How to Build Wealth on a ₹10,000 Salary is ne of the common asked questions on my YouTube Channel. Building wealth with Rs. 10,000 can feel complicated, but if you are disciplined, you can achieve good wealth with consistency. We will explore various investment options, from the safest to the most aggressive, and reveal the single most impactful investment you can make—in yourself. By the end of this post, you’ll have a clear, actionable plan to turn your small monthly contributions into a multi-crore portfolio over the long term.

First Step towards Starting Your Investment Journey

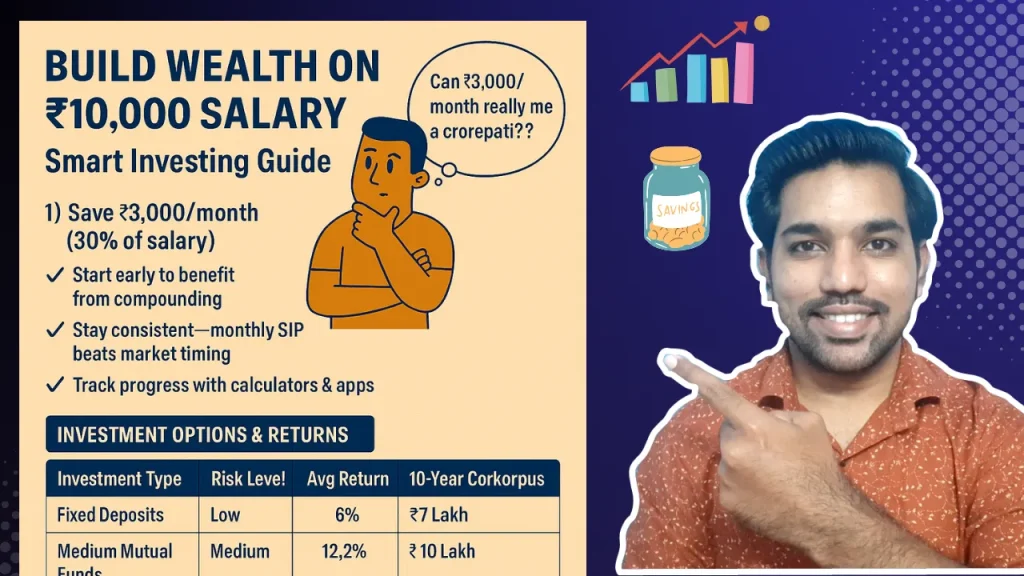

The first and most critical step is to cultivate the discipline of saving and investing a portion of your income consistently. You can dedicate 30% of a ₹10,000 salary to build wealth, which amounts to ₹3,000 per month, to investments. This principle of systematic, regular investment is far more effective than trying to time the market or save large, irregular sums. The earlier you start, the more you benefit from the incredible power of compounding, where your returns begin to generate their own returns, leading to exponential growth over decades.

The financial journey is not a sprint, it’s a marathon. Many people are confused by the complexity of the financial world, but the core principles are simple: save consistently, invest wisely, and stay patient. Let’s break down the different avenues available to you, starting with the most secure options and moving towards those with higher potential returns.

Investments Options For You

Safe and Secure: Understanding Fixed Deposits (FDs)

For many people, the concept of a Fixed Deposit (FD) is the entry point into investing. It is considered a safe option because your principal amount is guaranteed, and you receive a fixed rate of return. This makes it a popular choice for risk-averse investors. Check the Post Office Interest Rates here.

Historical Performance:

Historically, FDs in India have provided an average return of around 6%. While this rate may seem modest, its safety and predictability make it a cornerstone of a conservative portfolio.

The Power of Compounding with FDs:

Let’s see how a monthly investment of ₹3,000 would grow in a Fixed Deposit over a long period:

- After 10 years: Your corpus would be ₹7 lakh. However, due to inflation, the real value of this money would be only ₹5 lakh in today’s terms.

- After 20 years: The corpus would grow to ₹33 lakh, but its real value would be just ₹12 lakh.

- After 30 years: Your investment would reach ₹1 crore, with a real value of only ₹23 lakh.

- After 40 years: The corpus would be ₹3.34 crore, with a real value of ₹50 lakh.

This analysis highlights a critical lesson: while FDs are safe, they often struggle to beat inflation. While they are a good tool for short-term savings or a portion of your emergency fund, they may not be the most effective vehicle for long-term wealth creation.

