In the modern financial situation, the dream of a regular and consistent income stream that doesn’t rely on your day-to-day work, such as a job, has captured the imagination of millions. This concept, often referred to as passive income, is an important step of long-term financial freedom. 5 ways to generate passive income includes Fixed Deposit Interests, SWP for monthly income from mutual funds, Real Estate, buying bonds and P2P lending.

Let us understand each of them in detail.

1. Generating Income from Fixed Deposits

For generations, the Fixed Deposit (FD) has been the go-to savings vehicle for Indian households. It represents the investment of safety and predictability. When you open an FD, you are essentially lending a lump sum of money to a bank for a fixed period, and in return, the bank pays you a predetermined rate of interest. This interest can be received on a regular basis (e.g., monthly, quarterly, or annually), making it a reliable source of regular income.

The process is straightforward: you invest your capital, and it remains secure, insulated from the volatility of the stock market or other risky assets. The principal amount is guaranteed by the bank, making it a “no-risk” option in terms of capital preservation. The interest rates on FDs typically range from 4-6% annually, offering a consistent, stream of income.

However, to truly understand the FD, one must look beyond the headline interest rate. The real challenge with FDs lies in their inability to keep pace with inflation. Inflation is the rate at which the general level of prices for goods and services is rising, and subsequently, the purchasing power of currency is falling. In many economies, including India, the average annual inflation rate hovers around 6% or higher. When your FD is earning 5% interest while inflation is at 6%, your money is actually losing value in real terms. The purchasing power of your investment today will be less tomorrow.

Let’s illustrate with an example. If you invest ₹1 lakh in an FD at a 5% interest rate, you will earn ₹5,000 in interest over a year. But if a product that costs ₹1 lakh today will cost ₹1,06,000 in a year due to inflation, your investment has not grown; it has simply stayed behind.

Furthermore, the interest earned on an FD is taxable. For many, this interest is taxed at their marginal tax rate, which can be as high as 30%. This means the actual post-tax return is significantly lower. An FD earning a gross return of 6% might only provide a post-tax, inflation-adjusted return of 0% or even negative.

Therefore, the Fixed Deposit is not an investment product for wealth creation; it is a safety product for capital preservation. Its primary use case is for money you cannot afford to lose, such as an emergency fund or capital needed in the short term. While it generates a regular income, it is a poor long-term strategy for building real wealth that outpaces inflation.

2. Using a Systematic Withdrawal Plan (SWP) from Equities

For those with a higher risk tolerance and a longer time horizon, the stock market, through instruments like mutual funds, offers a more dynamic way to generate a regular income. While direct stock market trading is often speculative and complex, a Systematic Withdrawal Plan (SWP) from a well-diversified mutual fund portfolio provides a structured and disciplined way to get paid from your investments.

An SWP is the reverse of a Systematic Investment Plan (SIP). With an SIP, you invest a fixed amount of money every month into a mutual fund. With an SWP, you withdraw a fixed amount of money every month from your mutual fund portfolio. The money you initially invested continues to grow, and you simply draw down a small portion of it and its returns on a regular basis.

The core benefit of this approach is that the stock market has historically provided returns that significantly outperform inflation over the long term. A well-diversified equity mutual fund, such as one tracking a major index like the Nifty 50, has provided average returns of over 10% annually. This means your capital is not just generating income; it is also growing. A portion of that growth can be converted into a regular income stream through the SWP.

However, the major downside is market volatility. The stock market is not a straight line; it goes up and down. If you set up an SWP and the market experiences a downturn, you might be forced to withdraw money when the value of your mutual fund units is low. To get your fixed withdrawal amount, you would have to sell a larger number of units. This can significantly erode your principal, making it difficult for the remaining investment to recover and grow. If a prolonged bear market occurs, you could deplete your portfolio much faster than anticipated.

This risk makes an SWP a potentially dangerous strategy for a younger investor who needs a regular income to cover their living expenses. It is a strategy best suited for a large, established corpus, such as a retirement fund, where the goal is to draw down a small, sustainable percentage (e.g., 4% annually) of a very large portfolio. The SWP is not a solution for everyone, and its success is contingent on a long-term perspective and a deep understanding of market cycles.

SWP for Monthly Income Video

Watch more Videos on YouTube Channel

3. Real Estate and REITs

Investing in real estate has long been a traditional way to generate a regular income, typically through rental payments. This strategy offers a powerful combination of two income streams: rental yield and capital appreciation. Rental yield is the annual income from rent as a percentage of the property’s value. Capital appreciation is the increase in the property’s market value over time.

