One of the important questions for traders and investors is, How to Save STCG Tax that they have to pay on STCG (Short Term Capital Gains). You can Save STCG Tax by using Tax Rebate Section 87A which allows Rs. 12,500 with Old Tax Regime in FY 2024-25. This tax rebate can be used to adjust the STCG profits you receive in the financial year. Note that you cannot claim tax rebate 87A with new tax regime against the STCG Profits.

So for example, with old tax regime, if your taxable income is 2.5 lakh, and STCG is Rs. 20,000, based on which STCG tax will be Rs. 4000 (20% STCG tax), then tax with normal rates will be Rs. 0 since normal income is within basic exemption limit, and STCG tax of Rs. 4000 can be adjusted with tax rebate section 87A (max Rs. 12,500), which makes your effective income tax as Rs. 0.

- How to Save STCG Tax Video with Examples

- Understanding Short Term Capital Gains and Applicable Tax Rates

- Using Tax Rebate Section 87A

- Step-by-Step Guide to Saving STCG Tax When Filing ITR-2

- Practical Examples: Illustrating STCG Tax Savings Under the Old Tax Regime

- Why the New Tax Regime May Not Be Ideal for STCG Tax Savings

- Key Considerations for Optimizing Your STCG Tax Strategy

- Frequently Asked Questions (FAQ) on Short Term Capital Gains Tax

- Conclusion

How to Save STCG Tax Video with Examples

Understanding Short Term Capital Gains and Applicable Tax Rates

Short Term Capital Gains arise from the sale of capital assets held for a short period. For equity shares and equity-oriented mutual funds, this period is typically less than 12 months. The tax implications for STCG can vary based on the specific period in which the profit was made:

Key STCG Tax Rates for FY 2024-25:

- 15% Tax Rate: This rate is applicable if your Short Term Capital Gains were booked between April 1, 2024, and July 23, 2024. This period often catches investors who made quick trades early in the financial year.

- 20% Tax Rate: If your STCG profit was realized on or after July 23, 2024, until March 31, 2025, a higher tax rate of 20% applies. This change in rate mid-year highlights the importance of staying updated with tax regulations.

It’s important to note that these STCG tax rates are fixed and apply irrespective of your individual income tax bracket. This means whether you fall into the lowest or highest tax slab, the STCG on equity and equity-oriented mutual funds will be taxed at these specific rates. This fixed rate mechanism is a critical aspect of capital gains taxation that differentiates it from taxation on regular income like salary.

Understanding these rates is the first step towards effective tax planning. By knowing when your gains were booked, you can accurately assess your tax obligation and explore available saving mechanisms.

Using Tax Rebate Section 87A

Tax Rebate Section 87A of the Income Tax Act offers a significant tax rebate that can substantially reduce your overall tax burden, including in some cases, your STCG tax. However, the applicability and extent of this rebate depend on the tax regime you choose (Old vs. New) and your total taxable income.

Section 87A Rebate Under the Old Tax Regime:

Under the Old Tax Regime, Section 87A provides a tax rebate of up to ₹12,500. This rebate is available to individuals whose total taxable income (including STCG) does not exceed ₹5 lakh. If your total tax payable is less than ₹12,500 and your income is within this limit, your entire tax liability could be reduced to zero. This makes the Old Tax Regime a potentially attractive option for those with moderate incomes and some STCG.

Section 87A Rebate Under the New Tax Regime:

The New Tax Regime also offers a tax rebate under Section 87A, but with different limits. Here, the rebate can go up to ₹25,000, applicable if your total taxable income is ₹7 lakh or less. While this higher rebate amount seems appealing, there’s a critical distinction when it comes to STCG. As seen in above video, while filing ITR under the New Tax Regime, this rebate generally cannot be claimed against Short Term Capital Gains. It primarily applies to your normal income, such as salary or business income. This means even if your total income is below ₹7 lakh, any STCG tax will still be payable, as the rebate won’t offset it. This is a crucial point for investors to consider when choosing between the Old and New Tax Regimes.

