You can Achieve Financial Independence Retire Early (FIRE) by following 7 steps such as Starting SIP early, staying consistent and disciplined, step up your SIP amounts every year, keeping expenses low, becoming debt free, knowing your FIRE number and starting SWP in your retirement phase. These steps help you to Achieve Financial Independence Retire Early (FIRE) before the age of 60 years of age.

Let us understand this in more detail.

What is Financial Independence Retire Early?

- Financial Independence Retire Early (FIRE) consists of two things – “Financial Independence” and “Retire Early”. This is the term used when you become financially independent and can retire before the normal age of 60 years

- Gone are the days when you had to work for 60 years before you reach the retirement phase. Now people achieve financial freedom before the age of 60 years.

- So if you are in your 40s or 50s, you can achieve financial Independence and have the option of either continue to work or get engaged in your passion

- After attaining financial Independence, you can work on your passion as well that can provide you some side income to cover your monthly expenses

- So FIRE or Financial Independence Retire Early helps you to live your dream life since you no longer work for money and can get good returns from your investments or the side hustle you have started

Let us now understand how you can achieve Financial Independence Retire Early step by step.

How to Achieve Financial Independence Retire Early?

Below are the 7 steps to Achieve Financial Independence Retire Early (FIRE) at whatever age you are currently at. If you are in your 20s, you’ll achieve FIRE quickly in your life as compounding helps you to grow your money and returns

1. Start SIP Early

- The first step towards Achieving Financial Independence Retire Early is to Start SIP (Systematic Investment Plan)

- SIP is a way to invest in mutual funds or stocks, in which case you deposit specific amount in mutual funds every month for a period of time longer than 5 years to 7 years

- The Equity mutual fund helps you in compounding which is directly propotional to the time period you invest for

- Let;s say for exampl, if you start SIP of Rs. 10,000 at the age of 25 years and invest up to your age of 50 years, your total accumulated amount at the age of 50 years will be almost Rs. 1.89 Crore at 12% expected rate of returns

- On the other hand, if you start investing at 35 years of age upto 50 years, your accumulated corpus will be Rs. 50 Lakh. That’s 3.5 times less than the amount when you had started at 25 years of age

| Items | Age = 25 Years | Age = 35 Years |

|---|---|---|

| SIP Amount | Rs. 10,000 | Rs. 10,000 |

| Investing Time Period | 25 Years | 15 Years |

| Total Amount at 50 Years of Age | Rs. 1.89 Crore | Rs. 50 Lakh |

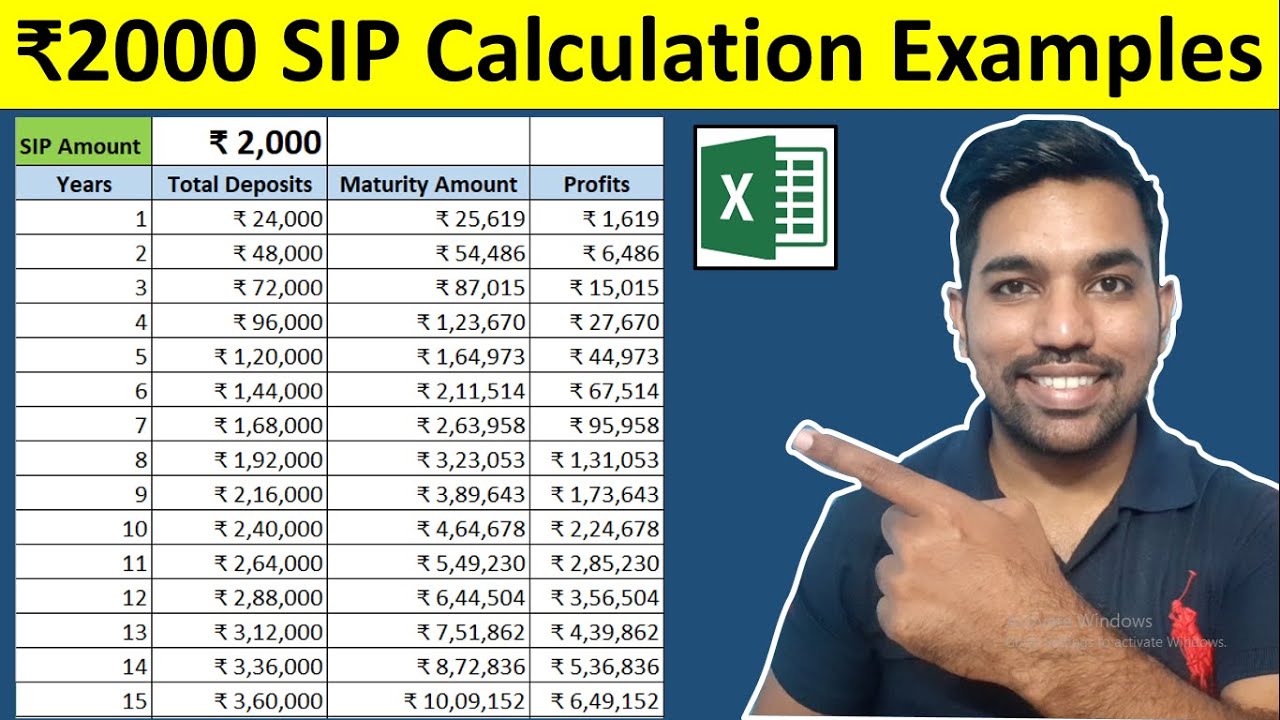

Rs. 2000 SIP Returns Calculation for 15 Years

Watch more Videos on YouTube Channel

2. Stay Consistent and Disciplined

- Starting SIP is one thing, but staying consistent is equally important

- As seen in above example, just by staying in the market for 15 years you accumulate Rs. 50 Lakh. By staying for more 10 years in the market, you reached 3.5 times more.