Medium Risk, High Reward: The Path of Mutual Funds

For those willing to take on a moderate amount of risk for the potential of higher returns in order to Build Wealth on salary, mutual funds offer a fantastic solution. Instead of directly investing in individual stocks, you can entrust your money to a professional fund manager who diversifies your investment across a basket of stocks. This approach reduces risk and leverages professional expertise.

The index mutual funds, which are passive funds that track a specific market index. This means their returns are directly tied to the performance of the companies within that index.

- Nifty 50 Index Fund: This fund invests in the top 50 companies of India. It is considered a relatively lower-risk mutual fund option as it is highly diversified and includes the most stable and well-established companies. Historically, the Nifty 50 has averaged returns of around 11.8% CAGR for last 15 Years.

- Mid-Cap Index Fund (e.g., Nifty Mid-Cap 100): This fund invests in mid-sized companies. While these companies are more volatile than large-caps, they often have higher growth potential. This fund carries a higher risk but can offer better long-term returns, averaging around 14.24% historically.

- Small-Cap Index Fund (e.g., Nifty Small-Cap 250): This fund invests in small-sized companies and is the most volatile and riskiest of the three. However, it also has the highest potential for explosive growth, with historical average returns of around 18.28%.

Watch Video Playlist: Mutual Funds for Beginners

Creating a Balanced Portfolio:

A balanced, medium-risk portfolio can be created by allocating your monthly ₹3,000 investment across these funds. A conservative-to-moderate split: 70% in Nifty 50, 20% in Mid-Cap, and 10% in Small-Cap can be allocated to achieve the financial goals.

Projected Returns with a Medium-Risk Portfolio:

- After 10 years: Your corpus could grow to ₹10 lakh, with a real value of ₹7 lakh. This is already a significant improvement over the FD option.

- After 20 years: The corpus could reach ₹63 lakh, with a real value of ₹24 lakh.

- After 30 years: You could accumulate ₹3 crore, with a real value of ₹80 lakh.

- After 40 years: Your wealth could balloon to ₹14 crore, with a real value of ₹2 crore.

This illustrates the immense power of equity investing over the long term, even with a small monthly investment.