Comparison Table: Section 87A Rebate

| Feature | Old Tax Regime | New Tax Regime |

| Maximum Rebate Amount | ₹12,500 | ₹25,000 |

| Income Limit for Rebate | Taxable income up to ₹5 lakh | Taxable income up to ₹7 lakh |

| Applicability to STCG Tax | Can be used to offset STCG tax if income within limit | Generally cannot be used to offset STCG tax |

| Primary Application | Normal income + STCG | Normal income only |

This comparison highlights why choosing the right tax regime is important for STCG tax savings. For those with significant STCG, the Old Tax Regime might offer more direct benefits through the Section 87A rebate, provided their overall income remains within the specified threshold of Rs. 5 lakh in a financial year.

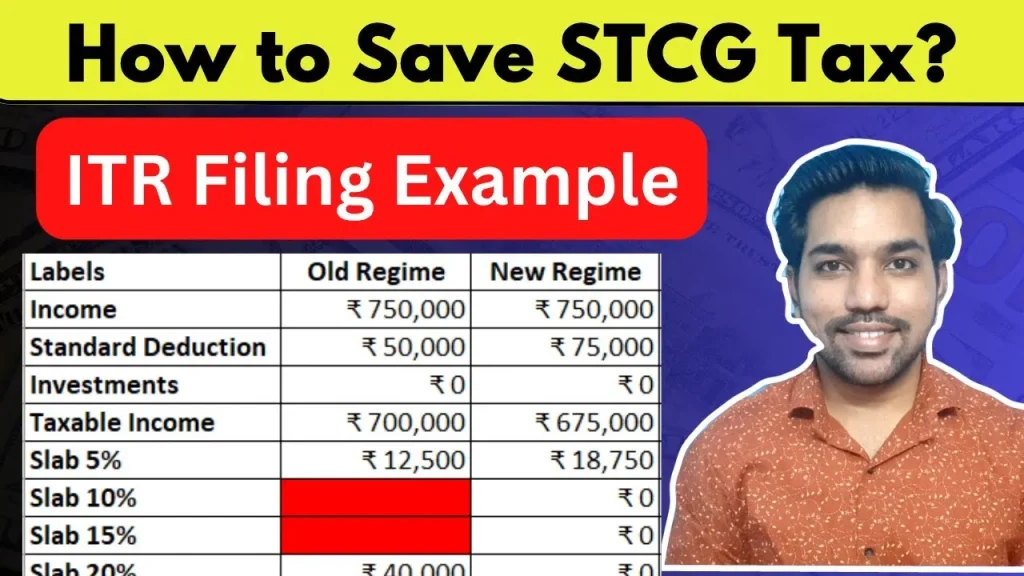

Step-by-Step Guide to Saving STCG Tax When Filing ITR-2

Filing ITR-2 can seem complex, but by following a structured approach, you can ensure all your capital gains are correctly reported and any applicable rebates are claimed. Here’s a detailed walkthrough of the process within the Income Tax Portal, specifically focusing on STCG.

- Login to the Income Tax Portal:

- Begin by logging into your account on the official Income Tax Department e-filing portal.

- Select the appropriate assessment year (AY 2025-26 for FY 2024-25).

- Choose ITR-2 as your Income Tax Return form. ITR-2 is typically used by individuals and HUFs who do not have income from business or profession, but have income from capital gains, multiple house properties, or foreign assets.

- Select Schedules:

- Upon entering the ITR-2 filing interface, you will be prompted to confirm certain details. Ensure you select “Taxable income is more than basic exemption limit” if applicable.

- Select any other relevant deduction schedules, such as those for Chapter VI-A deductions (e.g., Section 80C, 80D), if you are claiming them under the Old Tax Regime.

- General Information:

- For first-time filers for the current financial year, select option “139(1)” (Original Return).

- Crucially, to opt for the Old Tax Regime and potentially benefit from the STCG rebate, ensure you select “Yes” in the General Information section when asked about opting for the old regime. If you choose “No” or don’t make a selection, the system will default to the New Tax Regime.

- Schedule Salary (if applicable):

- If you are a salaried individual, enter your gross salary for the financial year in the “Schedule Salary” section.

- Under the Old Tax Regime, a standard deduction of ₹50,000 will be automatically applied to your salary income, reducing your taxable salary.

