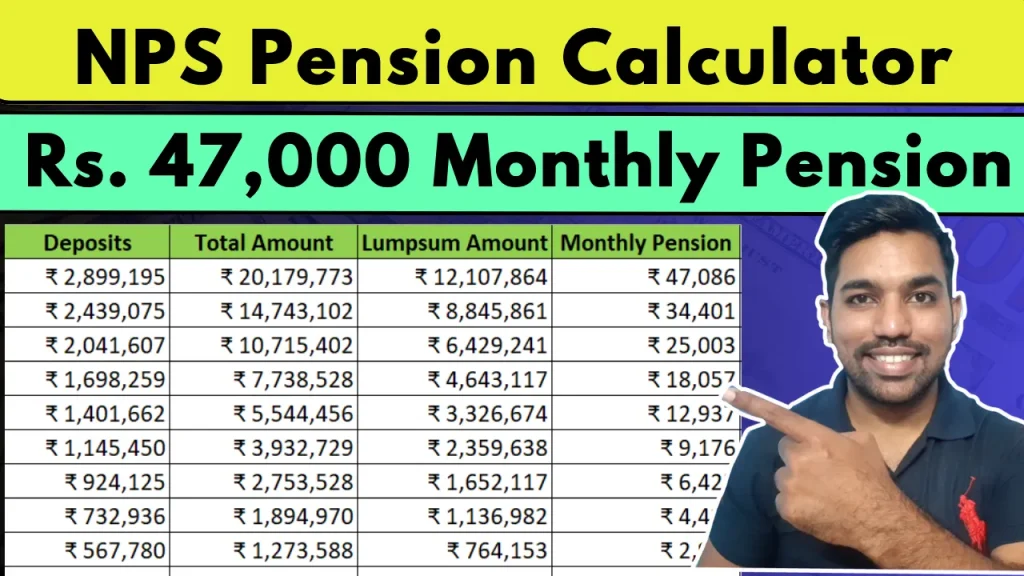

Retirement planning is not a one-year or even a five-year goal; it is a critical, decades-long journey that should ideally begin the moment you receive your first salary. In the quest for a financially secure and stress-free retirement, the National Pension System (NPS) stands out as one of the most powerful, yet often underutilized, tools available to the Indian taxpayer and investor. You can get monthly pension using NPS of approx. Rs. 47,000 when you start NPS account at the age of 20.

The NPS is a government-backed retirement scheme designed to provide a steady, reliable monthly pension after the age of 60. Unlike traditional retirement vehicles, NPS offers a unique blend of market-linked returns, flexibility, and significant tax advantages across three critical phases: contribution, accumulation, and withdrawal.

Let us understand NPS and pension calculation in more detail.

NPS Pension Calculation Video

Watch more Videos on YouTube Channel

NPS Eligibility, Structure, and Market Link

Understanding the core structure of the National Pension System is the first step toward building a robust retirement corpus. The NPS is fundamentally a defined contribution scheme that uses the power of the market for long-term wealth creation.

Eligibility and Contribution Timeline

The NPS is designed to be accessible to a wide range of individuals, promoting a culture of early and consistent saving.

- Eligibility: Any resident Indian citizen, salaried or self-employed, between the ages of 18 and 70 can open an NPS account.

- Contribution Period: Contributions can be made up to the age of 60, after which the retirement phase begins. However, subscribers can choose to defer their withdrawal or continue contributions up to the age of 85.

