If you are struggling financially, there are few Bad Money Habits that you must avoid. This is required for you financial stability and reducing your stress. Some of the bad habits include bad debt, not managing your money, not making any investments to grow your money, not understanding your income tax calculation, etc.

- 1. Paying Yourself Last: The Rich vs. Poor Habit

- 2. The Danger of Bad Debt: Understanding Responsible Borrowing

- 3. The Importance of a Financial Buffer: Emergency Fund Essentials

- 4. Mastering Income and Expenses Tracking: Understanding Your Financial Landscape

- 5. Conscious Spending: Differentiating Needs from Wants

- 6. The Power of Saving: Building Your Financial Foundation

- 7. Understanding Taxes: Minimizing Your Tax Liability

- 8. Time in the Market: The Importance of Early Investing

- 9. Engaging With Your Finances: Proactive Management

- Conclusion

1. Paying Yourself Last: The Rich vs. Poor Habit

This concept, popularized by Robert Kiyosaki’s “Rich Dad Poor Dad,” is a fundamental shift in mindset. The “poor people’s habit” is to pay all your bills and expenses first, leaving whatever’s leftover for savings. This often results in nothing being left to save! The “rich people’s habit,” on the other hand, prioritizes savings. The moment your paycheck hits your account, a portion is automatically transferred to your savings account. This is crucial! Treat saving as a non-negotiable expense, like rent or utilities.

You can simply start an SIP at the start of the month, before the remaining funds goes to your unnecessary expenses.

How to break the habit:

- Automate your savings: Set up automatic transfers to your savings account immediately after receiving your paycheck. Even a small percentage saved consistently adds up over time

- Budget effectively: Create a realistic budget that allocates funds for savings before other expenses. Tools like spreadsheets or budgeting apps can assist

- Prioritize saving: Consider saving as an investment in your future self, securing financial stability and opportunities.

2. The Danger of Bad Debt: Understanding Responsible Borrowing

Debt is a significant obstacle to financial freedom. While some debt (like a mortgage for a appreciating asset) can be manageable, excessive or high-interest debt can make you struggle to manage your finances. Avoid using debt for non-essential purchases, if you can’t afford something outright, you shouldn’t be buying it on credit. The high interest rates on credit cards quickly erase any perceived benefits or rewards.

How to break the habit:

- Prioritize high-interest debt: Focus on paying off high-interest debt (like credit cards) first to minimize interest charges.

- Create a debt repayment plan: Develop a strategic plan to tackle your debts, considering methods like the debt snowball or debt avalanche.

- Avoid unnecessary debt: Resist impulsive purchases and carefully consider the long-term implications of taking on debt.

- Seek professional help: If you’re struggling with debt, consider seeking advice from a financial advisor or credit counselor.

3. The Importance of a Financial Buffer: Emergency Fund Essentials

Unexpected expenses happen. A financial buffer, or emergency fund, provides a safety net to cover unforeseen costs, such as medical bills, car repairs, or job loss, without taking a loan. Aim for 3-6 months’ worth of living expenses in your emergency fund.

How to build a buffer:

- Start small: Begin by saving even a small amount each month, gradually increasing contributions as your financial situation improves.

- Automate transfers: Set up automatic transfers to a dedicated emergency fund account.

- Consider high-yield savings accounts: Explore high-yield savings accounts or money market accounts to earn interest on your emergency fund.

4. Mastering Income and Expenses Tracking: Understanding Your Financial Landscape

Understanding your income and expenses is critical for effective financial management. Track your income and spending diligently to identify areas where you can cut back and save more.

Effective tracking:

- Use budgeting apps: Many free and paid apps help track income and expenses automatically.

- Maintain a spreadsheet: Create a simple spreadsheet to manually record your income and expenses.

- Categorize expenses: This helps identify spending patterns and prioritize needs versus wants.

5. Conscious Spending: Differentiating Needs from Wants

Mindful spending is the key to financial success. Differentiate between needs (essential expenses) and wants (non-essential expenses). Before making any purchase, ask yourself if it’s truly necessary or if it’s an impulse buy. impulse buying is something that you buy based on the presentation of the products rather than the your needs.

