Taking out a long-term loan, such as a 25-year home loan, is a significant financial commitment. While these loans make large purchases affordable, the long tenure and accumulated interest can feel like a heavy burden. Many people are unaware that a few simple, disciplined strategies can drastically shorten their loan tenure and save them a substantial amount of money. For example, we can Pay Off a 25-Year Loan in 10 Years and save the loan interest amount by following few strategies – paying extra EMI amounts and regularly making loan prepayments.

Let us discuss these strategies in detail, but first, let’s understand the Loan EMI structure.

The Hidden Costs of Loan Repayment: Understanding the EMI Structure

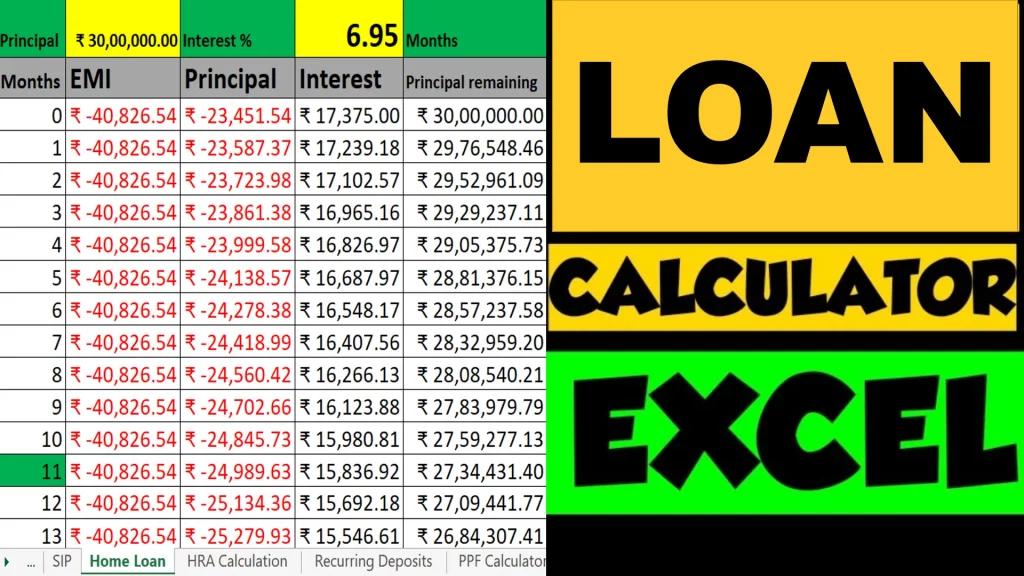

When you take out a loan, you agree to pay an Equated Monthly Installment (EMI). It’s a common misconception that each EMI payment is split evenly between the principal amount (the original loan amount) and the interest charged. In reality, the allocation is heavily skewed towards interest in the initial years of the loan. This means that a large portion of your early EMI payments goes towards paying off the interest amount, with only a small fraction reducing the principal.