ALSO READ: How to Start SIP Online

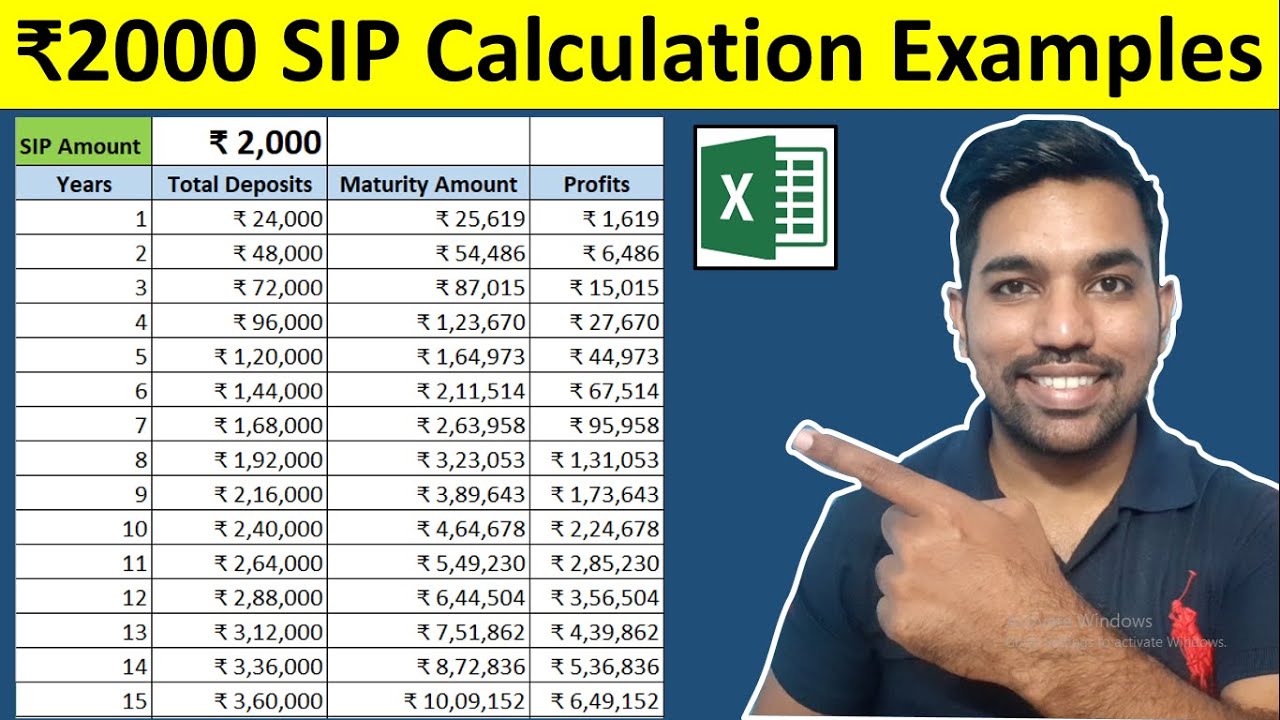

Rs. 2000 Mutual Fund Returns Calculation Video

Watch more Videos on YouTube Channel

Above video shows how you can invest via SIP in Mutual Funds to Build wealth on Salary every month, by being consistent.

The High-Risk, High-Reward Strategy: An Aggressive Mutual Fund Portfolio

For young investors in their 20s and early 30s who have a long investment horizon and a higher risk tolerance, an aggressive portfolio can be a game-changer. This strategy leverages the high growth potential of small and mid-cap companies.

Aggressive Portfolio Allocation:

The suggested allocation for this strategy is 10% in Nifty 50, 20% in Mid-Cap, and a significant 70% in Small-Cap. This portfolio is more volatile and will experience larger swings, but over decades, the potential for wealth creation is enormous.

Projected Returns with an Aggressive Portfolio:

- After 10 years: Your corpus could reach ₹13 lakh, with a real value of ₹8 lakh.

- After 20 years: You could become a millionaire, as your corpus could grow to ₹1 crore, with a real value of ₹36 lakh.

- After 30 years: The corpus could soar to ₹6.7 crore, with a real value of ₹1.5 crore.

- After 40 years: Your wealth could potentially reach an astounding ₹40 crore, with a real value of ₹5.75 crore.

This strategy demonstrates how a disciplined, long-term approach to investing can turn a modest salary into incredible wealth. Note that the small caps and mid cap mutual funds have higher risk and are more volatile compared to large cap companies which are included in Nifty 50.

You can download the SIP and Lumpsum Returns Calculator in Excel to check the monthly Investment Returns:

The Ultimate Investment: Investing in Yourself

While market investments are crucial for building wealth, the single best investment you can ever make is in yourself. No market asset can match the returns you can get from increasing your knowledge, skills, and earning potential during your initial career.

The Power of Personal Growth:

The best way is to improve your skills in your job or doing side business that can help you earn more income. Increasing your monthly pay during the start of your career can help you invest more to get more returns. This shows that the most direct way to increase your wealth is to increase your ability to earn, followed by making investments.

How to Invest in Yourself:

Even if you only have a small amount of money to spare, you can use it to grow your skills. Instead of putting all ₹3,000 into the market, you can allocate a portion towards your personal and professional development. This could include:

- Online Courses: Investing in courses that teach you high-demand skills like digital marketing, coding, or data analysis.

- Books: Buying books on topics that can enhance your expertise or offer new perspectives.

- Networking: Attending events, conferences, or workshops to connect with professionals and learn from their experiences.

- Tools and Resources: Purchasing software, equipment, or other tools that can make you more efficient and productive in your work or side projects.

- Starting a Side Hustle: Using a small amount of capital to launch a side business that can generate a new stream of income.

The returns on these investments are not measured in percentages but in the exponential growth of your earning capacity.

Comparison Table: A Side-by-Side Look at Your Options

| Investment Option | Risk Level | Expected Annual Return | 10-Year Corpus (₹) | 40-Year Corpus (₹) |

| Fixed Deposits (FDs) | Low | 6% | 7 Lakh | 3.34 Crore |

| Medium Mutual Funds | Medium | 12.2% | 10 Lakh | 14 Crore |

| Aggressive Mutual Funds | High | 16.5% | 13 Lakh | 40 Crore |

| Investing in Yourself | Varies | Unquantifiable | Exponential Earning Growth | Unquantifiable |

Note: The expected returns for mutual funds are an average of the index funds mentioned. The actual returns may vary based on market conditions.