Strategies for conscious spending:

- The 24-hour rule: Wait 24 hours before making any significant purchase to avoid impulsive spending.

- Track discretionary spending: Monitor your spending on non-essential items to identify areas for reduction.

- Prioritize needs: Focus on fulfilling your essential needs before indulging in wants.

6. The Power of Saving: Building Your Financial Foundation

Saving consistently, even small amounts, builds wealth over time. Explore different savings vehicles such as high-yield savings accounts, money market accounts, or investment accounts, depending on your financial goals and risk tolerance.

Boost your savings:

- Increase savings rate gradually: Gradually increase your savings rate over time as your income increases

- Set savings goals: Define specific savings goals (e.g., emergency fund, down payment, retirement) to stay motivated

- Explore high-yield options: Research high-yield savings accounts or investment options to maximize returns

7. Understanding Taxes: Minimizing Your Tax Liability

Understanding tax laws is crucial for maximizing your after-tax income. Take advantage of tax deductions and credits to minimize your tax liability. If unsure, consult a tax professional.

You can make use of tax deductions in old tax regime. But old regime slab rates are higher compared to new tax regime, so you can select tax regime based on your income and investments level.

ALSO READ: How to Calculate Income Tax with Examples

8. Time in the Market: The Importance of Early Investing

The earlier you start investing, the more time your money has to grow through compounding. Even small, consistent investments made early can yield substantial returns over the long term.

Giving time to the Market is more important than timing the marketALSO READ: SIP returns in Sensex for last 25 Years

9. Engaging With Your Finances: Proactive Management

Ignoring your finances won’t magically solve financial problems. Engage with your finances proactively, creating budgets, tracking your progress, and making adjustments as needed. Seek advice if you’re struggling.

Learning is a lifetime process, so based on these above mentioned points you can start working on your actions and automating your savings and investments. Apart from this, you can watch my YouTube videos to learn more about handling your personal finances.

Conclusion

Breaking free from bad money habits requires commitment and consistent effort. By implementing the strategies outlined in this guide, you can take control of your finances, build wealth, and achieve your financial goals. Remember, financial success isn’t about quick fixes, it’s about cultivating healthy financial habits that support long-term growth and security. Don’t hesitate to seek professional advice if needed, and remember that progress, not perfection, is the key to financial freedom.

Some more Reading

- 5 Home Loan Repayment Tips

- How to Diversify your Portfolio

- Why Taking high interest loans can be a problem

Save Home Loan Interest Amount!

Use Home Loan Excel Calculator that will help you to Save Interest Amount on Home Loan EMI.

Click below button to download Home Loan EMI and Prepayment Calculator in Excel:

Watch how Home Loan Calculator in Excel Works

Income Tax Calculator App – FinCalC

For Income Tax Calculation on your mobile device, you can Download my Android App “FinCalC” which I have developed for you to make your income tax calculation easy.

What you can do with this mobile App?

- Calculate Income Tax for FY 2025-26 and previous FY 2024-25

- Enter estimated Investments to check income tax with Old and New Tax Regime

- Save income tax details and track regularly

- Know how much to invest more to save income tax

- More calculators including PPF, SIP returns, Savings account interest and lot more

Use Popular Calculators:

