Home Loan Prepayment is a way to reduce the remaining Principal Balance in your Loan account that helps you to save loan interest amount over long term and also reduce the Loan Tenure. Even paying just two extra EMIs every year could cut your 15‑year loan down to about 11 years, helping you become debt‑free much faster than you imagined. Small steps today can create massive financial freedom tomorrow.

Home Loan Prepayment (Part Payment) Video

Watch more Videos on YouTube Channel

What is Home Loan Prepayment?

- Home loan prepayment means paying off your loan (partially or fully) before the scheduled EMI tenure ends. This means you reduce the principal remaining balance in your loan account to close the Home Loan before time

- Impact on principal: Extra payments directly reduce the outstanding principal amount of your home loan

- Interest savings: Lower principal means reduced interest burden over time, thus prepayment or part payment helps you to save the home loan interest

- Tenure reduction: Prepayment can shorten the loan duration significantly – just with 1 extra prepayment in a year, you can save 2-3 months of EMI of future thus reducing your loan tenure

- Best timing: Home Loan Prepayment is most beneficial in the early years of the loan when interest outgo is highest and the principal remaining balance is also high. The interest calculation works on reducing balance of the principal amount in your home loan

- Charges: Some lenders apply prepayment penalties when the loan is of fixed interest rate, but floating-rate home loans often have no charges

- Documentation: Loan Part payment usually requires a written request (a form to be filled), bank statement of last 3 months, a cheque and lender’s approval for prepayment

- Flexibility: Borrowers can choose between reducing EMI amounts or reducing tenure after prepayment. Reducing tenure helps you save more interest compared to reducing EMI

- Credit profile: Early repayment of home loan improves creditworthiness and reduces your long-term debt obligations, thus improving your credit score as well

- Liquidity check: Ensure you retain enough funds for emergencies before prepaying. Your emergency funds must not me touched just to prepay the loans

- Opportunity cost: Compare loan interest rate vs. potential investment returns before deciding. But if you are during the initial phase of home loan, try to make prepayments whenever possible, and during the ending phase of last 12 months to 18 months, it is better to invest in mutual funds via SIP instead of making prepayments, since there is not much interest amounts that can be saved during the ending phase of home loan

- Financial freedom: While doing loan prepayments, it helps you to achieve debt-free living sooner compared to not doing any prepayments

- Example: Prepaying ₹1 lakh on a ₹50 lakh loan in year 2 can save lakhs in interest and reduce tenure by 2–3 years.

- Considerations: Prepayment may not always be optimal if your loan interest rate is relatively low compared to investment returns in markets (mutual funds or stocks). But it is always better emotionally to be debt free before focusing on increasing your portfolio amount of mutual funds or stocks.

How does home loan prepayment work?

Let us now understand how home loan prepayment or part payment works.

When you take a home loan, your monthly EMI (Equated Monthly Installment) is split into two parts:

- Principal repayment – the actual loan amount you borrowed

- Interest payment – the cost of borrowing

In the early years of the loan, a larger portion of your EMI goes toward interest amount of EMI. As time passes, the share of principal repayment increases. If you make a prepayment, the extra amount you pay, directly reduces the outstanding principal. Since interest is calculated on the reduced principal amount, your future interest outgo drops significantly. Hence prepayment helps you to save lot of interest amount that you pay via EMI every month.

