With improved lifestyle, taking high interest loans are not uncommon. But this can lead to multiple problems that include high repayment Cost, Debt trap and Financial Stress, credit score impact, limited financial freedom and higher risk of default. Such problems can be difficult to come out from over long term, and hence the high interest loans must be avoided.

Let us understand the problems of taking high interest loans and what can be the solution to avoid such problems.

1. High Repayment Costs

- High interest rate loans means you have to pay higher interest amounts over the loan tenure or loan period

- This will lead to the major part of your EMI (Equated Monthly Installment) to go into interest payments

- Remember that the interest rate is applied on your principal amount to calculate the interest amount of any month

- So, when the interest rate of principal amount is high, you have to pay high interest amounts thus resulting in skyrocketing repayment cost for you

- At the end of the loan tenure, you end up paying more interest amount compared to the principal amount you had borrowed

ALSO READ: Home Loan Calculation Method

2. Debt Trap & Financial Stress

- When you pay high interest amount due to high interest rate, you enter into debt trap that seem to be very difficult to come out from

- Your salary or income is limited and if almost 50% of the income is going into paying high interest loans, you would have less amount to cover for other household expenses

- This leads to financial stress if there is any emergency that pops up that needs urgent funds

- This is also called debt trap, in which case, you want to close the loan as son as possible but couldn’t do it since you are already paying high interest amount on it and the journey seems to be very long

- To come out of such situations, many borrowers try to take more loans to cover for the existing loans, only to make the situation worse

- Yes, you can take another loan only when the interest rate is lower than the existing loan but not otherwise

- Constant financial stress can impact mental well-being and quality of life

3. Impact on Credit Score

- If you miss payment of any EMI for any month, it can badly impact your credit score

- Credit score is the measure for banks and financial institutions to assess your loan repayment history, so that they can lend you more loans

- But if the credit score is impacted negatively, due to missed or late payments, you will not be qualified for future loans

- This can avoid you from taking important financial decisions such as buying a new house or a new car on loan

ALSO WATCH: Buy vs Rent a House Which is Better [Excel Calculator]

4. Limited Financial Freedom

- Due to EMI payments, your other financial goals such as saving or investing in mutual funds or stocks are restricted

- You are forced to live on paycheck to paycheck, just thinking about your next salary hitting the bank account

- Savings or investing is important for your long term financial stability which get impacted due to high interest loans

- In such cases, your cash flow might also be impacted, making it difficult to cover for monthly expenses

5. Higher Risk of Default

- The burden of paying high interest loans can increase the risk of defaults

- Defaulting or loans or non payment of EMIs can lead to legal consequences and repossession of assets being taken away from you

- Always remember, the material you take on loan is not yours until you pay the loan amount in full, and is owned by bank or financial institution, whether it is new house, new car or anything else

- So it becomes yours only when you close the loan after paying all the EMIs

- So such risk of defaults can also lead to long term financial instability

ALSO READ: 5 Ways to Save Money on Monthly Bills

What Can You Do Instead?

So what is the solution of paying high interest loans. Below are some of the solutions:

- Go for low interest rate loans to pay less interest amounts

- Improve financial planning and budgeting to minimize the need for loans. It is better to stop taking loans rather than managing multiple of them at once

- Explore other investment alternatives or emergency funds to avoid completely relying on the loans you have to take forcefully. This is only possible with proper financial planning and budgeting

