Every July, lakhs of salaried employees open the income tax portal, see a list of ITR forms, pick one that looks familiar, and submit their return. Weeks later, some of them receive a defective return notice from the Income Tax Department asking them to refile with the correct form.

Picking the wrong ITR form is the single most common reason a return gets flagged as defective under Section 139(9) and bounced back by the Centralised Processing Centre (CPC). The seven ITR forms are not interchangeable.

And for AY 2026-27, there is an additional consequence most people do not know about — your form now decides your deadline too. ITR-1 and ITR-2 filers must file by 31st July 2026. ITR-3 and ITR-4 non-audit filers get an extra month, until 31st August 2026.

This article will help you identify the correct form in five minutes also with comparison of ITR-1 vs ITR-2 vs ITR-3 vs ITR-4 — with clear eligibility conditions, examples, and a quick decision guide at the end.

You can also download the Income Tax Calculator in Excel using below button to calculate your Income Tax based on Salary, STCG (Short Term Capital Gains), LTCG (Long Term Capital Gains):

- What Changed for AY 2026-27 – Read This First

- How to File ITR 1 Online on Salary – WATCH VIDEO

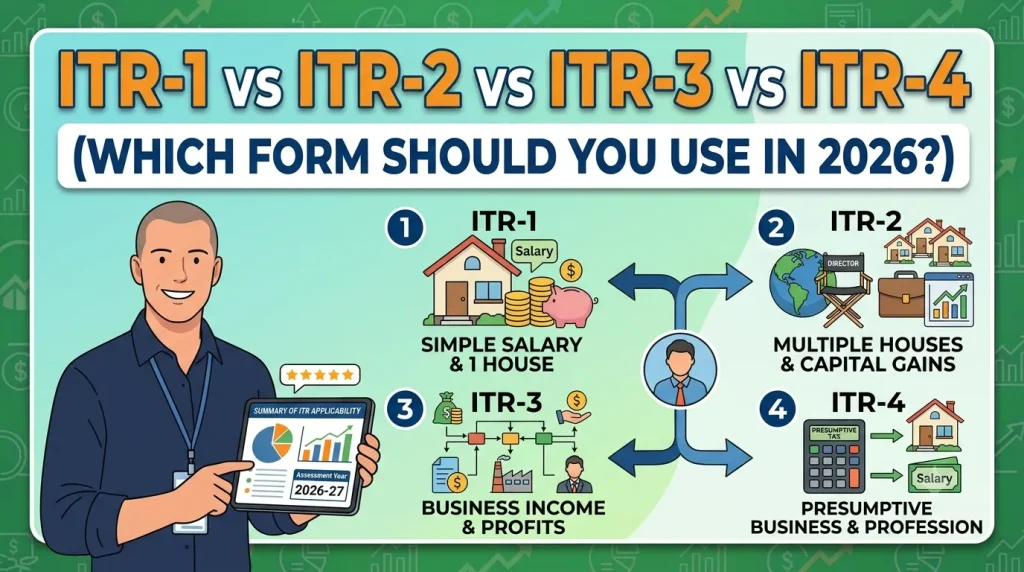

- ITR-1 (Sahaj) – For Most Salaried Employees

- ITR-2 – For Investors and High Earners

- ITR-3 – For Business Owners, F&O Traders and Professionals

- Income Tax Calculation VIDEO – Rs. 5 Lakh to 20 Lakh Examples

- ITR-4 (Sugam) – For Small Businesses and Freelancers Under Presumptive Taxation

- Quick Comparison Table – ITR-1 vs ITR-2 vs ITR-3 vs ITR-4

- Quick Decision Guide – Which Form is Right for You?

- Common Mistakes to Avoid While Selecting ITR Form

- Frequently Asked Questions on ITR Form Selection

What Changed for AY 2026-27 – Read This First

Before you assume the same form you filed last year still applies, check these two important changes CBDT introduced for AY 2026-27:

Two changes for AY 2026-27 have widened who can use the simplest form, ITR-1:

- Up to two house properties can now be reported in ITR-1. Earlier, owning more than one house pushed you into ITR-2.