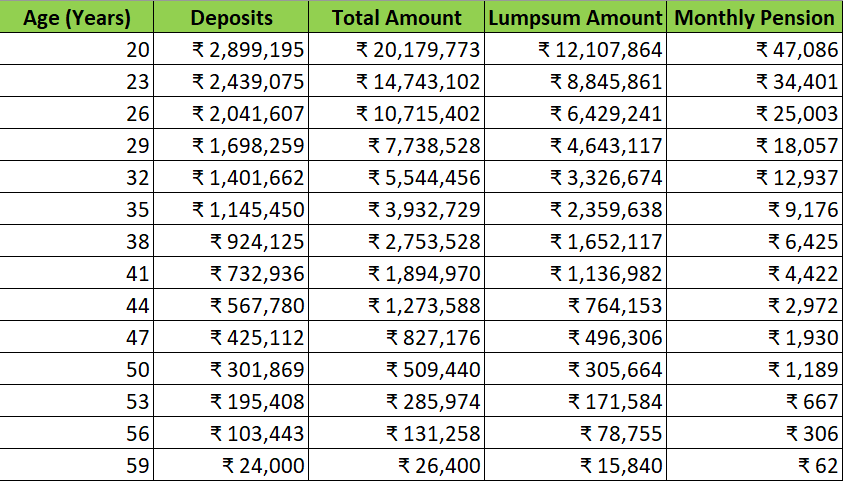

- The Power of Starting Early: Based on above video, the single most impactful factor in retirement wealth is the duration of investment. A person starting at 20 gains an additional 5 years of compounding compared to a person starting at 25. This early start generates a substantially larger corpus and, consequently, a higher monthly pension later during retirement phase.

USE NPS Pension Calculator

Market-Linked Returns and Fund Management

A crucial feature that separates NPS from fixed-return retirement products like the Public Provident Fund (PPF) is its market-linked nature.

- Expected Returns: While past performance is not a guarantee, NPS accounts have historically generated returns in the range of 9% to 15% per annum. This variability is linked to the performance of the Indian economy and financial markets.

- Tier I vs. Tier II Accounts:

- Tier I Account: This is the primary pension account. Contributions here are eligible for tax deductions, and the funds are locked in until retirement (with some exceptions for partial withdrawal).

- Tier II Account: This is a voluntary savings account. It offers flexibility to withdraw money at any time, but contributions are generally not eligible for tax deductions (except for central government employees under specific conditions).

- Asset Allocation Flexibility (E, C, G): NPS allows subscribers to choose how their money is invested across three main asset classes:

- Asset Class E (Equity): High-growth, high-risk investments, primarily in stock markets.

- Asset Class C (Corporate Bonds): Medium-risk investments in corporate debt.

- Asset Class G (Government Securities): Low-risk investments in government debt, providing stability.

Subscribers can choose between two investment strategies:

- Active Choice: The subscriber determines the percentage allocation across E, C, and G, allowing for higher exposure to equity (E) for younger investors.

- Auto Choice (Life Cycle Fund): The asset mix is automatically adjusted based on the subscriber’s age. Equity exposure automatically decreases as the subscriber approaches retirement, shifting funds towards the safer G (Government Securities) class. This is often recommended for individuals who prefer a hands-off approach to risk management.

There are few changes proposed to be done in NPS accounts, watch below video for more details

NPS Rule Changes October 2025 Video

NPS Tax Advantages with Old and New Tax Regime

One of the most compelling reasons to invest in NPS is the significant income tax relief it provides, making it an efficient vehicle for simultaneously saving for retirement and reducing current tax liability. The NPS offers tax benefits under multiple sections, applicable to both self-contribution and employer contribution.

The Power of Self-Contribution (Section 80CCD(1B))

This is the most popular and distinct tax deduction available exclusively through NPS.

- Deduction Limit: An additional deduction of up to ₹50,000 over and above the ₹1.5 lakh limit under Section 80C/80CCD(1) is available for self-contributions to the Tier I NPS account.

- Tax Regimes: This deduction is available only under the Old Tax Regime. For high-income earners operating under the old regime, this ₹50,000 deduction can lead to significant tax savings, pushing the total tax-saving potential (including Section 80C) to ₹2 lakh.

Leveraging the NPS Employer Contribution (Section 80CCD(2))

This deduction is crucial, especially for salaried individuals, as it is available under both the Old and New Tax Regimes, making it a primary tax-saving option for those opting for the New Regime.

| Tax Regime | Maximum Deduction Limit (Employer Contribution) | How It Works |

| Old Tax Regime | 10% of Basic Salary + Dearness Allowance (DA) | The employer’s contribution (up to the limit) is deductible from the employee’s taxable income. |

| New Tax Regime | 14% of Basic Salary + DA | The maximum deduction limit for Central Government employees is 14% of basic salary plus DA. For private and state government employees, the limit remains 10%. |

Example of Employer Contribution:

If an employee’s basic monthly salary is ₹50,000:

- Old Regime Maximum Deduction: 10% of ₹50,000 = ₹5,000 per month, or ₹60,000 annually.

- New Regime (if applicable at 14%) Maximum Deduction: 14% of ₹50,000 = ₹7,000 per month, or ₹84,000 annually.

