Did you know that a mere 0.5% hike in Home Loan interest rates on a ₹40 lakh home loan can increase your total repayment by over ₹3 lakh? On the flip side, a similar cut could save you the same amount. Understanding why and how these rate changes happen can help you stay ahead and make smarter financial moves. Home Loan Interest Rate Change Calculator can help you plan your finances and budget accordingly to handle interest rate changes.

You can download Home Loan Interest Rate Change Calculator using below button:

Home Loan Interest Rate Change Calculator [Video]

Watch more Videos on YouTube Channel

What happens when Home Loan Interest Rate Changes?

When home loan interest rates changes, your EMI or loan tenure adjusts automatically based on updated interest rate, which directly impacts your monthly budget and total interest outgo in home loan. Even a small 0.5% shift can add or save lakhs over the loan’s lifetime.

Below are some points you should know when Home Loan Interest Rate Changes:

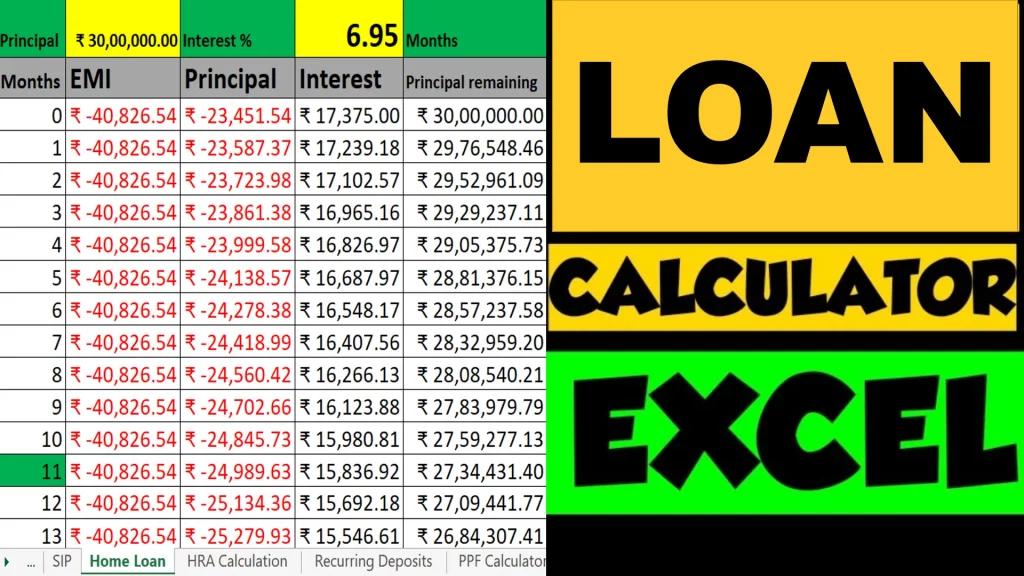

- EMI Increase with Rate Hike: If interest rates rise, your monthly EMI goes up unless you opt to extend the loan tenure. For example, a ₹40 lakh loan at 8.5% for 20 years has an EMI of approximately ₹34,700; if the rate rises to 9%, EMI jumps to ~₹36,000, adding ~₹3.1 lakh over the tenure. Most banks try to keep the EMI same and increase the tenure by default – in any case, your interest outgo will increase with interest rate increase

- EMI Reduction with Rate Cut: A decrease in interest rates lowers EMIs or shortens tenure, saving you money. Even a 0.5% cut can reduce total interest significantly

- Tenure Adjustment: Lenders often adjust tenure instead of EMI when rates change. This means your monthly payment stays the same, but the loan duration extends or shortens depending on the rate movement

- Repo Rate Linkage: Most floating-rate home loans are linked to the RBI’s repo rate. When RBI hikes repo rates, borrowing costs rise, when it cuts rates, EMIs reduce. Repo rate is the interest rate at which RBI lends money to banks – so if bank’s interest rate increases, bank also increase their loan interest rates as well