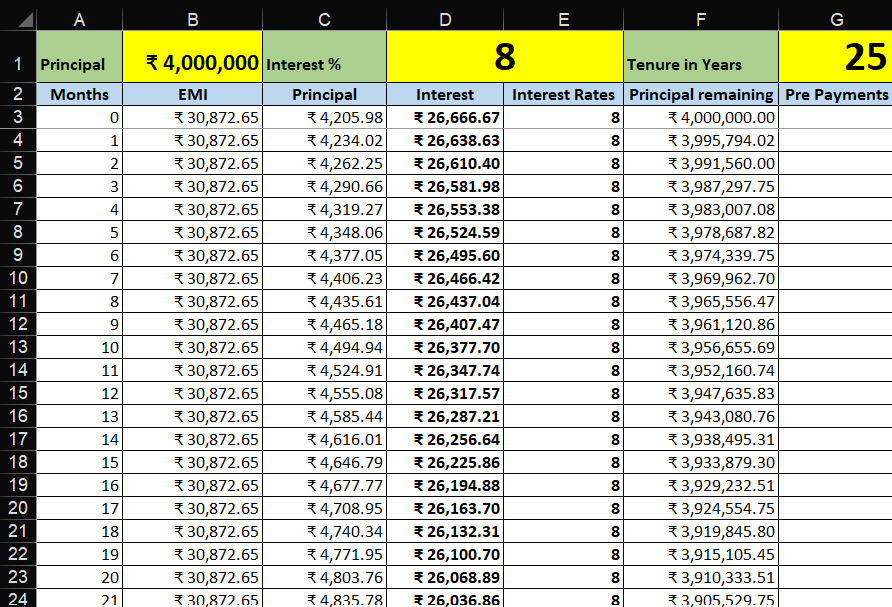

For instance, on a home loan of 40 lakh rupees at an 8% interest rate for 25 years, your monthly EMI would be approximately 30,873 rupees. Over the life of the loan, you would end up paying a staggering 52 lakh rupees in interest—more than the original loan amount. In the very first month, nearly 27,000 rupees of your EMI would be interest, while only around 4,000 rupees would go to the principal. This dynamic slowly shifts over time, but it can take more than 15 years for the principal portion of your EMI to finally become larger than the interest portion. This front-loading of interest is why long-term loans feel so slow to pay down and is the key to why accelerating your payments is so powerful.

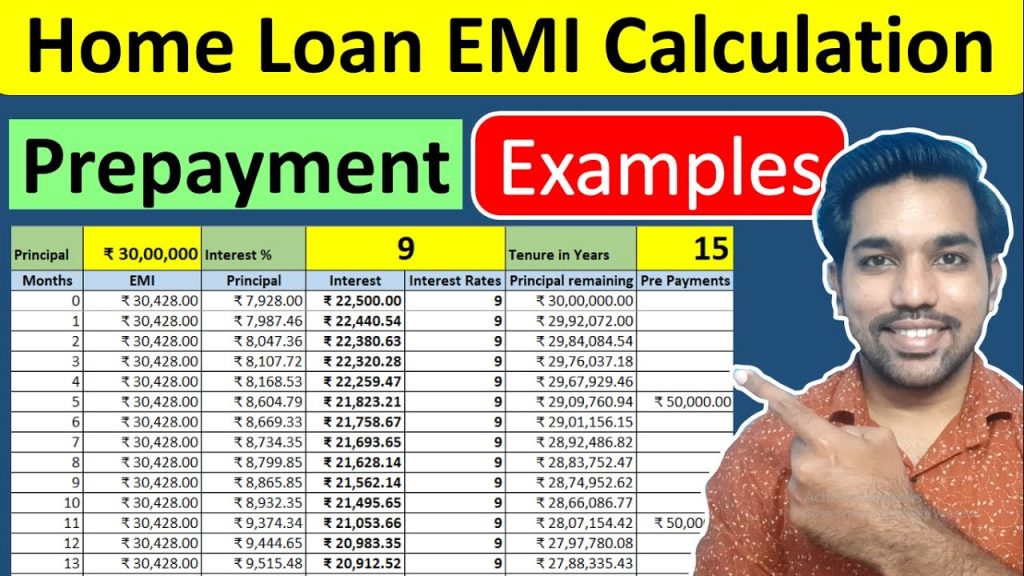

Below is the excel calculator screenshot of above calculations:

You can download the Home Loan Excel Claculator using below button:

Home Loan EMI Calculation Method Video

Watch more Videos on YouTube Channel

Let us now see the strategies to close your loan before time.