This provision enables employees to get a deduction on a non-taxable employer contribution, making NPS a powerful tool to lower the effective taxable income, even in the New Tax Regime, where most other traditional deductions are unavailable. This is particularly relevant for individuals aiming to reduce a high taxable income (e.g., above ₹12 lakh) to maximize their post-tax wealth.

ALSO READ: How to Calculate Income Tax in India with Examples

Retirement Payout Strategy: The Crucial 60% and 40% Rule

The moment of truth for any retirement plan is the withdrawal phase. The NPS features a specific rule governing the withdrawal of the accumulated corpus at the age of 60, focusing on providing both an immediate lump sum and a guaranteed monthly income.

Lump Sum Withdrawal (Maximum 60%)

Upon reaching the retirement age (60), the NPS subscriber is allowed to withdraw a maximum of 60% of the total accumulated corpus as a tax-free lump sum.

- Tax Status: This portion of the withdrawal is 100% tax-free.

- Purpose: This amount provides immediate liquidity for retirement needs, such as settling remaining debts, funding a large purchase, or creating an emergency reserve.

- Calculation Example: If the total NPS corpus at age 60 is ₹2.01 Crore, the maximum lump sum withdrawal is 60%, or approximately ₹1.21 Crore (Tax-Free).

Mandatory Annuity Investment (Minimum 40%)

The remaining minimum 40% of the corpus must be used to purchase an Annuity Plan from an Annuity Service Provider (ASP). This is the mechanism that converts the accumulated corpus into a fixed, reliable monthly pension.

- What is an Annuity? An annuity is a financial product sold by insurance companies. The subscriber hands over a lump sum (the 40% corpus), and in return, the provider guarantees a fixed stream of income (pension) for a specified period, often for life.

- Annuity Rate (Interest Rate): The annuity rate (the effective interest rate on the invested corpus) typically ranges from 5% to 8% and is locked in at the time of purchase. A higher annuity rate directly translates to a higher monthly pension.

- Calculation Example: Using the previous example, if the remaining 40% corpus is ₹80.4 lakh, and the assumed annuity rate is 7%, the yearly income would be approximately ₹5.63 lakh, translating to a monthly pension of around ₹47,000.

- Tax Implications of Pension: Unlike the lump-sum withdrawal, the monthly pension received from the annuity is fully taxable as income according to the pensioner’s applicable income tax slab.

| NPS Withdrawal Component | Maximum Percentage | Tax Status | Purpose |

| Lump Sum Withdrawal | 60% | 100% Tax-Free | Immediate liquidity and financial cushioning. |

| Annuity Investment | Minimum 40% | Pension is Fully Taxable | Guaranteed, stable monthly income for life. |

The Exception for Small Corpus: If the total corpus at age 60 is ₹5 lakh or less, the subscriber is allowed to withdraw the entire amount as a lump sum without purchasing an annuity.

ALSO READ: 15-65-20 Rule of Financial Freedom

Compounding Advantage with NPS

Based on above video, time in the market is more valuable than trying to save a large amount later. This is the cornerstone of effective retirement planning.

The Penalty for Starting Late: Age vs. Corpus

Assuming a starting contribution of ₹2,000 per month, an annual contribution escalation of 5%, and an expected return of 10%, the drop in the final corpus and pension due to a late start is staggering.

| Starting Age | Retirement Age | Contribution Duration | Total Contribution (Approx.) | Final Corpus (Approx.) | Monthly Pension (7% Annuity) |

| 20 Years | 60 | 40 Years | ₹29 Lakh | ₹2.01 Crore | ₹47,000 |

| 23 Years | 60 | 37 Years | ₹26 Lakh | ₹1.61 Crore | ₹34,401 |

| 25 Years | 60 | 35 Years | ₹24 Lakh | ₹1.31 Crore | ₹27,826 |

| 30 Years | 60 | 30 Years | ₹19 Lakh | ₹74 Lakh | ₹15,741 |

| 35 Years | 60 | 25 Years | ₹15 Lakh | ₹39 Lakh | ₹8,382 |

Conclusion from Data: A delay of just 5 years (from 20 to 25) reduces the final corpus by approximately 35% (from ₹2.01 Cr to ₹1.31 Cr). The money lost due to missing five years of compounding is impossible to fully recover through increased contributions alone later in life.