- Schedule Capital Gains – Reporting STCG:

- This is the most critical section for STCG. Expand the section for “Short Term Capital Gain”.

- Click “Add Another” to enter details for each STCG transaction.

- Categorize by Transfer Date:

- Before July 23, 2024: Enter details of transactions where the transfer (sale) occurred before this date. These gains will be taxed at 15%.

- On or After July 23, 2024: Enter details for transactions where the transfer occurred on or after this date. These gains will be taxed at 20%.

- Enter Transaction Details:

- Schedule SI (Special Income):

- Your calculated STCG tax will be displayed here. For instance, if you had an STCG of ₹20,000 taxed at 20%, you would see ₹4,000 as the STCG tax here. This schedule consolidates all income taxed at special rates, providing a clear overview.

- Part B – Computation of Total Income:

- Finally, proceed to “Part B – Computation of Total Income.” This section provides a summary of your entire tax computation.

- You will see:

- Tax at Normal Rates: This is the tax calculated on your gross salary (after standard deduction) or other normal income.

- Tax at Special Rates: This will show the tax on your STCG, as calculated in Schedule SI.

- The Total Tax will be the sum of tax at normal rates and tax at special rates.

- Crucially, the tax rebate under Section 87A will be applied here. If your total tax payable (including STCG tax) is within the rebate limit and your income qualifies, the rebate will reduce your final tax liability.

By following above steps, you can ensure accurate reporting of your STCG and effectively claim the Section 87A rebate where applicable, leading to significant tax savings.

Practical Examples: Illustrating STCG Tax Savings Under the Old Tax Regime

To solidify your understanding, let’s look at practical examples demonstrating how the Section 87A rebate impacts STCG tax under the Old Tax Regime. These scenarios highlight the income thresholds and their effect on your final tax payable.

Example 1: Full Tax Rebate (Gross Salary ₹3.5 Lakh, STCG ₹20,000)

- Gross Salary: ₹3,50,000

- Standard Deduction (Old Regime): ₹50,000

- Taxable Salary: ₹3,00,000

- Short Term Capital Gain (STCG): ₹20,000 (taxed at 20%)

- Total Income: ₹3,00,000 (Taxable Salary) + ₹20,000 (STCG) = ₹3,20,000

Tax Calculation:

- Normal Tax (on ₹3,00,000): ₹2,500 (assuming basic exemption limit and slab rates)

- STCG Tax (on ₹20,000 at 20%): ₹4,000

- Total Tax Payable (before rebate): ₹2,500 + ₹4,000 = ₹6,500

Applying Section 87A Rebate:

- Since the total income (₹3,20,000) is less than the ₹5 lakh limit for the Old Tax Regime’s Section 87A rebate, and the total tax payable (₹6,500) is less than the maximum rebate of ₹12,500, the entire tax amount of ₹6,500 will be rebated.

- Final Tax Payable: ₹0

This example clearly shows how individuals with moderate incomes can effectively eliminate their STCG tax liability by utilizing the Section 87A rebate under the Old Tax Regime.

Example 2: No Tax Rebate (Gross Salary ₹5.5 Lakh, STCG ₹20,000)

- Gross Salary: ₹5,50,000

- Standard Deduction (Old Regime): ₹50,000

- Taxable Salary: ₹5,00,000

- Short Term Capital Gain (STCG): ₹20,000 (taxed at 20%)

- Total Income: ₹5,00,000 (Taxable Salary) + ₹20,000 (STCG) = ₹5,20,000

Tax Calculation:

- Normal Tax (on ₹5,00,000): ₹12,500 (assuming slab rates)

- STCG Tax (on ₹20,000 at 20%): ₹4,000

- Total Tax Payable (before rebate): ₹12,500 + ₹4,000 = ₹16,500

Applying Section 87A Rebate:

- In this scenario, the total income (₹5,20,000) exceeds the ₹5 lakh limit for the Section 87A rebate under the Old Tax Regime.

- Therefore, the rebate is not applicable.

- Final Tax Payable: ₹16,500 + 4% Health and Education Cess.

This example underscores the importance of the income threshold for claiming the Section 87A rebate to save STCG Tax. Even a slight exceedance can lead to the loss of the entire rebate benefit.