Conclusion

Building a multi-crore portfolio from a modest salary is not an impossible dream; it is a very real possibility with the right knowledge and discipline. By committing to a consistent monthly investment of even a small amount like ₹3,000, you are setting the stage for incredible financial growth. While Fixed Deposits provide a safe haven, the real wealth-building potential lies in the stock market and mutual funds through disciplined, long-term investing.

Ultimately, the most powerful tool in your financial arsenal is your own potential. Investing in your skills, knowledge, and ability to earn will always provide the highest, most consistent returns. By combining smart market investments with a continuous commitment to personal growth, you can transform your financial trajectory and secure a future of abundance and freedom. The journey begins now—with your next paycheck.

Some more Reading:

- What is Equity Mutual Funds

- 4 Signs your are Doing Well Financially

- 5 Habits of Rich People that will change your Life

Frequently Asked Questions

Is it too late to start investing if I’m already in my 30s or 40s?

It is never too late to start. While starting early gives you a significant advantage due to compounding. Consistent and disciplined investing at any age will yield far better results than not investing at all. The key is to start now, no matter how small the amount.

How do I choose between different mutual funds?

For a beginner, it is highly recommended to start with index funds as they are passively managed and have lower fees. Once you are comfortable, you can do more research or consult a financial advisor to explore actively managed funds or a more customized portfolio.

What if the market crashes? Won’t I lose all my money in mutual funds?

Market volatility is a normal part of investing. While the value of your portfolio may decrease during a crash, a long-term perspective is crucial. Market history shows that markets have always recovered and reached new highs over time. The best strategy is to continue your monthly investments during a downturn, as you will be buying assets at a lower price.

Should I invest in a lump sum or through a Systematic Investment Plan (SIP)?

For someone with a salary of ₹10,000, a Systematic Investment Plan (SIP) is the best approach. It allows you to invest a fixed amount regularly, which helps in rupee cost averaging, meaning you buy more units when the price is low and fewer when the price is high, reducing your average cost over time.

What are the risks of investing in small-cap funds?

Small-cap funds are highly volatile. They are more susceptible to market downturns and can experience significant price swings. While they have the potential for very high returns, they also carry a higher risk of capital loss in the short term. They are best suited for investors with a long-term horizon (10+ years) who can ride out the market fluctuations.

Save Home Loan Interest Amount!

Use Home Loan Excel Calculator that will help you to Save Interest Amount on Home Loan EMI.

Click below button to download Home Loan EMI and Prepayment Calculator in Excel:

Watch how Home Loan Calculator in Excel Works

Income Tax Calculator App – FinCalC

For Income Tax Calculation on your mobile device, you can Download my Android App “FinCalC” which I have developed for you to make your income tax calculation easy.

What you can do with this mobile App?

- Calculate Income Tax for FY 2025-26 and previous FY 2024-25

- Enter estimated Investments to check income tax with Old and New Tax Regime

- Save income tax details and track regularly

- Know how much to invest more to save income tax

- More calculators including PPF, SIP returns, Savings account interest and lot more

Use Popular Calculators:

- Income Tax Calculator

- Home Loan EMI Calculator

- SIP Calculator

- PPF Calculator

- HRA Calculator

- Step up SIP Calculator

- Savings Account Interest Calculator

- Lump sum Calculator

- FD Calculator

- RD Calculator

- Car Loan EMI Calculator

- Bike Loan EMI Calculator

- Sukanya Samriddhi Calculator

- Provident Fund Calculator

- Senior Citizen Savings Calculator

- NSC Calculator

- Monthly Income Scheme Calculator

- Mahila Samman Savings Calculator

- Systematic Withdrawal Calculator

- CAGR Calculator

I’d love to hear from you if you have any queries about Personal Finance and Money Management.

JOIN Telegram Group and stay updated with latest Personal Finance News and Topics.

Download our Free Android App – FinCalC to Calculate Income Tax and Interest on various small Saving Schemes in India including PPF, NSC, SIP and lot more.

Follow the Blog and Subscribe to YouTube Channel to stay updated about Personal Finance and Money Management topics.