This means some taxpayers who were filing ITR-2 last year because of a second property or a small mutual fund redemption can now use the simpler ITR-1 for AY 2026-27. If that is you — this is good news.

How to File ITR 1 Online on Salary – WATCH VIDEO

Watch more Videos on YouTube Channel

ITR-1 (Sahaj) – For Most Salaried Employees

ITR-1 is the simplest form and the one most salaried employees in India should be using.

You can file ITR-1 if:

- You are a resident individual (not NRI or RNOR)

- Total income does not exceed Rs. 50 Lakh

- Income is from salary or pension

- Income from up to 2 house properties

- Interest income from savings account, FD, recurring deposits

- Dividend income from stocks or mutual funds

- Long-term capital gains under Section 112A up to Rs. 1.25 Lakh — with no carry-forward capital losses

You cannot use ITR-1 if: ITR-1 is barred, even below Rs. 50 Lakh, for a taxpayer who:

- Is a non-resident or RNOR

- Has any income from business or profession, including F&O or intraday trading

- Has taxable capital gains other than Section 112A long-term gains up to Rs. 1.25 Lakh, including short-term gains

- Has income from crypto or other virtual digital assets

Filing deadline: 31st July 2026

Below is an example to understand when to file ITR 1:

Example: Priya earns a salary of Rs. 14 Lakh, has one self-occupied flat and one rented flat, and earned Rs. 40,000 FD interest. With no other income heads and total income below Rs. 50 Lakh, ITR-1 is the correct form.

ITR-2 – For Investors and High Earners

ITR-2 is one step above ITR-1. It is for individuals and HUFs who have more complex income — capital gains, multiple properties, foreign assets — but no business or professional income.

You should file ITR-2 if: File ITR-2 if you have no business income and any of the following applies:

- Capital gains from equity, mutual funds, real estate, bonds, or other capital assets — short-term or long-term, and any amount of Section 112A LTCG above Rs. 1.25 Lakh

- More than two house properties

- Foreign income or foreign assets, including ESOPs in a foreign parent, overseas bank accounts, or foreign mutual funds

- Total income exceeds Rs. 50 Lakh with no business income

- NRIs and RNOR taxpayers must use ITR-2 (or ITR-3 if they have business income) — they cannot use ITR-1 or ITR-4

- Crypto income (VDA — Virtual Digital Assets) must be declared in ITR-2 if there is no business income

You cannot use ITR-2 if you have any income from business or profession — in that case ITR-3 is required.

One useful point: if you are eligible for the simpler ITR-1, you can still choose ITR-2, but there is rarely a reason to. ITR-1 is shorter, more pre-filled, and quicker. Always use the simplest form that fully fits your income profile.

Filing deadline: 31st July 2026

Below is an example to understand when to file ITR 2:

Example: Meera earns a salary of Rs. 22 Lakh and sold mutual fund units with Rs. 3 Lakh in LTCG. Since the gains exceed the Rs. 1.25 Lakh ITR-1 limit, she must file ITR-2.

ALSO READ: What is AIS Document in Income Tax Return

ITR-3 – For Business Owners, F&O Traders and Professionals

ITR-3 is the most comprehensive individual ITR form. If you run a business, trade in F&O, are a freelancing professional maintaining full books of accounts, or are a partner in a firm — ITR-3 is your form.

You should file ITR-3 if:

- You have income from a proprietorship business

- You are a doctor, lawyer, architect, consultant, or other professional in independent practice maintaining full books

- You do F&O trading or intraday trading — these are treated as business income

- You are a director in a company with business income

- Your business turnover exceeds Rs. 2 Crore (above the presumptive scheme limit)

From AY 2026-27, ITR-3 includes a dedicated section for F&O trading income, requiring separate disclosure of F&O turnover and profit/loss in the P&L schedule. Previously, F&O income was often buried in general business income. This enhanced disclosure is aimed at improving the department’s ability to track derivatives trading income and cross-match it with exchange data.

Important for F&O traders: Many F&O traders skip filing altogether if they made a net loss, believing there is no tax to pay. This is a mistake. F&O losses must be reported in ITR-3 to be eligible for carry-forward — you can carry forward business losses for 8 years and set them off against future F&O profits. If you do not file on time, the right to carry forward the loss is forfeited.