Example 3: Partial Tax Rebate (Gross Salary ₹5.3 Lakh, STCG ₹20,000)

- Gross Salary: ₹5,30,000

- Standard Deduction (Old Regime): ₹50,000

- Taxable Salary: ₹4,80,000

- Short Term Capital Gain (STCG): ₹20,000 (taxed at 20%)

- Total Income: ₹4,80,000 (Taxable Salary) + ₹20,000 (STCG) = ₹5,00,000

Tax Calculation:

- Normal Tax (on ₹4,80,000): ₹11,500 (assuming slab rates)

- STCG Tax (on ₹20,000 at 20%): ₹4,000

- Total Tax Payable (before rebate): ₹11,500 + ₹4,000 = ₹15,500

Applying Section 87A Rebate:

- Here, the total income (₹5,00,000) is exactly at the limit for the Section 87A rebate.

- The maximum rebate available is ₹12,500.

- Rebate Received: ₹12,500

- Remaining Tax Payable: ₹15,500 – ₹12,500 = ₹3,000 + 4% Health and Education Cess.

This example illustrates a scenario where a partial rebate is received to Save STCG Tax, reducing the tax burden but not eliminating it entirely. It highlights the precise application of the rebate up to its maximum limit.

Why the New Tax Regime May Not Be Ideal for STCG Tax Savings

While the New Tax Regime offers a higher basic exemption limit and a larger Section 87A rebate (up to ₹25,000 for income up to ₹7 lakh), it comes with a significant caveat for investors dealing with STCG. As highlighted earlier, the Section 87A rebate under the New Tax Regime cannot be used to adjust or offset Short Term Capital Gains tax.

This means that even if your total income is below ₹7 lakh and you qualify for the ₹25,000 rebate, this rebate will only apply to your normal income (like salary or business income). Any STCG tax calculated at 15% or 20% will still be payable in full, regardless of the rebate you receive on your other income.

For instance, if you have a salary of ₹6.5 lakh and an STCG of ₹50,000, under the New Tax Regime, your salary income might be fully rebated, but you would still have to pay the tax on the ₹50,000 STCG. This makes the New Tax Regime less attractive for individuals whose primary goal is to minimize STCG tax specifically through the Section 87A rebate. Investors should carefully evaluate their income sources and the potential impact of each regime before making a choice.

Watch below video on New Tax Regime tax saving options

New Tax Regime Tax Saving Options Video

Key Considerations for Optimizing Your STCG Tax Strategy

Beyond understanding the tax rates and rebates, several other factors can influence your STCG tax strategy.

- Timing of Sales: As demonstrated, the date of booking your STCG profit (before or after July 23, 2024, for FY 2024-25) directly impacts the tax rate. Strategic timing of your sales, where feasible, can help you manage your tax liability.

- Choosing the Right ITR Form: Ensure you select the correct ITR form. ITR-2 is appropriate for individuals with capital gains. Using the wrong form can lead to complications and delays in processing your return.

- Accurate Data Entry: Double-check all figures entered, including sale value, cost of acquisition, and dates. Errors can lead to incorrect tax calculations and potential notices from the tax department.

- Utilizing Online Calculators: Many online income tax calculators and mobile applications (such as fincalc mobile app) can help you estimate your tax liability under both the Old and New Tax Regimes. These tools can be invaluable for comparing scenarios and making an informed decision about which regime to choose.

By considering these points, you can develop a robust STCG tax strategy that aligns with your financial goals and minimizes your tax outflow.

Frequently Asked Questions (FAQ) on Short Term Capital Gains Tax

Here are some frequently asked questions about Short Term Capital Gains tax and its implications, based on common user queries and the content discussed:

What is Short Term Capital Gain (STCG)?

Short Term Capital Gain is the profit earned from selling a capital asset (like shares, mutual funds, or property) within a short period after its purchase. For listed equity shares and equity-oriented mutual funds, this period is typically less than 12 months.

What are the STCG tax rates for equity shares in FY 2024-25?

