Are you confused between prepaying your home loan or investing in mutual funds with surplus amount you have? While mutual funds promise higher returns, they are subject to market volatility and economic fluctuations. Prepaying your home loan, however, offers guaranteed savings and the priceless benefit of becoming debt‑free sooner. Understanding the trade‑offs between these two strategies can help you make a smarter financial decision that aligns with your long‑term financial goals, peace of mind and financial security.

You can download the Home Loan Excel Calculator with Prepayment Option using below button:

Home Loan Prepayment vs Mutual Fund Investing Video

Watch more Videos on YouTube Channel

Should your Prepay Home Loan or Invest in Mutual Funds

Below are some key points whether you should prepay the home loan or invest the surplus amount in mutual funds via SIP or lumpsum investing:

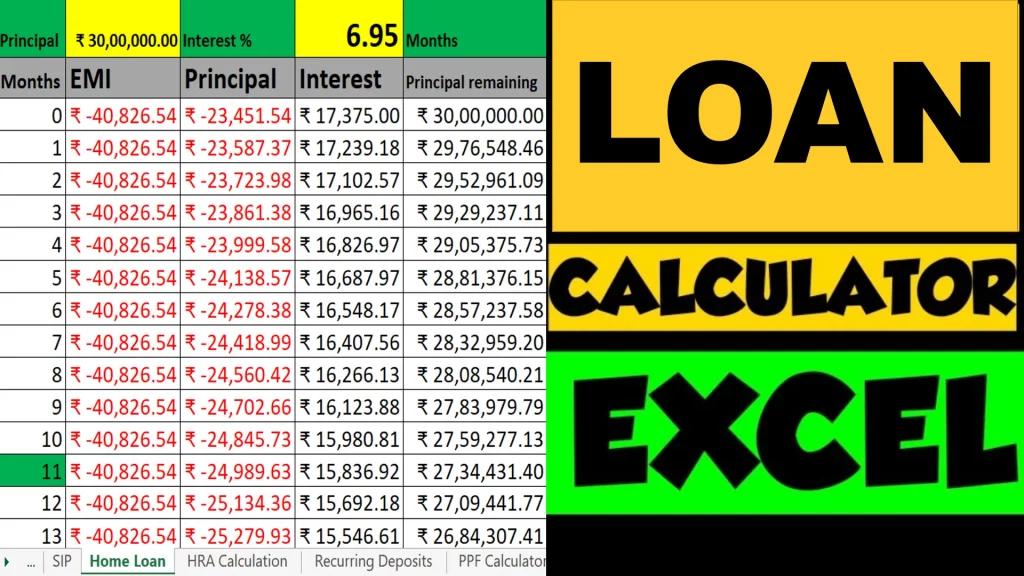

- Prepaying Home Loan guarantees savings – Example: Prepaying ₹2 lakh in the 5th year of a ₹40 lakh loan can save ₹3–4 lakh in interest, a benefit that is certain, unlike mutual funds where returns are uncertain due to market volatility.

- Debt‑free living ensures financial security – Prepayment reduces EMI stress, shortens tenure, and gives instant peace of mind, something investments cannot guarantee in the short term.

- Mutual Funds carry risk and uncertainty – While equity funds may deliver 10–12% historically, returns fluctuate with economic conditions, global sentiments, and market volatility, making them unreliable compared to the assured benefit of loan prepayment.

- Peace of mind vs. chasing returns – Even if mutual funds average 12% returns, closing a 9% home loan early provides guaranteed relief and freedom from debt, which often outweighs potential but uncertain gains.

- Liquidity vs. security – Mutual funds offer liquidity, but prepayment secures your future by reducing liabilities and freeing up cash flow permanently.

- Risk factor favors prepayment – Mutual funds expose you to market risk, while prepayment is a risk‑free strategy with guaranteed financial benefit.

- Tax benefits tilt toward loans – Section 24 interest deduction (especially for let‑out property) continues even under the new regime apart from old tax regime, while ELSS mutual fund deductions under Section 80C are limited to the old regime.

- Hybrid strategy with prepayment focus – Prepaying part of the loan reduces debt gradually, while limited mutual fund investment can support long‑term wealth, ensuring balance but prioritizing debt freedom.

- Age and goals matter – Senior citizens and risk‑averse individuals benefit more from prepayment, while younger earners may experiment with investments, but debt‑free living remains universally valuable for all age groups

- Financial discipline through prepayment – Regular prepayments gradually reduces principal remaining balance in loan account, ensuring guaranteed progress toward debt‑free living

- Personalized but safer choice – Evaluating risk appetite and goals often shows prepayment as the more secure, stress‑free option compared to uncertain mutual fund returns.