ITR-3 also accommodates all other income types — salary, house property, capital gains, and foreign assets — alongside business income, making it the most flexible individual ITR form.

Filing deadline: 31st August 2026 (non-audit) | 31st October 2026 (audit cases)

Income Tax Calculation VIDEO – Rs. 5 Lakh to 20 Lakh Examples

ITR-4 (Sugam) – For Small Businesses and Freelancers Under Presumptive Taxation

ITR-4 is the simplified business form designed for small businesses, traders, and professionals who do not want to maintain detailed books of accounts and instead opt for the presumptive taxation scheme.

You can file ITR-4 if:

- You are a resident individual, HUF, or firm (not LLP)

- Total income does not exceed Rs. 50 Lakh

- You opt for presumptive taxation under:

- Section 44AD — traders and manufacturers with turnover up to Rs. 2 Crore (or Rs. 3 Crore if 95%+ receipts are digital)

- Section 44ADA — professionals including freelancers, consultants, doctors, architects with gross receipts up to Rs. 50 Lakh (or Rs. 75 Lakh if 95%+ receipts are digital)

- Section 44AE — goods transport vehicle owners

- You also have income from up to 2 house properties and LTCG under Section 112A up to Rs. 1.25 Lakh (new for AY 2026-27)

Under presumptive taxation, your income is assumed at a fixed percentage — 8% or 6% of turnover under 44AD, and 50% of gross receipts under 44ADA — without needing to maintain detailed profit and loss accounts. This is why ITR-4 is significantly simpler to file than ITR-3.

You cannot use ITR-4 if:

- You are an NRI

- You have F&O or intraday trading income — this is not eligible under presumptive taxation

- If gross receipts in FY 2025-26 crossed Rs. 50 Lakh (even as a consultant under 44ADA), you cannot use ITR-4 — file ITR-3 instead

- You have brought forward losses to carry forward

From AY 2026-27, taxpayers filing ITR-4 must disclose investments made during the year in the Financial Particulars section. This is a new transparency requirement aimed at cross-checking declared income against the investment capacity of the business.

Filing deadline: 31st August 2026 (non-audit)

Example: Rohan bills Rs. 28 Lakh in professional receipts as a freelance consultant. Under Section 44ADA he offers 50% (Rs. 14 Lakh) as deemed income, keeps no detailed books, and files ITR-4 Sugam.

ALSO READ: How to File ITR 1 Online – Complete Beginners

Quick Comparison Table – ITR-1 vs ITR-2 vs ITR-3 vs ITR-4

| Items | ITR-1 | ITR-2 | ITR-3 | ITR-4 |

|---|---|---|---|---|

| Salary income | Yes | Yes | Yes | Yes |

| Capital gains (small LTCG) | Up to Rs. 1.25L | All types | All types | Up to Rs. 1.25L |

| House properties | Up to 2 | Any number | Any number | Up to 2 |

| Business income | No | No | Yes | Yes (presumptive) |

| F&O trading | No | No | Yes | No |

| Foreign assets | No | Yes | Yes | No |

| NRI / RNOR | No | Yes | Yes | No |

| Directors | No | Yes | Yes | No |

| Income limit | Rs. 50L | No limit | No limit | Rs. 50L |

| Due date | 31 Jul 2026 | 31 Jul 2026 | 31 Aug 2026 | 31 Aug 2026 |

Quick Decision Guide – Which Form is Right for You?

Answer these questions in order:

Question 1: Do you have any income from business, profession, F&O trading, or freelancing?

- Yes → Go to Question 2

- No → Go to Question 3

Question 2: Do you maintain full books of accounts, or is your turnover/receipts above the presumptive limit?

- Yes → ITR-3

- No (and you qualify for presumptive scheme) → ITR-4

Question 3: Do you have capital gains above Rs. 1.25 Lakh (or any short-term gains), foreign income, foreign assets, more than 2 properties, or income above Rs. 50 Lakh?