- Impact on Total Interest Paid: Rate hikes increase the total interest outgo over the loan tenure, while rate cuts reduce it. This directly affects long-term affordability

- Budgeting Challenges: For middle-income borrowers, even small hikes can strain monthly budgets, especially for loans in the ₹10–25 lakh range

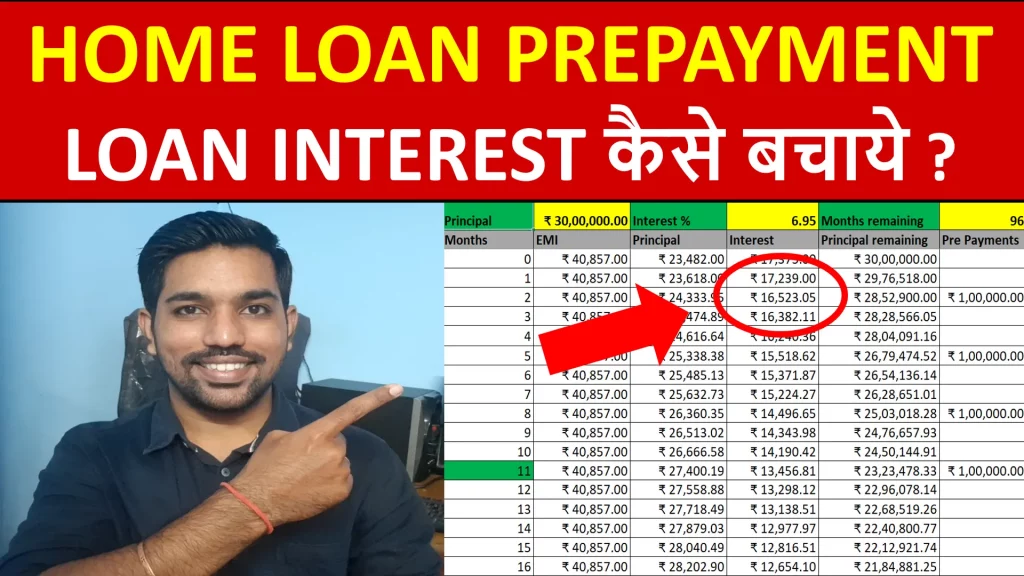

- Borrower Options: You can choose to prepay part of the loan, refinance to a lower rate, or request tenure adjustments to manage the impact of rate changes

- Property Market Influence: Rising interest rates can reduce home loan demand and slow property purchases, while falling rates often boost demand

- Fixed vs. Floating Loans: Fixed-rate loans remain unaffected by rate changes, while floating-rate loans fluctuate with market conditions

- Long-Term Planning: Understanding how rate changes affect EMIs help borrowers plan better, avoid financial stress, and make informed prepayment or refinancing decisions. So you should know these points when your home loan interest rate changes.

Use Home Loan EMI Calculator:

Why Home Loan Interest Rate Changes?

Below are few reasons to understand why home loan interest rate changes:

- Repo Rate Movements (RBI Policy): In India, most floating-rate home loans are benchmarked to the RBI’s repo rate. When the RBI increases repo rates to control inflation, borrowing costs rise, leading to higher home loan interest rates. Conversely, when repo rate is cut – it makes loan cheaper interms of interest rates

- Inflation and Economic Conditions: High inflation often prompts the RBI to raise rates, making loans costlier. During low inflation or economic slowdown, rates are reduced to encourage borrowing and spending by the people of India. So RBI tries to keep the balance in order to make money flow in the market

- Bank Funding Costs: Lenders adjust home loan rates based on their own cost of funds. If deposit rates or borrowing costs rise, banks pass this on to borrowers through higher loan rates

- Global Market Trends: International interest rate changes, currency fluctuations, and global liquidity can indirectly influence Indian lending rates, especially for long-term loans

- Loan Type (Fixed vs. Floating): Fixed-rate loans remain constant throughout the tenure, while floating-rate loans change whenever the benchmark rate is revised. This is why borrowers with floating loans see frequent EMI or tenure adjustments. But fixed rate loans have slightly higher interest rate compared to floating rate home loans

You can download the Home Loan Excel Calculator from the top of this article to know the calculations when your loan interest rate changes.