In short: Prepaying your home loan is a guaranteed path to peace of mind and financial freedom, while mutual fund investing carries risks and uncertainties that may not align with everyone’s comfort level. A strategy involving combination of both can also be utilized to prepay the loans gradually and also to build wealth via SIP Investments in mutual funds with the surplus amount you have.

Why Home Loan Prepayment is Better?

Below are few key points to understand why Home Loan Prepayment in better for you:

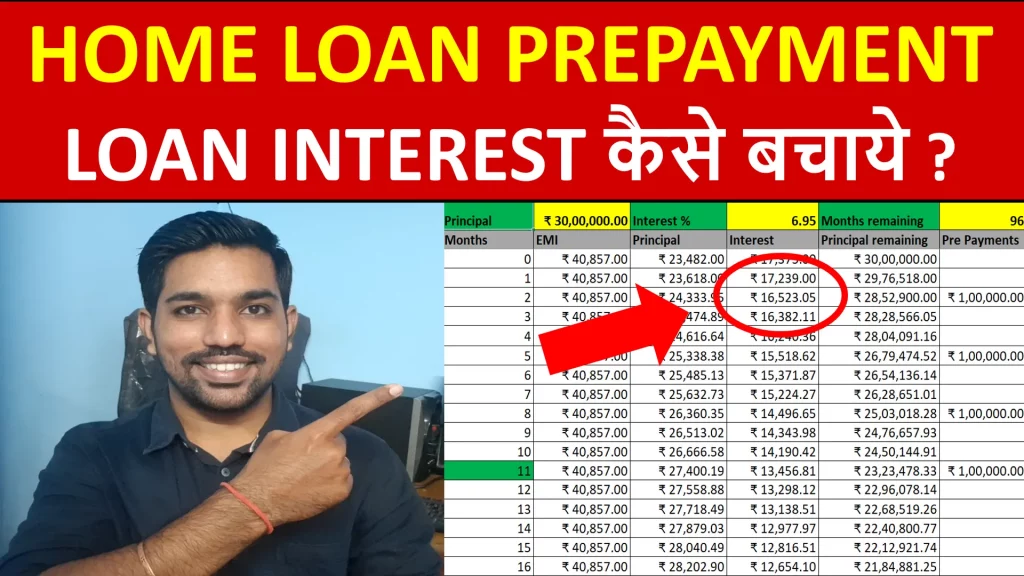

- Guaranteed Interest Savings – Every rupee used for prepayment or part payment directly reduces your outstanding principal balance in the home loan, cutting down future interest costs. Example: Prepaying ₹2 lakh early in a ₹40 lakh loan can save ₹3–4 lakh in interest over the tenure.

- Debt‑Free Living – Loan Prepayment shortens the loan tenure and lowers EMI stress, giving you peace of mind and financial freedom much earlier. You can either choose between reducing the loan tenure or reducing the EMI Amount. Reducing loan tenure is better as it save more interest amount compared to reducing the loan EMI amount

- Risk‑Free Strategy – Unlike mutual funds or market investments, prepayment offers guaranteed returns equal to your loan’s interest rate, without exposure to volatility. Your interest amount is saved drastically compared to uncertain returns if invested in mutual funds for short duration

- Improved Cash Flow – With reduced EMIs or a shorter loan term, you free up monthly income for other goals, retirement planning, or emergency needs.

- Tax Efficiency – While Section 24 deductions are useful, the real benefit of prepayment is eliminating long‑term interest outgo, which often outweighs tax savings by keeping the loan for long term

- Financial Discipline & Security – Regular prepayments steadily reduce liabilities by decreasing the principal remaining balance of the loan, ensuring you move closer to debt‑free living and long‑term stability.

So these are some of the benefits of making Home Loan Prepayment in order to close the loan before time and becoming debt-free.

When SIP Investing can be better than Home Loan Prepayment?

Systematic Investment Plans (SIPs) can sometimes be better than home loan prepayment when the loan interest rate is relatively low and the expected returns from equity mutual funds are significantly higher. For example, if your home loan rate is 7% and SIPs are averaging around 12% over the long term, investing may help you build wealth faster. SIPs also provide liquidity, meaning you can withdraw funds in case of emergencies, unlike prepayment where money gets locked into reducing debt. Additionally, SIPs benefit from compounding and rupee cost averaging, making them attractive for younger investors with long horizons.