Strategy 1: The Power of an Extra EMI

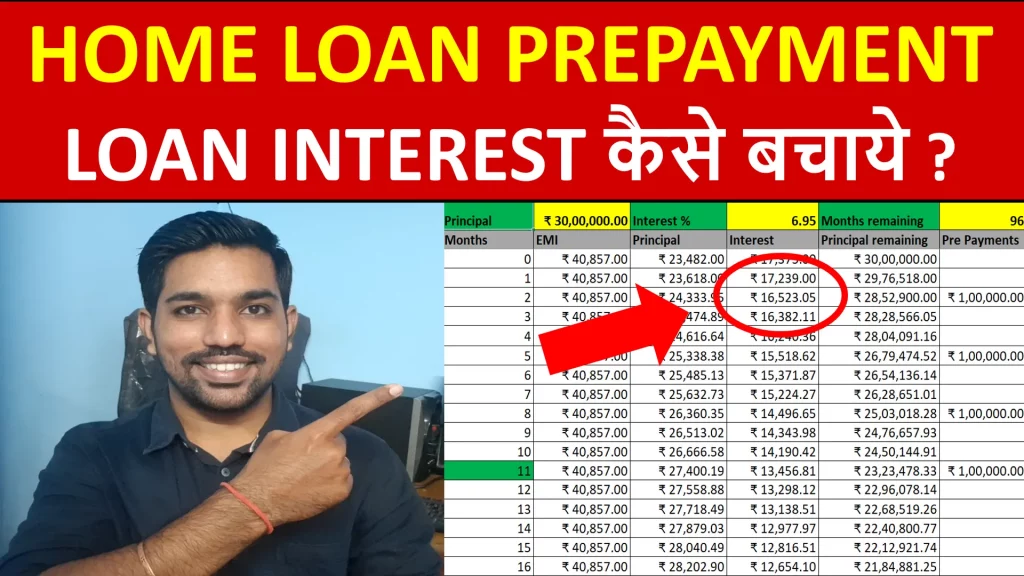

The simplest and most effective way to combat the front-loaded interest is to make additional payments directly to your loan’s principal. A highly effective method is to pay just one extra EMI per year. This small, seemingly insignificant action can have a monumental impact on your loan tenure and total interest paid.

By making one extra EMI payment annually, the entire amount goes directly towards reducing your principal. This directly counteracts the initial slow principal reduction, allowing your loan balance to drop much faster. For the 40 lakh rupee loan example, making just one extra EMI each year can reduce your loan term from 25 years to just 20 years, saving you a remarkable 12 lakh rupees in interest. If you can manage to pay two extra EMIs a year, you could potentially shorten the loan tenure to just 16 years, saving you over 20 lakh rupees.

This strategy works because it leverages the power of compound interest in reverse. Instead of working against you, it starts to work for you by reducing the principal amount on which interest is calculated, accelerating your path to becoming debt-free.

ALSO READ: 7 Home Loan Mistakes you Should Avoid

Strategy 2: The Compound Effect of Increasing Your EMI

As your career progresses, your income is likely to increase through promotions, bonuses, or annual raises. A second powerful strategy is to commit to increasing your EMI by a small percentage, such as 5%, every single year. This is a proactive approach that turns your rising income into a powerful tool for debt repayment.

This strategy is highly effective because a small, consistent increase in your payment amount has a compounding effect on your loan’s principal reduction. It’s an easy adjustment that many people can make without significantly impacting their lifestyle. Using the same 40 lakh rupee loan example, increasing your EMI by just 5% annually can reduce your loan tenure to 13-14 years, resulting in a massive interest saving of 22 lakh rupees.

This approach ensures that as your financial capacity grows, so does your ability to tackle debt. It’s a disciplined and forward-thinking habit that ensures your increasing income translates directly into accelerated financial freedom.

ALSO READ: Home Loan Prepayment Calculation with Examples

Combining Both Strategies: The Ultimate Acceleration Plan

The true magic happens when you combine both strategies. By making one extra EMI payment per year and simultaneously increasing your EMI by 5% annually, you create a supercharged repayment plan. This powerful combination can help you pay off a 25-year loan in as little as 10 years, saving you a substantial amount in interest.

