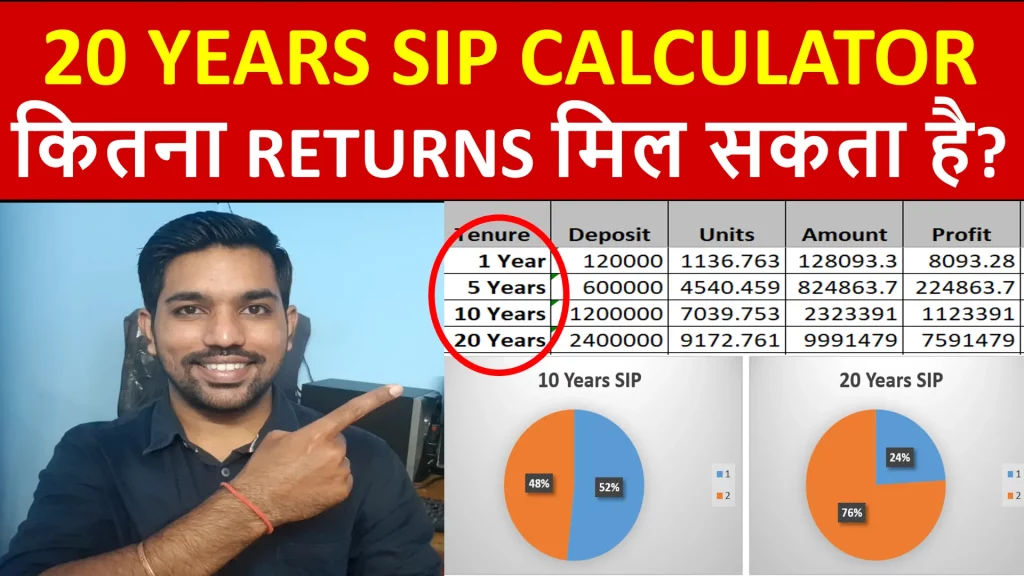

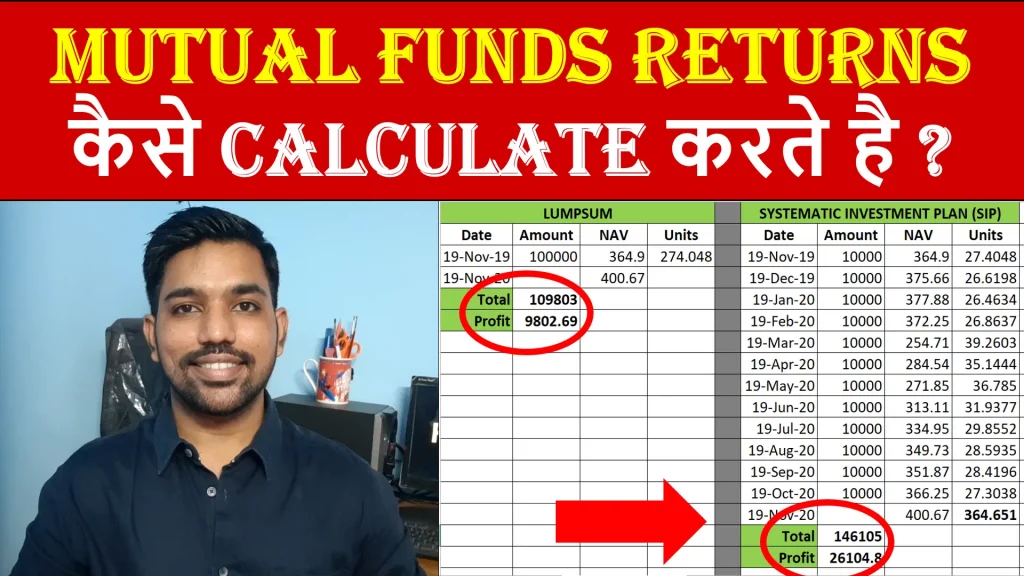

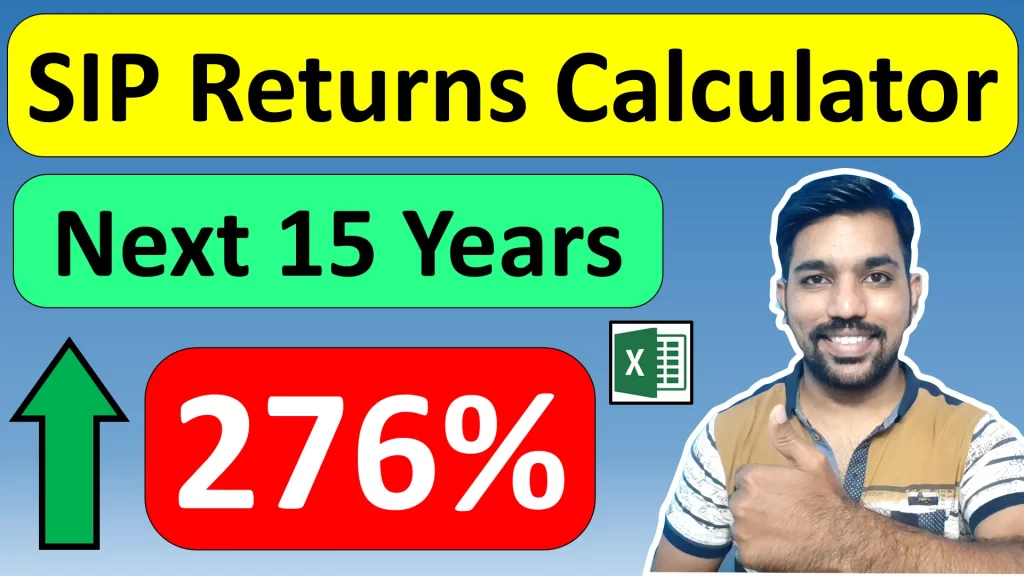

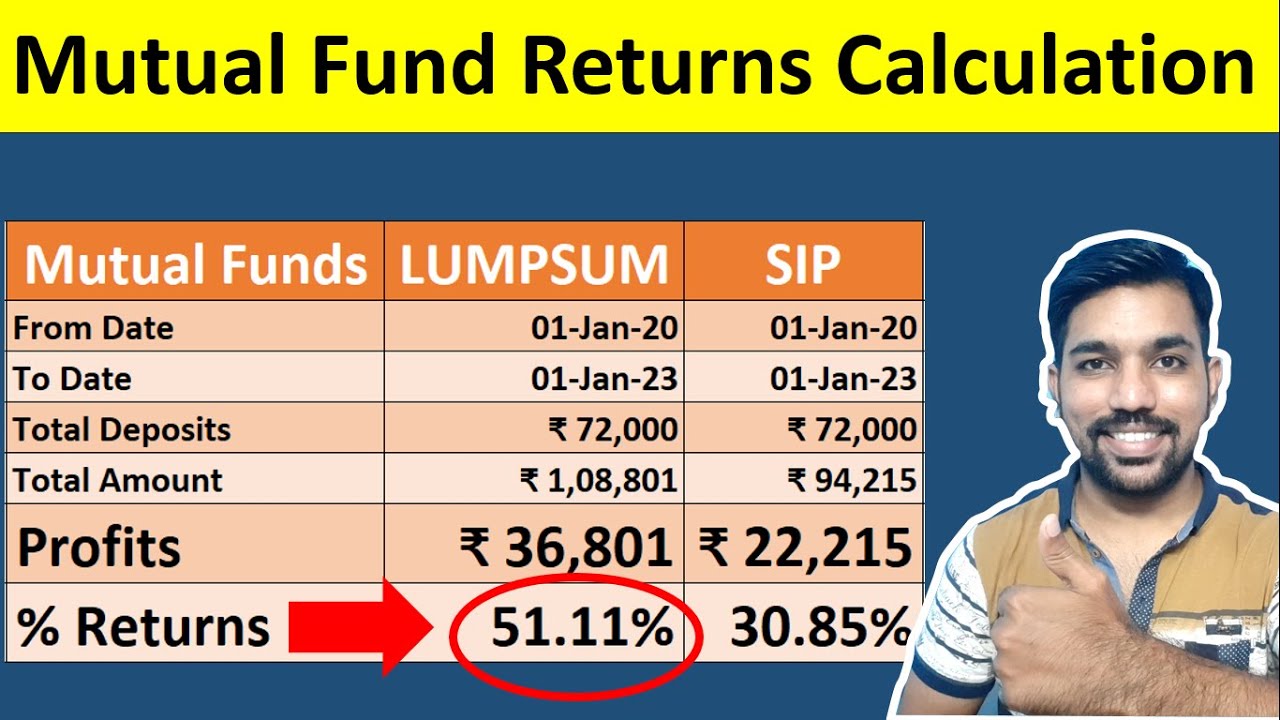

Returns on Debt Mutual Funds

You can get good returns in Debt Mutual Funds between 6% to 10% based on the type of fund selected. Below is the video on Lump sum investment returns calculation in any mutual fund:

Watch more Videos on YouTube Channel

Also, if you are an aggressive investor and want some exposure to equities along with debt instruments, you can consider investing in Hybrid Mutual Fund that invest in both these asset classes to diversify your investments and get better returns compared to a debt fund.