Example

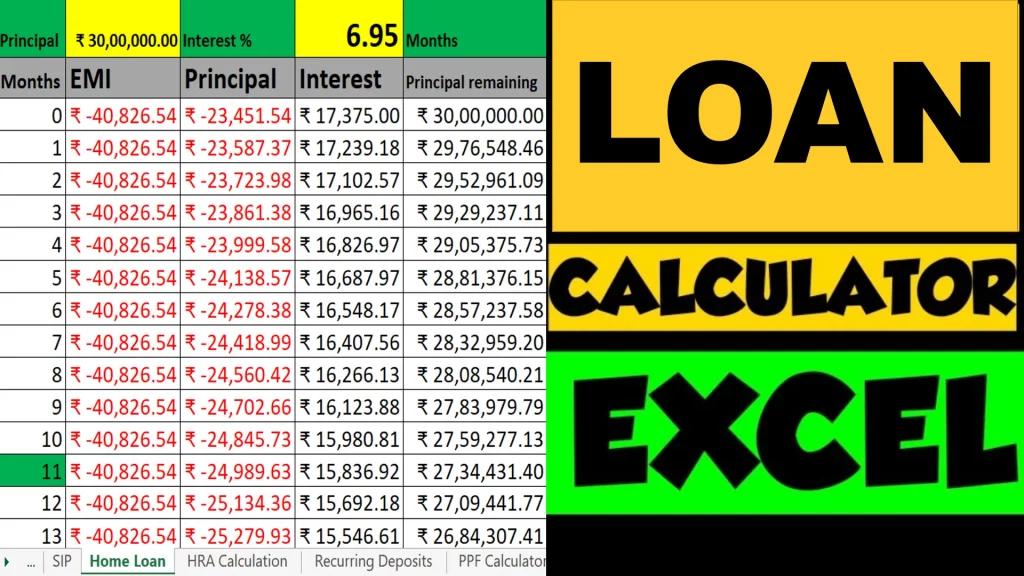

Suppose you take a ₹50 lakh home loan at 8% interest for 20 years.

- Your EMI works out to roughly ₹41,822 per month. (Use Home Loan Calculator Here)

- Over 20 years, you would pay about ₹50 lakh in interest—almost equal to your loan amount.

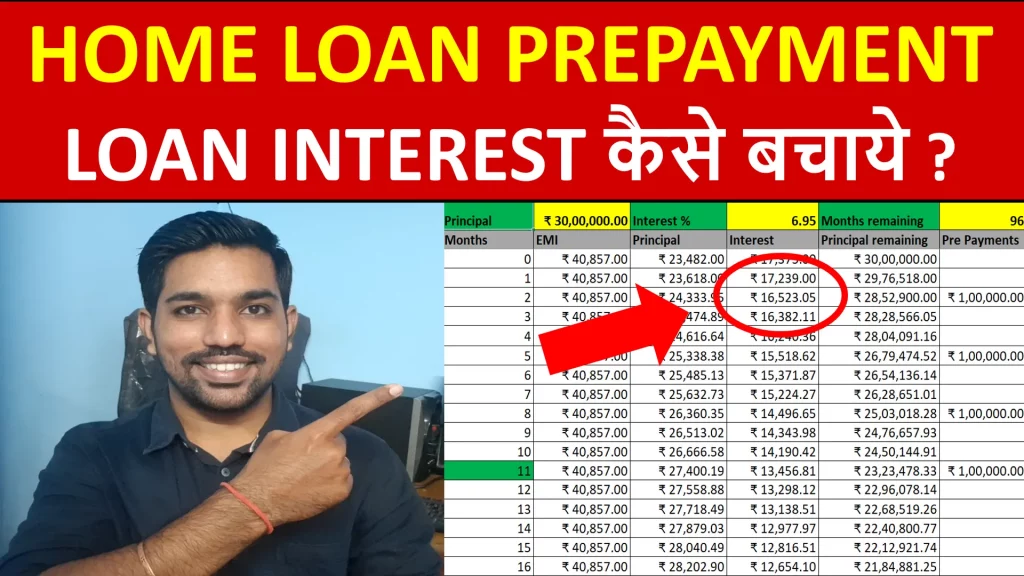

Now imagine you make a part-prepayment of ₹5 lakh in the 5th year:

- Your outstanding principal reduces immediately – This also reduces the interest component of your Loan EMI

- Also, your EMI tenure shortens by about 2–3 years, or you can choose to reduce your EMI amount. It is better to reduce the tenure here and keep EMI same in order to save more interest amount

- You save ₹8–10 lakh in interest over the life of the loan. This savings increases with continuous prepayments over time as and when possible

If you make the same prepayment in the 15th year, the benefit is smaller because most of the interest has already been paid by then. This shows why early prepayment is more impactful, compared to doing same during the later stages of the home loan

You can download the home loan excel calculator at the top of this article to calculate savings on your Home Loan Prepayments

Benefits of Home Loan Prepayment

Let us now see what are the benefits of Home Loan Prepayment:

- Significant Interest Savings: By reducing the outstanding principal amount early, you cut down the total interest payable over the loan tenure. Since interest is calculated on the remaining principal balanceof home loan, even a small prepayment in the initial years can save you lakhs in interest.