This disciplined, dual-pronged approach is the secret to getting out of debt faster and building significant wealth. It’s about leveraging both lump-sum payments and consistent, small increases to attack the loan principal from all sides. By freeing yourself from the burden of long-term debt, you can reallocate those funds towards building an investment portfolio, securing your family’s future, or pursuing other financial goals.

The following comparison table illustrates the dramatic difference these strategies make:

| Repayment Plan | Loan Tenure (Years) | Total Interest Paid (₹ Lakhs) | Interest Saved (₹ Lakhs) |

| Standard 25-Year Loan | 25 | ~52 | 0 |

| 1 Extra EMI per Year | 20 | ~40 | ~12 |

| Increase EMI by 5% Annually | 13-14 | ~30 | ~22 |

| 1 Extra EMI + 5% Annual Increase | ~12.5 | ~25 | ~27 |

This table clearly demonstrates how a proactive and disciplined approach can turn a decades-long commitment into a manageable, short-term goal.

Frequently Asked Questions

Is it really possible to pay off a 25-year loan in 10 years?

Yes, absolutely. While the provided strategies can get you close, paying off a 25-year loan in 10 years is very aggressive and requires a combination of both strategies as well as making additional lump-sum payments whenever possible (e.g., from bonuses, tax refunds, etc.). The key is to be consistent with your efforts.

What if my bank doesn’t allow prepayment?

Most modern loan agreements, especially for home loans, allow for prepayment without penalty. However, it’s crucial to check your specific loan agreement. If there are prepayment penalties, calculate if the interest savings outweigh the penalty. In many cases, it still makes financial sense to prepay.

Should I pay off my loan or invest my extra money?

This is a classic financial dilemma. The decision depends on your loan’s interest rate. If your loan has a high-interest rate (e.g., above 8-9%), paying it off is often a better “guaranteed return” than investing, which comes with risk. If your loan has a very low-interest rate, investing in instruments that offer a higher potential return might be more beneficial. The strategies outlined here are generally for loans where the interest rate is a significant financial burden.

Will a small EMI increase make a big difference?

Yes, a small increase makes a huge difference due to the compounding effect. The earlier you increase your EMI, the more interest you save because you are reducing the principal on which the interest is calculated for the longest period. Even a 2% or 3% annual increase can significantly shorten your loan tenure.

Some more Reading:

- Home Loan Calculations with Variable Interest Rates

- 5 Repayment Tips for Home Loans

- 5 Habits of Rich People that will Change your Life

Conclusion: Take Control of Your Financial Future

Paying off a long-term loan faster is more than just a financial goal; it’s a path to peace of mind and true financial freedom. The 15-65-20 system, while not directly mentioned, shares the same core principle of intentional allocation. By understanding how EMIs are structured and employing disciplined strategies like making extra payments and increasing your EMI with your income, you can turn a decades-long commitment into a manageable, short-term goal. This approach not only saves you a fortune in interest but also allows you to reallocate those funds towards building wealth and securing your future. Start today by making a small change, and watch your debt disappear faster than you ever thought possible

Save Home Loan Interest Amount!

Use Home Loan Excel Calculator that will help you to Save Interest Amount on Home Loan EMI.

Click below button to download Home Loan EMI and Prepayment Calculator in Excel:

Watch how Home Loan Calculator in Excel Works

Income Tax Calculator App – FinCalC

For Income Tax Calculation on your mobile device, you can Download my Android App “FinCalC” which I have developed for you to make your income tax calculation easy.

What you can do with this mobile App?

- Calculate Income Tax for FY 2025-26 and previous FY 2024-25

- Enter estimated Investments to check income tax with Old and New Tax Regime

- Save income tax details and track regularly

- Know how much to invest more to save income tax

- More calculators including PPF, SIP returns, Savings account interest and lot more

/footer