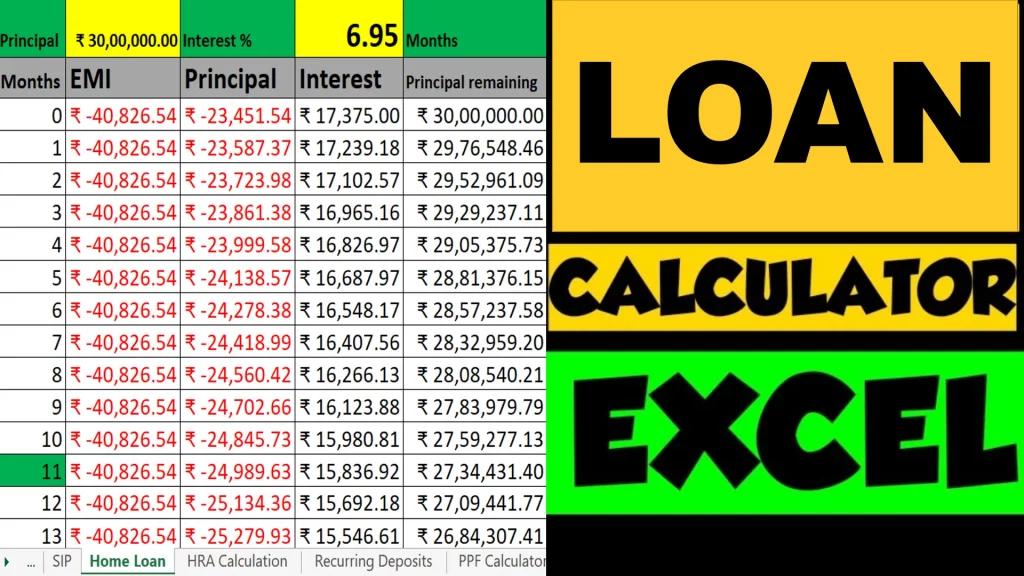

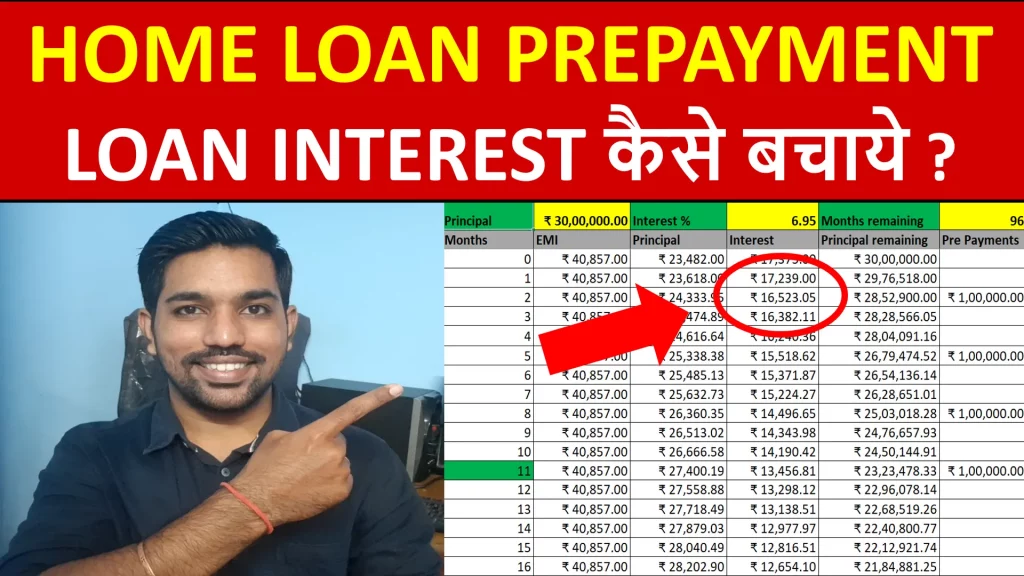

Save Home Loan Interest Amount!

Use Home Loan Excel Calculator that will help you to Save Interest Amount on Home Loan EMI.

Click below button to download Home Loan EMI and Prepayment Calculator in Excel:

Watch how Home Loan Calculator in Excel Works

Income Tax Calculator App – FinCalC

For Income Tax Calculation on your mobile device, you can Download my Android App “FinCalC” which I have developed for you to make your income tax calculation easy.

What you can do with this mobile App?

- Calculate Income Tax for FY 2025-26 and previous FY 2024-25

- Enter estimated Investments to check income tax with Old and New Tax Regime

- Save income tax details and track regularly

- Know how much to invest more to save income tax

- More calculators including PPF, SIP returns, Savings account interest and lot more

Use Popular Calculators:

- Income Tax Calculator

- Home Loan EMI Calculator

- SIP Calculator

- PPF Calculator

- HRA Calculator

- Step up SIP Calculator

- Savings Account Interest Calculator

- Lump sum Calculator

- FD Calculator

- RD Calculator

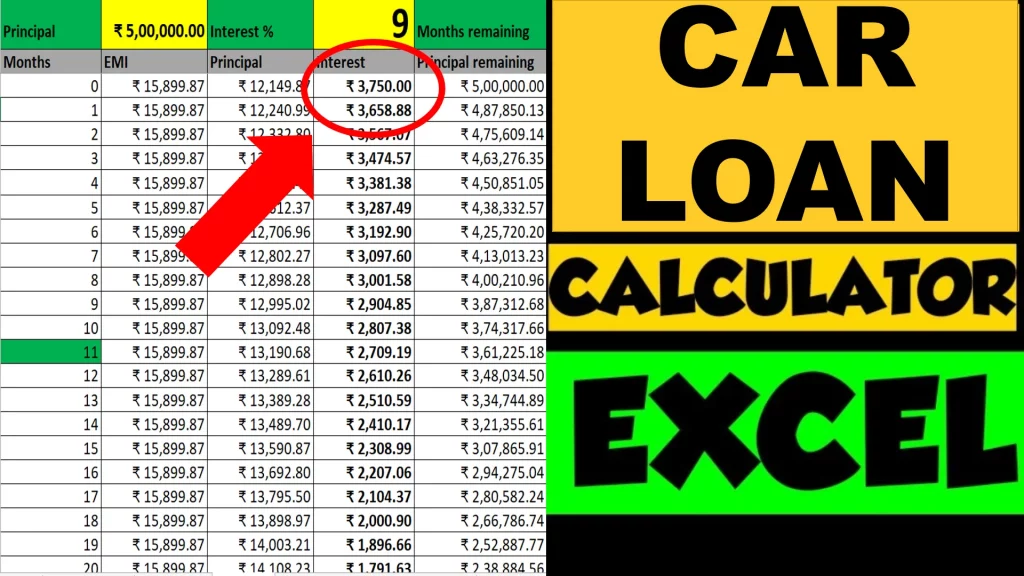

- Car Loan EMI Calculator

- Bike Loan EMI Calculator

- Sukanya Samriddhi Calculator

- Provident Fund Calculator

- Senior Citizen Savings Calculator

- NSC Calculator

- Monthly Income Scheme Calculator

- Mahila Samman Savings Calculator

- Systematic Withdrawal Calculator

- CAGR Calculator

I’d love to hear from you if you have any queries about Personal Finance and Money Management.

JOIN Telegram Group and stay updated with latest Personal Finance News and Topics.

Download our Free Android App – FinCalC to Calculate Income Tax and Interest on various small Saving Schemes in India including PPF, NSC, SIP and lot more.

Follow the Blog and Subscribe to YouTube Channel to stay updated about Personal Finance and Money Management topics.