- Shorter Loan Tenure: Prepayment allows you to close your loan years earlier than scheduled. Instead of paying EMIs for 20 years, you might finish in 15–17 years, freeing up your income for other financial goals such as retirement planning, child education and travelling

- Reduced EMI Burden: After prepayment, lenders often give you the option to either reduce your EMI amount or shorten the tenure. Lower EMIs ease monthly cash flow, making it easier to manage household expenses. But it is better to keep EMI same and lower the tenure to maximize savings

- Improved Financial Security: Clearing debt faster reduces long-term financial risk. With fewer liabilities, you gain peace of mind and greater flexibility to handle emergencies or invest in new opportunities

- Better Credit Profile: Early repayment improves your creditworthiness. A lower debt-to-income ratio and timely prepayments can boost your credit score, making it easier to qualify for future loans at better interest rates

- Freedom to Reallocate Funds: Once your loan burden reduces, you can redirect funds toward investments, retirement planning, or other wealth-building activities. This accelerates your journey toward financial independence

What happens if I pay 2 EMI extra every year?

If you pay two extra EMIs every year, you are essentially making a prepayment towards your home loan. This accelerates repayment and reduces your overall interest burden. Here’s how it works:

- As mentioned above, each EMI consists of principal + interest. By paying extra EMIs, you directly reduce the outstanding principal faster than scheduled

- Since interest is calculated on the remaining principal balance, lowering it early means you pay less interest in future months

- Over time, this strategy can shorten your loan tenure by several years. For example, on a 20-year loan, paying two extra EMIs annually could help you finish in 15–16 years instead

- The earlier you start this practice, the greater the benefit, because interest outgo is highest in the initial years of your home loan due to high principal balance

- You also gain financial flexibility—lower debt obligations free up income for other goals like investments, retirement, or children’s education

- Importantly, check with your lender about prepayment rules. Most banks allow extra EMI payments without penalty, especially on floating-rate loans, but it’s wise to confirm with the lender or bank

Example: Suppose your EMI is ₹40,000. Paying two extra EMIs per year adds ₹80,000 toward your loan annually. Over 10 years, that’s ₹8 lakh in prepayments, which could save you ₹12–15 lakh in interest and cut your loan tenure by 3–4 years.

In short, paying two extra EMIs every year is a simple yet powerful way to become debt-free faster, close your home loan before time and save a substantial amount in loan interest.

Is prepayment of home loan good or bad?

Home Loan Prepayment is generally good — it reduces interest costs, shortens tenure, and helps you become debt-free faster. It may be less ideal only if your loan interest rate is very low compared to potential investment returns during the later stages of home loan, since your principal remaining balance also decreases with time.

How to clear a 15 year home loan in 5 years?

Here are the 6 steps to clear a 15‑year home loan in just 5 years:

- Make Aggressive Prepayments Early – Channel any surplus income or bonuses directly into prepayments. Doing this in the first few years maximizes interest savings since interest outgo is highest at the start

- Pay Extra EMIs Each Year – Commit to paying at least 2–3 additional EMIs annually. This steadily reduces the principal faster and can shave years off your loan tenure

- Increase EMI Amounts When Income Rises – Instead of sticking to the original EMI, revise it upward whenever your salary or business income grows. Even a 10–20% increase in EMI can drastically cut loan tenure

- Redirect Investments with Lower Returns – If you have funds in low‑yield instruments (like savings accounts or fixed deposits), consider diverting them toward loan prepayment. The guaranteed interest savings often outweigh modest investment returns. But do not touch your emergency funds in this case

- Cut Non‑Essential Expenses & Build a Prepayment Fund – Create a dedicated fund for prepayments by avoiding impulsive spending. Automating transfers into this fund ensures discipline

- Avoid New Debt Commitments – Stay clear of additional loans or credit card debt during this period. Keeping liabilities minimal allows you to focus resources on clearing the home loan aggressively

Conclusion

Home loan prepayment is a smart financial strategy that helps borrowers save substantial interest amount and reduce their loan tenure. By making extra payments early, you accelerate principal reduction, which directly lowers future interest outgo. This not only brings financial freedom sooner but also improves your credit score and overall financial security.