- Yes → ITR-2

- No → ITR-1

Common Mistakes to Avoid While Selecting ITR Form

Filing ITR-1 despite short-term gains or Section 112A gains above Rs. 1.25 Lakh — a common cause of defective returns. Using ITR-4 for F&O or intraday trading — not eligible presumptive income.

- Assuming last year’s form still applies — two major eligibility changes happened in AY 2026-27 (two house properties and small LTCG now allowed in ITR-1)

- Filing ITR-4 and declaring income below the presumptive rate — if you declare less than the minimum presumptive rate, you may be required to maintain full books of account and switch to ITR-3 with a possible audit requirement

- Salaried individual with a side consulting project using ITR-1 — any professional or freelance income, even small, moves you to ITR-3 or ITR-4. ITR-1 is strictly for those with no business or professional income

ALSO READ: 7 Mistakes to avoid while Filing ITR

Frequently Asked Questions on ITR Form Selection

Which ITR form should a salaried employee file for AY 2026-27?

Most salaried employees with income below Rs. 50 Lakh, no capital gains above Rs. 1.25 Lakh, and no business income should file ITR-1. If you have mutual fund or stock capital gains above this limit, use ITR-2.

Which ITR form is for F&O traders?

F&O trading income is treated as business income. F&O traders must file ITR-3, regardless of whether they made a profit or loss. ITR-4 is not eligible for F&O trading.

Can I file ITR-2 even if I am eligible for ITR-1?

Yes — you are allowed to file a higher form than required. But there is no benefit to doing so. ITR-1 is simpler, faster, and more pre-filled. Use ITR-1 if you are eligible.

What happens if I file the wrong ITR form?

The Income Tax Department issues a defective return notice under Section 139(9), and you must refile correctly within the given time or the return is treated as invalid.

Which form should a freelancer use?

If your gross receipts are below Rs. 50 Lakh (or Rs. 75 Lakh with 95%+ digital receipts) and you opt for the 50% presumptive deduction under Section 44ADA, use ITR-4. If you maintain full books or exceed the limit, use ITR-3.

So we discussed about ITR-1 vs ITR-2 vs ITR-3 vs ITR-4 in this article.

Getting your ITR form right is the foundation of a clean, compliant return. Before you open the income tax portal this July, spend five minutes on this decision — it determines your form, your deadline, and whether your return gets processed smoothly or bounced back with a defective notice. Use the income tax calculator on this page to calculate your tax liability first, then use the decision guide above to confirm the right form before you begin filing.

Save Home Loan Interest Amount!

Use Home Loan Excel Calculator that will help you to Save Interest Amount on Home Loan EMI.

Click below button to download Home Loan EMI and Prepayment Calculator in Excel:

Watch how Home Loan Calculator in Excel Works

Income Tax Calculator App – FinCalC

For Income Tax Calculation on your mobile device, you can Download my Android App “FinCalC” which I have developed for you to make your income tax calculation easy.

What you can do with this mobile App?

- Calculate Income Tax for FY 2025-26 and previous FY 2024-25

- Enter estimated Investments to check income tax with Old and New Tax Regime

- Save income tax details and track regularly

- Know how much to invest more to save income tax

- More calculators including PPF, SIP returns, Savings account interest and lot more

Use Popular Calculators:

- Income Tax Calculator

- Home Loan EMI Calculator

- SIP Calculator

- PPF Calculator

- HRA Calculator

- Step up SIP Calculator

- Savings Account Interest Calculator

- Lump sum Calculator

- FD Calculator

- RD Calculator

- Car Loan EMI Calculator

- Bike Loan EMI Calculator

- Sukanya Samriddhi Calculator

- Provident Fund Calculator

- Senior Citizen Savings Calculator

- NSC Calculator

- Monthly Income Scheme Calculator

- Mahila Samman Savings Calculator

- Systematic Withdrawal Calculator

- CAGR Calculator

I’d love to hear from you if you have any queries about Personal Finance and Money Management.

JOIN Telegram Group and stay updated with latest Personal Finance News and Topics.

Download our Free Android App – FinCalC to Calculate Income Tax and Interest on various small Saving Schemes in India including PPF, NSC, SIP and lot more.

Follow the Blog and Subscribe to YouTube Channel to stay updated about Personal Finance and Money Management topics.