Power of Step up Contributions

The analysis also reveals how consistently increasing the contribution—known as step-up SIP—can supercharge the corpus, compensating for a slightly later start.

If an investor starts at age 25 with ₹2,000/month but increases the contribution by 10% annually (instead of 5%), the results drastically improve:

| Starting Age | Annual Contribution Step-Up | Monthly Pension (7% Annuity) | Total Corpus (Approx.) |

| 25 Years | 5% (Standard) | ₹27,826 | ₹1.31 Crore |

| 25 Years | 10% (Aggressive) | ₹55,000 | ₹2.61 Crore |

By merely doubling the annual step-up rate from 5% to 10%, the final corpus and the resulting monthly pension effectively double as well. This emphasizes the need for investors to align their NPS contributions with their annual salary hikes, ensuring the investment keeps pace with their rising income and the economic growth of the country.

Applying Inflation and Market Optimism

A truly effective retirement plan must account for the eroding power of inflation. The monthly pension of ₹50,000 that feels substantial today may be insufficient 30 years from now.

The Inflation Challenge

Inflation, typically hovering between 5% and 6% in India, means that the cost of living doubles roughly every 12 to 14 years. When calculating retirement needs, the investor must project current monthly expenses into the future.

- Future Value Calculation: An individual whose current monthly expenses are ₹40,000 and who has 30 years until retirement, must assume their expenses will inflate to roughly ₹2,28,978 per month (assuming a 6% average inflation rate).

- Contribution Goal: Therefore, the retirement planning goal must be to secure a monthly pension at least equal to this future expense, necessitating a significantly higher monthly contribution today.

The NPS calculator is an essential tool here. By adjusting the required future monthly pension (e.g., aiming for ₹2.5 lakh instead of ₹1 lakh), the calculator determines the current monthly contribution needed, allowing the investor to tailor their savings to their lifestyle.

The Effect of Optimized Market Returns

While 10% is a conservative, safe assumption for long-term NPS returns, a slightly higher return (e.g., 12%) significantly accelerates wealth creation.

- Impact of 2% Higher Return: In the example of the 25-year-old starting with ₹4,000/month and a 10% annual step-up:

- At 10% Return: Final Corpus = ₹5.21 Crore; Monthly Pension = ₹1.1 Lakh

- At 12% Return: Final Corpus = ₹7.25 Crore; Monthly Pension = ₹1.5 Lakh

A mere two-percentage-point difference in the long-term annual return can increase the final corpus and pension by over 38%. This underscores the importance of actively managing the NPS asset allocation (E, C, G) and considering a higher equity (E) exposure during the initial decades of the investment journey to capture higher market-linked returns.

The Final Takeaway

The NPS is more than just a savings product; it is a structured financial instrument that combines tax efficiency, market upside, and forced discipline for retirement planning. Its advantages are clear and compelling:

- Triple Tax Benefit: Deductions under Section 80CCD(1), 80CCD(1B), and 80CCD(2).

- EET (Exempt-Exempt-Taxable) Status: Contributions are exempt, the accumulation is exempt, and only the annuity portion of the withdrawal is taxed (the largest lump-sum is tax-free).

- Forced Discipline: The lock-in nature of the Tier I account ensures that the retirement corpus remains untouched, preventing pre-mature expenditure.

- Liquidity in Retirement: The 60% tax-free lump-sum withdrawal provides immediate financial freedom.

The primary conclusion from all analysis is simple: Start now, and step up aggressively. The difference between a comfortable retirement and a financially constrained one is often measured in the few early years of compounding missed. Use the powerful tools and tax deductions the NPS provides to build the multi-crore corpus necessary to defeat inflation and secure a monthly income that truly supports your golden years.

Some more Reading:

Frequently Asked Questions

What is the minimum and maximum age to open an NPS account?

Any resident Indian citizen, salaried or self-employed, between the ages of 18 and 70 can open a Tier I NPS account. While the standard retirement age is 60, subscribers can defer the purchase of an annuity or continue contributing up to the age of 75. The video analysis strongly suggests starting at the youngest possible age (18 or upon first employment) to maximize the decades-long benefit of compounding.

What happens to the corpus if I decide to retire before the age of 60?