Who Should Invest in Debt Mutual Funds?

- Retirees seeking regular income

- Risk-averse investors avoiding equity volatility

- Short-term goal planners (vacation, car, emergency fund)

- Investors looking to diversify their portfolio

Conclusion

So Debt Mutual Funds invest in Debt instruments to provide decent returns on investment and protect your capital amount as well based on the investment horizon. There are different types of Debt Funds we have discussed that are usually classified based on the maturity period of the underlying debt instruments in that fund.

Also, after 1st April 2023, taxation on Debt Funds will quite simple. The STCG and LTCG capital gains need to be added in your income and taxed as per your income tax slab rates.

Some more Reading:

- 5 Habits of Rich People That will CHange your Life

- Rs. 1000 Mutual Fund Returns Calculation for 15 Years

- Types of Life Insurance in India

Frequently Asked Questions

What is a debt mutual fund?

A debt mutual fund invests in fixed-income instruments like bonds and treasury bills to offer stable returns with lower risk.

What are the 4 types of mutual funds?

The 4 types of mutual funds are Equity Mutual Funds, Debt Mutual Funds, Hybrid Mutual Funds and Money market funds. We have discussed Debt Funds in this article in detail.

Which is better FD or debt mutual fund?

It depends on your goal. If your goal is for more than 1 year and less than 3 years, it is better to invest in Debt mutual fund like short term debt funds to get better returns. If returns is not the concern and you need to be sure that your invested capital is 100% safe, than you should choose fixed deposits, since debt funds are not completely risk free when it comes to saving your principal amount invested. It has certain risk to some extent based on the type of debt mutual fund selected.

How safe is debt mutual fund?

Debt mutual fund has low risk compared to equity mutual funds, since debt funds invest in debt instruments like corporate bonds, treasury bills, commercial papers, etc. Now the debt instruments is associated with credit rating, higher credit rating meaning debt fund is less risky compared to low credit rating debt instruments. So Debt mutual fund has low risk to some extent.

Can I invest in debt funds via SIP?

Yes. SIPs are available for most debt funds and help build disciplined investing habits.

Can I withdraw money from debt fund?

Yes you can withdraw money anytime in debt fund, provided you don’t make losses!

Save Home Loan Interest Amount!

Use Home Loan Excel Calculator that will help you to Save Interest Amount on Home Loan EMI.

Click below button to download Home Loan EMI and Prepayment Calculator in Excel:

Watch how Home Loan Calculator in Excel Works

Income Tax Calculator App – FinCalC

For Income Tax Calculation on your mobile device, you can Download my Android App “FinCalC” which I have developed for you to make your income tax calculation easy.

What you can do with this mobile App?

- Calculate Income Tax for FY 2025-26 and previous FY 2024-25

- Enter estimated Investments to check income tax with Old and New Tax Regime

- Save income tax details and track regularly

- Know how much to invest more to save income tax

- More calculators including PPF, SIP returns, Savings account interest and lot more

Use Popular Calculators:

- Income Tax Calculator

- Home Loan EMI Calculator

- SIP Calculator

- PPF Calculator

- HRA Calculator

- Step up SIP Calculator

- Savings Account Interest Calculator

- Lump sum Calculator

- FD Calculator

- RD Calculator

- Car Loan EMI Calculator

- Bike Loan EMI Calculator

- Sukanya Samriddhi Calculator

- Provident Fund Calculator

- Senior Citizen Savings Calculator

- NSC Calculator

- Monthly Income Scheme Calculator

- Mahila Samman Savings Calculator

- Systematic Withdrawal Calculator

- CAGR Calculator

I’d love to hear from you if you have any queries about Personal Finance and Money Management.

JOIN Telegram Group and stay updated with latest Personal Finance News and Topics.

Download our Free Android App – FinCalC to Calculate Income Tax and Interest on various small Saving Schemes in India including PPF, NSC, SIP and lot more.

Follow the Blog and Subscribe to YouTube Channel to stay updated about Personal Finance and Money Management topics.