- This is how staying consistent and disciplined whill help you to see magic of compounding

- It takes long time to reach your first Rs. 1 crore and might take a long time, but Rs. 2 crore will take less time, Rs. 3 crore will be more faster, and so on every subsequent crore amount will take less and less time. This is only because your accumulated funds are working for you and showing the magic of compounding over time. You just need to stay consistent

3. Step up your Investments

- SIP with fixed amount is good, but Step up SIP is better

- Step up SIP is a way to increase your SIP amount after every year by let’s say 10% or by a fixed amount, so that you save more in order to achieve FIRE before time

- So if we take same example like above and you start investing Rs. 10000 per month at the age of 25 years

- Now let’s say after every year, you increase the SIP amount by Rs. 1000 due to salary increment or bonus

- So by age of 50 years, at 12% expected rate of returns, your accumulated amount would be around Rs. 3.14 Crore

- This is dues to more deposits you have made over time, and the compounding helps you to grow your money

4. Keep Expenses in control

- It’s very easy to increase your monthly expenses due to increase in your income after every year due to job switch, promotion, salary increment or bonus

- You need to control such increase in expenses due to lifestyle inflation

- Lifestyle inflation is the term used when your monthly expenses increases due to your lifestyle. Let’s say for example, you go for new movie every month. Now after a year, the price of the movie tickets would increase due to inflation. Since this example can be included your lifestyle, this increase in the price of the movie tickets can be considered as lifestyle inflation

- Now, you don’t have control on the inflation part of this. But what you can control is reducing the number of times you go to watch movies

- So, instead of going every month, you can go once in 2 months. This will help you to keep your expenses in control

ALSO READ: Bad Money Habits you should Avoid

5. Become Debt Free

- Now once you have reduced your spendings, it is also important to become debt free

- So, if you have taken home loan or car loan, make sure that you make loan prepayments to reduce your total interest amount to be paid

- The main idea is to close your loans before time and become debt free so that you can achieve Financial Independence

- Loans or Debt are the important instruments here which might delay your financial independence

6. Know your FIRE Number

- FIRE number helps you to know the amount you should have in your mutual fund portfolio

- Your FIRE number depends on your monthly or yearly expenses

- For example, if your monthly expenses is Rs. 50,000 which makes your yearly expenses as Rs. 6 Lakh, than you need to multiply this number by 25 to get your FIRE number which tells you the accumulated corpus you must have. In this case, your portfolio amount in mutual fund must be at least Rs. 1.5 Crore

FIRE Number Formula = Yearlt expenses * 25- In above formula, 25x is the minimum number you should use. You can also increase this number to 30 times or 40 times. This will give you some margin of safety as well.

- Next step is to start SWP with the help of 4% withdrawal rule

7. Start SWP

- SWP or Systematic Withdrawal Plan is the ultimate step for which you were working towards

- After you have worked hard to continue SIP over the years, you accumulated good amount of corpus in the mutual fund portfolio. This can help you to withdraw systematically at 4% withdrawal rate

- The rule of 4% in SWP states that you need to withdraw maximum of 4% from your mutual fund portfolio every year, in order to cover your expenses and also to increase the portfolio amount due to expected returns you generate at approximately 12% per year

- For example, if you have accumulated Rs. 1.5 crore, 4% of this amount will be Rs. 6 Lakh which should cover your yearly expenses. If this amount does not cover the expenses, you need to increase the accumulated corpus in mutual fund

- So follow the 4% rule in any case based on your yearly expenses and adjust your mutual fund portfolio amount accordingly

So these were the 7 steps to achieve Financial Independence Retire Early.

Some more Reading:

Save Home Loan Interest Amount!

Use Home Loan Excel Calculator that will help you to Save Interest Amount on Home Loan EMI.

Click below button to download Home Loan EMI and Prepayment Calculator in Excel:

Watch how Home Loan Calculator in Excel Works

Income Tax Calculator App – FinCalC

For Income Tax Calculation on your mobile device, you can Download my Android App “FinCalC” which I have developed for you to make your income tax calculation easy.

What you can do with this mobile App?

- Calculate Income Tax for FY 2025-26 and previous FY 2024-25

- Enter estimated Investments to check income tax with Old and New Tax Regime

- Save income tax details and track regularly

- Know how much to invest more to save income tax

- More calculators including PPF, SIP returns, Savings account interest and lot more

Use Popular Calculators:

- Income Tax Calculator

- Home Loan EMI Calculator

- SIP Calculator

- PPF Calculator

- HRA Calculator

- Step up SIP Calculator

- Savings Account Interest Calculator

- Lump sum Calculator

- FD Calculator

- RD Calculator

- Car Loan EMI Calculator

- Bike Loan EMI Calculator

- Sukanya Samriddhi Calculator

- Provident Fund Calculator

- Senior Citizen Savings Calculator

- NSC Calculator

- Monthly Income Scheme Calculator

- Mahila Samman Savings Calculator

- Systematic Withdrawal Calculator

- CAGR Calculator

I’d love to hear from you if you have any queries about Personal Finance and Money Management.

JOIN Telegram Group and stay updated with latest Personal Finance News and Topics.

Download our Free Android App – FinCalC to Calculate Income Tax and Interest on various small Saving Schemes in India including PPF, NSC, SIP and lot more.

Follow the Blog and Subscribe to YouTube Channel to stay updated about Personal Finance and Money Management topics.