If you choose to exit NPS before the age of 60 (premature withdrawal), the rules are much stricter:

- You must utilize a minimum of 80% of the accumulated corpus to purchase an annuity.

- You can withdraw the remaining 20% as a lump sum.

- Crucially, this lump sum withdrawal of 20% is fully taxable in the year of withdrawal. Premature exit is therefore highly discouraged due to the tax penalty and reduced lump-sum amount.

How is the lump-sum withdrawal at age 60 treated for tax purposes?

Up to 60% of the total accumulated corpus at the age of 60 can be withdrawn as a lump sum, and this amount is 100% tax-free. For example, if your corpus is ₹2 crore, the ₹1.2 crore lump sum is entirely exempt from tax, making this a highly tax-efficient component of the NPS.

Is the monthly pension I receive from the annuity tax-free?

No. While the 60% lump sum withdrawal is tax-free, the monthly pension you receive from the annuity (purchased with the remaining 40% minimum corpus) is fully taxable. This pension income is added to your other income and taxed according to your applicable income tax slab rate for that financial year.Q5: Can I claim tax benefits under the New Tax Regime by investing in NPS?

Yes, you can claim a significant tax deduction under the New Tax Regime, but only on the employer’s contribution to your NPS account. Under Section 80CCD(2), the employer’s contribution (up to 10% of Basic Salary + DA, or 14% for Central Government employees) is deductible from your taxable income. This deduction is one of the few available tax benefits under the simplified New Tax Regime, making NPS a key tax planning tool for salaried employees regardless of the regime they choose. The additional ₹50,000 self-contribution deduction (80CCD(1B)) is not available in the New Tax Regime.

If I am starting late (e.g., at age 35), how can I catch up on the missed years of compounding?

The best way to mitigate the penalty of a late start is to focus on two levers:

- Increase Initial Contribution: Start with a higher monthly contribution (e.g., ₹4,000 instead of ₹2,000).

- Aggressive Step-Up/Escalation: Commit to a higher annual increase in your contribution (e.g., 10% instead of 5%) to align with your salary growth. The video calculation shows that a 10% annual escalation can dramatically increase the final corpus, potentially doubling the eventual monthly pension compared to a flat 5% escalation.

What is the NPS rule if my corpus is very small at retirement?

If your total NPS corpus is ₹5 lakh or less at the time of your retirement (age 60), you are not required to purchase an annuity. You can withdraw the entire 100% of the accumulated amount as a tax-free lump sum. This rule is in place to ensure that very small annuities, which would result in a negligible monthly pension, are avoided.

Save Home Loan Interest Amount!

Use Home Loan Excel Calculator that will help you to Save Interest Amount on Home Loan EMI.

Click below button to download Home Loan EMI and Prepayment Calculator in Excel:

Watch how Home Loan Calculator in Excel Works

Income Tax Calculator App – FinCalC

For Income Tax Calculation on your mobile device, you can Download my Android App “FinCalC” which I have developed for you to make your income tax calculation easy.

What you can do with this mobile App?

- Calculate Income Tax for FY 2025-26 and previous FY 2024-25

- Enter estimated Investments to check income tax with Old and New Tax Regime

- Save income tax details and track regularly

- Know how much to invest more to save income tax

- More calculators including PPF, SIP returns, Savings account interest and lot more

Use Popular Calculators:

- Income Tax Calculator

- Home Loan EMI Calculator

- SIP Calculator

- PPF Calculator

- HRA Calculator

- Step up SIP Calculator

- Savings Account Interest Calculator

- Lump sum Calculator

- FD Calculator

- RD Calculator

- Car Loan EMI Calculator

- Bike Loan EMI Calculator

- Sukanya Samriddhi Calculator

- Provident Fund Calculator

- Senior Citizen Savings Calculator

- NSC Calculator

- Monthly Income Scheme Calculator

- Mahila Samman Savings Calculator

- Systematic Withdrawal Calculator

- CAGR Calculator

I’d love to hear from you if you have any queries about Personal Finance and Money Management.

JOIN Telegram Group and stay updated with latest Personal Finance News and Topics.

Download our Free Android App – FinCalC to Calculate Income Tax and Interest on various small Saving Schemes in India including PPF, NSC, SIP and lot more.

Follow the Blog and Subscribe to YouTube Channel to stay updated about Personal Finance and Money Management topics.