However, SIP returns are not guaranteed and can fluctuate due to market volatility, global events, and economic conditions. In contrast, prepaying a home loan offers risk‑free, assured savings equal to your loan’s interest rate. For instance, prepaying ₹2 lakh early in a ₹40 lakh loan can save ₹3–4 lakh in interest, a benefit that no SIP investment can guarantee. Ultimately, while SIPs may suit aggressive investors, home loan prepayment remains the safer, more reliable path to peace of mind and debt‑free living.

You can prepay the home loan amount during the inital stages of the loan since majority of the interest is taken from you during the initial months and years of home loan, and start investing more in mutual funds via SIP when the remaining loan tenure is around 12 months to 18 months since you must have paid the interest amount prior to this period.

What is the 5 20 30 40 rule for home loan?

Let us now understand the 5 20 30 40 rule for home loan.

The 5-20-30-40 rule for home loan is a smart guideline for home buyers to avoid financial stress when taking a home loan to buy a property. It sets clear limits on how much you should borrow, how long the loan tenure should be, and how much of your income should go toward EMIs.

- 5x Annual Income The price of the house should not exceed five times your annual income. Example: If your annual income is ₹10 lakh, your home purchase should ideally be capped at ₹50 lakh.

- 20-Year Loan Tenure Keep the loan tenure within 20 years to avoid excessive interest outgo. Longer tenures may reduce EMI but drastically increase total interest paid.

- 30% EMI-to-Income Ratio Your monthly EMI should not exceed 30% of your monthly income. Example: If you earn ₹1 lakh per month, your EMI should be capped at ₹30,000 to maintain financial comfort.

- 40% Savings Rule Ensure that at least 40% of your income is saved or invested after paying EMIs and other expenses. This builds long-term financial stability and prevents over-leverage.

So you can follow above rule of 5 20 30 40 for home loan to be financially stable. Lower the tenure of the home loan will help you to pay less interest amount. Additionally, once the loan tenure is about to end and only 12 to 18 months of EMI is remaining, you can start investing any surplus amounts in mutual funds via SIP to build wealth over long term.

Conclusion

When comparing home loan prepayment with mutual fund investing, the choice ultimately depends on your financial priorities. Mutual funds may offer higher long‑term returns, but they come with market risks and uncertainty. Prepaying a home loan, on the other hand, provides guaranteed savings, reduces long‑term interest burden, and delivers peace of mind by moving you closer to debt‑free living.

For individuals who value security and financial freedom over chasing uncertain returns, home loan prepayment often proves to be the more reliable and rewarding option compared to investing the surplus amount in mutual funds

Some more Reading:

Save Home Loan Interest Amount!

Use Home Loan Excel Calculator that will help you to Save Interest Amount on Home Loan EMI.

Click below button to download Home Loan EMI and Prepayment Calculator in Excel:

Watch how Home Loan Calculator in Excel Works

Income Tax Calculator App – FinCalC

For Income Tax Calculation on your mobile device, you can Download my Android App “FinCalC” which I have developed for you to make your income tax calculation easy.

What you can do with this mobile App?

- Calculate Income Tax for FY 2025-26 and previous FY 2024-25

- Enter estimated Investments to check income tax with Old and New Tax Regime

- Save income tax details and track regularly

- Know how much to invest more to save income tax

- More calculators including PPF, SIP returns, Savings account interest and lot more

Use Popular Calculators:

- Income Tax Calculator

- Home Loan EMI Calculator

- SIP Calculator

- PPF Calculator

- HRA Calculator

- Step up SIP Calculator

- Savings Account Interest Calculator

- Lump sum Calculator

- FD Calculator

- RD Calculator

- Car Loan EMI Calculator

- Bike Loan EMI Calculator

- Sukanya Samriddhi Calculator

- Provident Fund Calculator

- Senior Citizen Savings Calculator

- NSC Calculator

- Monthly Income Scheme Calculator

- Mahila Samman Savings Calculator

- Systematic Withdrawal Calculator

- CAGR Calculator

I’d love to hear from you if you have any queries about Personal Finance and Money Management.

JOIN Telegram Group and stay updated with latest Personal Finance News and Topics.

Download our Free Android App – FinCalC to Calculate Income Tax and Interest on various small Saving Schemes in India including PPF, NSC, SIP and lot more.

Follow the Blog and Subscribe to YouTube Channel to stay updated about Personal Finance and Money Management topics.