When balanced with liquidity needs and investment opportunities, prepayment can be one of the most effective ways to manage long-term debt.

Some more Reading:

Save Home Loan Interest Amount!

Use Home Loan Excel Calculator that will help you to Save Interest Amount on Home Loan EMI.

Click below button to download Home Loan EMI and Prepayment Calculator in Excel:

Watch how Home Loan Calculator in Excel Works

Income Tax Calculator App – FinCalC

For Income Tax Calculation on your mobile device, you can Download my Android App “FinCalC” which I have developed for you to make your income tax calculation easy.

What you can do with this mobile App?

- Calculate Income Tax for FY 2025-26 and previous FY 2024-25

- Enter estimated Investments to check income tax with Old and New Tax Regime

- Save income tax details and track regularly

- Know how much to invest more to save income tax

- More calculators including PPF, SIP returns, Savings account interest and lot more

Use Popular Calculators:

- Income Tax Calculator

- Home Loan EMI Calculator

- SIP Calculator

- PPF Calculator

- HRA Calculator

- Step up SIP Calculator

- Savings Account Interest Calculator

- Lump sum Calculator

- FD Calculator

- RD Calculator

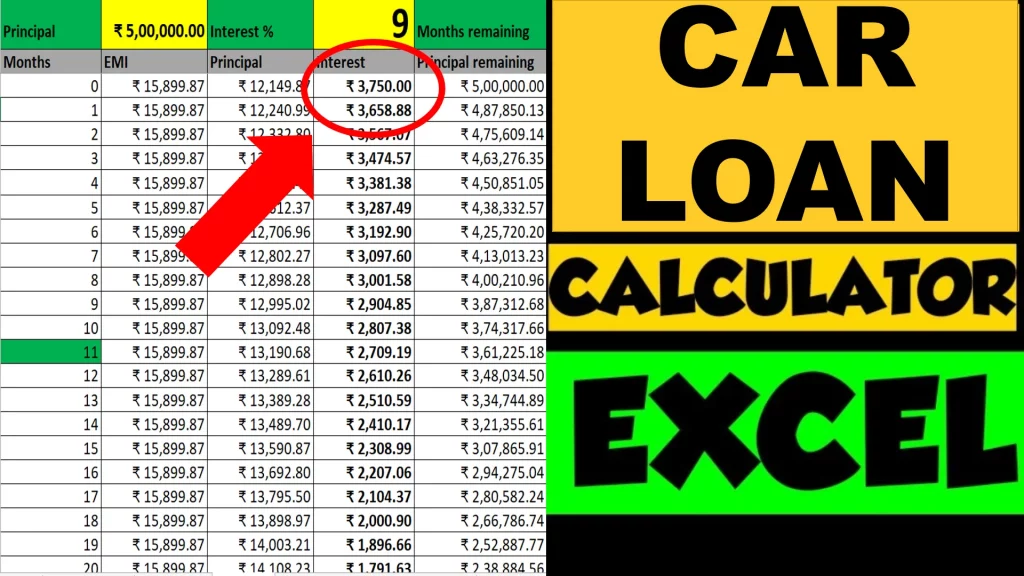

- Car Loan EMI Calculator

- Bike Loan EMI Calculator

- Sukanya Samriddhi Calculator

- Provident Fund Calculator

- Senior Citizen Savings Calculator

- NSC Calculator

- Monthly Income Scheme Calculator

- Mahila Samman Savings Calculator

- Systematic Withdrawal Calculator

- CAGR Calculator

I’d love to hear from you if you have any queries about Personal Finance and Money Management.

JOIN Telegram Group and stay updated with latest Personal Finance News and Topics.

Download our Free Android App – FinCalC to Calculate Income Tax and Interest on various small Saving Schemes in India including PPF, NSC, SIP and lot more.

Follow the Blog and Subscribe to YouTube Channel to stay updated about Personal Finance and Money Management topics.