Interest Rate Change Effective Date

The interest rate change effective date is the day from which your revised home loan interest rate is applied by the lender. From this date onward, your EMI or loan tenure is recalculated based on the new rate.

Most of the banks follow the first day of the new quarter as the interest rate change effective date, so it depends on the lender. For example, if repo rate increases in the month of November or December, you’ll likely see the increase in your existing home loan from next quarter – which is from 1st January. So new rates would be likely applicable from either of – 1st January, 1st April, 1st July or 1st October.

ALSO READ: Home Loan for Beginners

Can Bank Change the Home Loan Interest Rate on Existing Loan?

Yes, banks can change the interest rate on an existing home loan, but it depends on the type of loan you have.

For floating-rate loans, the interest rate is linked to benchmarks like the RBI’s repo rate, so it fluctuates whenever the benchmark changes. This means your EMI or loan tenure will be recalculated based on the new rate, and usually the effective date for the new interest rate is from next quarter.

For fixed-rate loans, the interest rate remains constant throughout the tenure, so banks cannot alter it. In practice, most borrowers opt for floating-rate loans, which makes them directly affected by market and policy-driven rate changes.

Also, floating rate home loans are cheaper compared to fixed rate home loans.

Conclusion

Home loan interest rate changes are driven by factors like RBI policy decisions, inflation, and banks’ funding costs, and they directly affect your EMI, loan tenure, and total interest burden. Borrowers with floating-rate loans must stay alert, as even a small 0.25% shift can add or save lakhs over the loan’s lifetime.

Understanding these changes help you to plan better, manage cash flow, and make timely decisions such as prepayment or refinancing. In essence, monitoring rate movements is key to protecting your financial stability and maximizing savings.

Some more Reading:

Save Home Loan Interest Amount!

Use Home Loan Excel Calculator that will help you to Save Interest Amount on Home Loan EMI.

Click below button to download Home Loan EMI and Prepayment Calculator in Excel:

Watch how Home Loan Calculator in Excel Works

Income Tax Calculator App – FinCalC

For Income Tax Calculation on your mobile device, you can Download my Android App “FinCalC” which I have developed for you to make your income tax calculation easy.

What you can do with this mobile App?

- Calculate Income Tax for FY 2025-26 and previous FY 2024-25

- Enter estimated Investments to check income tax with Old and New Tax Regime

- Save income tax details and track regularly

- Know how much to invest more to save income tax

- More calculators including PPF, SIP returns, Savings account interest and lot more

Use Popular Calculators:

- Income Tax Calculator

- Home Loan EMI Calculator

- SIP Calculator

- PPF Calculator

- HRA Calculator

- Step up SIP Calculator

- Savings Account Interest Calculator

- Lump sum Calculator

- FD Calculator

- RD Calculator

- Car Loan EMI Calculator

- Bike Loan EMI Calculator

- Sukanya Samriddhi Calculator

- Provident Fund Calculator

- Senior Citizen Savings Calculator

- NSC Calculator

- Monthly Income Scheme Calculator

- Mahila Samman Savings Calculator

- Systematic Withdrawal Calculator

- CAGR Calculator

I’d love to hear from you if you have any queries about Personal Finance and Money Management.

JOIN Telegram Group and stay updated with latest Personal Finance News and Topics.

Download our Free Android App – FinCalC to Calculate Income Tax and Interest on various small Saving Schemes in India including PPF, NSC, SIP and lot more.

Follow the Blog and Subscribe to YouTube Channel to stay updated about Personal Finance and Money Management topics.