- Income Tax Calculator

- Home Loan EMI Calculator

- SIP Calculator

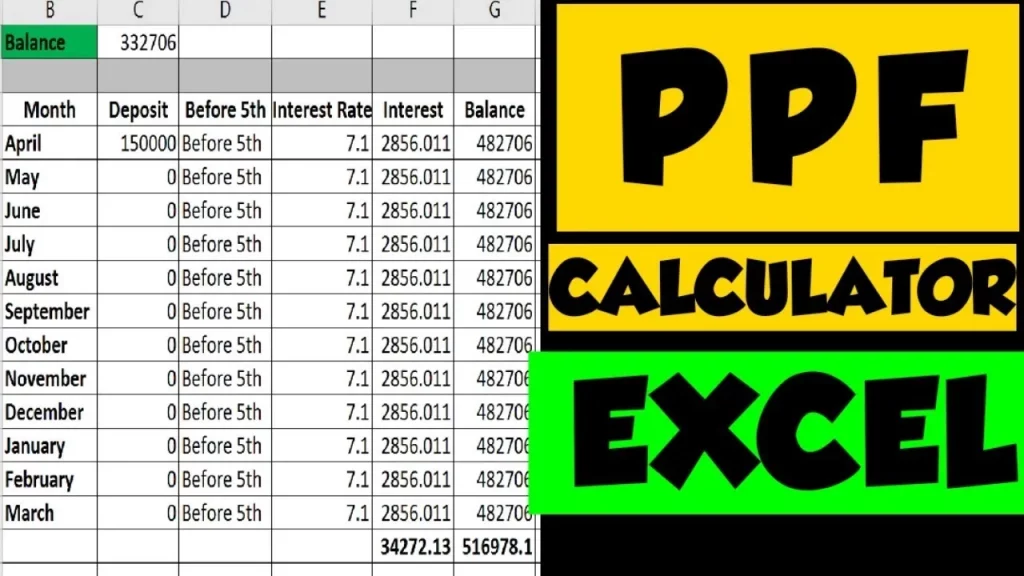

- PPF Calculator

- HRA Calculator

- Step up SIP Calculator

- Savings Account Interest Calculator

- Lump sum Calculator

- FD Calculator

- RD Calculator

- Car Loan EMI Calculator

- Bike Loan EMI Calculator

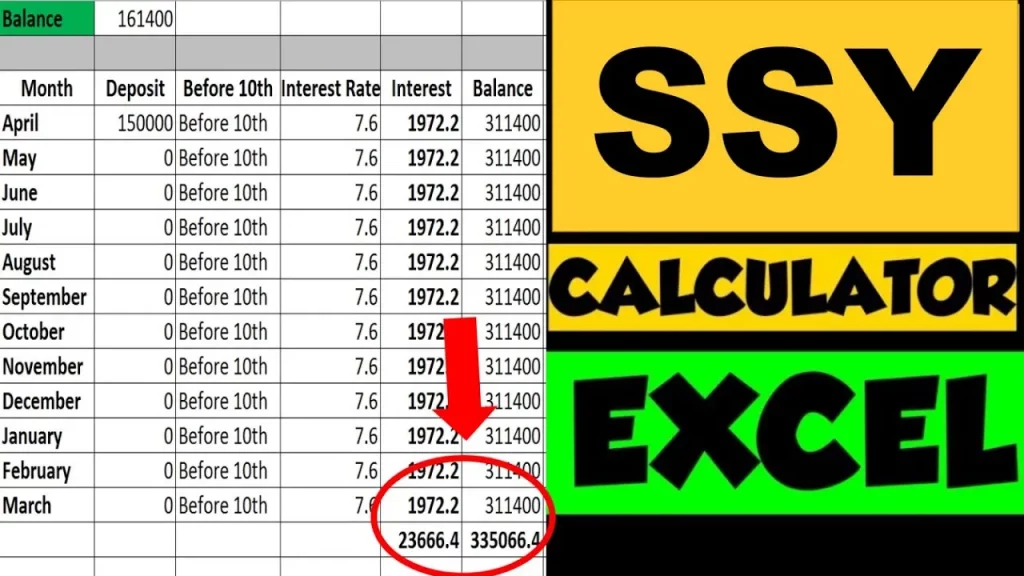

- Sukanya Samriddhi Calculator

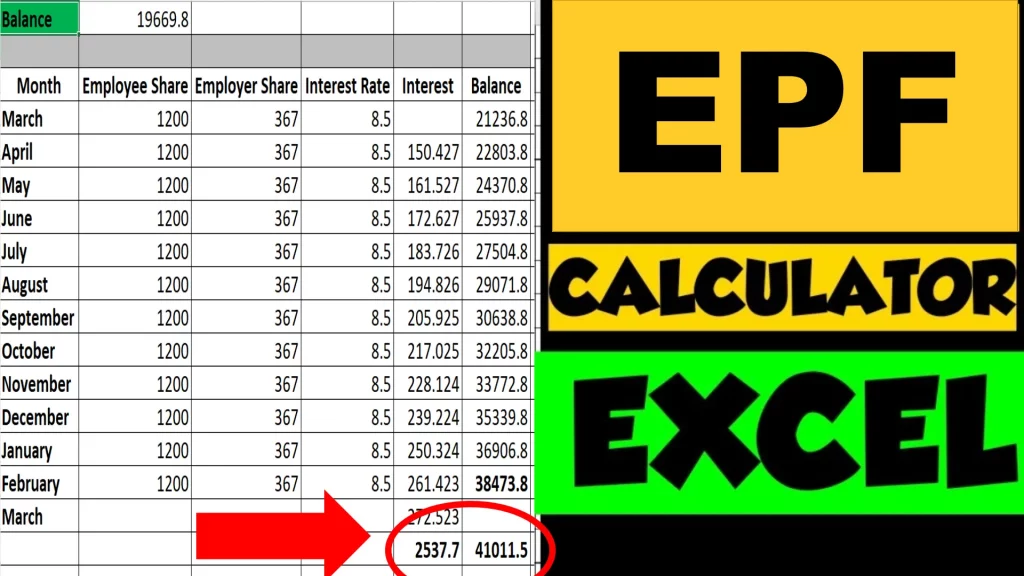

- Provident Fund Calculator

- Senior Citizen Savings Calculator

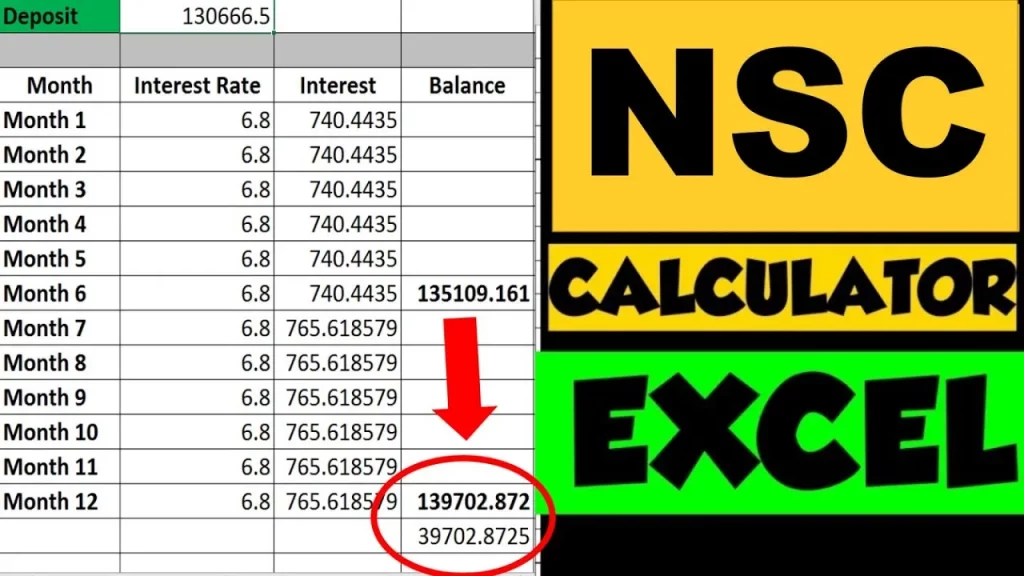

- NSC Calculator

- Monthly Income Scheme Calculator

- Mahila Samman Savings Calculator

- Systematic Withdrawal Calculator

- CAGR Calculator

I’d love to hear from you if you have any queries about Personal Finance and Money Management.

JOIN Telegram Group and stay updated with latest Personal Finance News and Topics.

Download our Free Android App – FinCalC to Calculate Income Tax and Interest on various small Saving Schemes in India including PPF, NSC, SIP and lot more.

Follow the Blog and Subscribe to YouTube Channel to stay updated about Personal Finance and Money Management topics.