For FY 2024-25, STCG on equity shares and equity-oriented mutual funds is taxed at 15% if booked between April 1, 2024, and July 23, 2024. If booked on or after July 23, 2024, until March 31, 2025, the rate is 20%. These rates apply regardless of your income slab.

Can Section 87A rebate be claimed against STCG tax?

Yes, under the Old Tax Regime, Section 87A rebate (up to ₹12,500) can be claimed against STCG tax, provided your total taxable income does not exceed ₹5 lakh. However, under the New Tax Regime, the Section 87A rebate (up to ₹25,000 for income up to ₹7 lakh) generally cannot be used to offset STCG tax; it applies primarily to normal income.

Which ITR form should I use if I have STCG?

If you are an individual and have income from capital gains (including STCG) but do not have income from business or profession, you should typically use ITR-2.

What is the significance of July 23, 2024, for STCG taxation?

July 23, 2024, marks a change in the STCG tax rate for equity and equity-oriented mutual funds. Gains booked before this date are taxed at 15%, while those booked on or after this date are taxed at 20%.

What if my total income exceeds the limit for Section 87A rebate in the Old Tax Regime?

If your total taxable income exceeds ₹5 lakh in the Old Tax Regime, you will not be eligible for the Section 87A rebate, and your STCG tax will be payable in full along with your other tax liabilities.

Is Securities Transaction Tax (STT) relevant for STCG?

Yes, STCG on equity shares and equity-oriented mutual funds is typically covered under Section 111A, which applies when STT has been paid on the transaction. This is why the specific rates of 15% or 20% apply.

Conclusion

Understanding and effectively managing your Short Term Capital Gains tax is an important step of sound financial planning and knowing How to Save STCG Tax. By grasping the nuances of STCG tax rates and strategically utilizing the Section 87A rebate, particularly under the Old Tax Regime, you can significantly reduce your tax outflow for the financial year 2024-25. The detailed steps for filing ITR-2, combined with practical examples, provide a clear roadmap for reporting your capital gains accurately and claiming all eligible benefits.

While the New Tax Regime offers its own set of advantages, its limitations regarding STCG tax adjustment through Section 87A make the Old Tax Regime a potentially more favorable choice for investors focused on minimizing capital gains tax. Always remember to maintain thorough records, consider the timing of your investments and sales, and seek professional guidance when in doubt. By taking these proactive steps, you can navigate the tax landscape with confidence, ensuring compliance while optimizing your financial returns.

Save Home Loan Interest Amount!

Use Home Loan Excel Calculator that will help you to Save Interest Amount on Home Loan EMI.

Click below button to download Home Loan EMI and Prepayment Calculator in Excel:

Watch how Home Loan Calculator in Excel Works

Income Tax Calculator App – FinCalC

For Income Tax Calculation on your mobile device, you can Download my Android App “FinCalC” which I have developed for you to make your income tax calculation easy.

What you can do with this mobile App?

- Calculate Income Tax for FY 2025-26 and previous FY 2024-25

- Enter estimated Investments to check income tax with Old and New Tax Regime

- Save income tax details and track regularly

- Know how much to invest more to save income tax

- More calculators including PPF, SIP returns, Savings account interest and lot more

Use Popular Calculators:

- Income Tax Calculator

- Home Loan EMI Calculator

- SIP Calculator

- PPF Calculator

- HRA Calculator

- Step up SIP Calculator

- Savings Account Interest Calculator

- Lump sum Calculator

- FD Calculator

- RD Calculator

- Car Loan EMI Calculator

- Bike Loan EMI Calculator

- Sukanya Samriddhi Calculator

- Provident Fund Calculator

- Senior Citizen Savings Calculator

- NSC Calculator

- Monthly Income Scheme Calculator

- Mahila Samman Savings Calculator

- Systematic Withdrawal Calculator

- CAGR Calculator

I’d love to hear from you if you have any queries about Personal Finance and Money Management.

JOIN Telegram Group and stay updated with latest Personal Finance News and Topics.

Download our Free Android App – FinCalC to Calculate Income Tax and Interest on various small Saving Schemes in India including PPF, NSC, SIP and lot more.

Follow the Blog and Subscribe to YouTube Channel to stay updated about Personal Finance and Money Management topics.