For example, if you buy a property for ₹1 crore and it generates ₹3 lakh in annual rental income, your rental yield is 3%. If the property’s value appreciates by 5% in that same year, your total return is a respectable 8%. Unlike an FD, this return often beats inflation and provides a tangible, physical asset that can be used or sold.

However, the major hurdle to direct real estate investment is the large lump sum required upfront. Buying a commercial or residential property is a significant financial undertaking, often requiring a substantial down payment and a long-term loan. This makes it an inaccessible option for most individuals with limited capital. Additionally, being a landlord comes with its own set of challenges, including property maintenance, finding and managing tenants, dealing with vacancies, and paying property taxes.

Fortunately, there is a modern and accessible alternative: Real Estate Investment Trusts (REITs). A REIT is a company that owns, operates, or finances income-producing real estate. You can think of it as a mutual fund for real estate. Instead of buying a whole building, you can buy shares of a REIT, which gives you fractional ownership of a portfolio of properties. These properties, such as office spaces, shopping malls, or data centers, generate rental income, and the REIT is legally required to distribute a significant portion of this income (typically 90%) to its shareholders in the form of a regular dividend.

Investing in REITs is a game-changer because it eliminates the high entry barrier of direct real estate. You can start investing in REITs with as little as a few hundred or thousand rupees, making it accessible to virtually anyone. You also get the benefit of professional management, as the REIT’s team handles all the property management and tenant issues. However, there’s a crucial distinction: while you receive regular dividends from the rental income, you do not get the benefit of direct property appreciation. The share price of a REIT can go up or down based on market conditions, but it’s not a direct reflection of the physical property’s appreciating value.

REITs are a powerful tool for generating a regular income stream from a diversified portfolio of real estate assets without the complexities and high costs of direct ownership. They provide liquidity, meaning you can easily buy and sell shares, unlike a physical property which can take months to sell.

ALSO READ: Home Loan Calculation Method with Prepayment Calculator

4. Bonds: The Bridge Between Safety and Risk

Bonds represent a middle ground between the guaranteed but low returns of FDs and the higher but volatile returns of equities. When you buy a bond, you are essentially lending money to a company or a government. In return for your loan, the issuer of the bond promises to pay you a fixed rate of interest, known as the coupon payment, at regular intervals for a set period. At the end of the bond’s term, your original principal is returned to you.

Bonds are an attractive option for generating a regular income because they offer a higher return than FDs, with a predictable payment schedule. A good quality corporate bond might offer an annual return of 9-11%, which is significantly better than the 4-6% offered by most FDs and often comfortably beats inflation. The payments can be structured to be paid out every six months, providing a reliable and substantial income stream.

However, the main risk associated with bonds is the possibility of default. The company you lend money to might not be able to pay back the interest or the principal. This is where credit ratings become crucial. Credit rating agencies, such as CRISIL, ICRA, and CARE in India, evaluate the financial health and creditworthiness of companies and assign them a rating. A rating of ‘AAA’ signifies the highest safety and lowest risk of default, while a lower rating like ‘B’ or ‘C’ indicates a higher risk.

The higher the risk, the higher the interest rate the company will offer to compensate investors for taking on that risk. A highly-rated company might offer a lower interest rate, while a lower-rated company might offer a much higher rate. The key is to find a balance between risk and reward. Experts recommend sticking to bonds with a strong rating, such as an ‘A’ rating or higher, to minimize the risk of losing your capital.

Today, platforms like Wint Wealth and GoldenPi have made it easier than ever for retail investors to access the bond market. These platforms vet the companies and provide all the necessary information, including the credit rating, so you can make an informed decision. Investing in bonds is a smart way to diversify your portfolio and generate a predictable income stream that can be a powerful component of your financial strategy.

ALSO READ: Financial Planning for Millennials with Step by Step Guide

5. High-Yield, High-Risk: P2P Lending

In recent years, a new class of investment has emerged, promising high returns and regular income: Peer-to-Peer (P2P) lending and invoice discounting. These digital platforms connect lenders directly with borrowers, bypassing traditional financial institutions.

P2P lending platforms allow you to lend money to individuals or small businesses in exchange for a fixed, high rate of interest. For example, platforms like the 12% Club market themselves by offering a daily return of 12%. The appeal is clear: a high, consistent return without the volatility of the stock market. Some platforms even offer the ability to withdraw your money at any time without penalty, adding to their appeal.

Invoice discounting is a similar concept where you purchase a company’s unpaid invoices at a discount. When the invoice is eventually paid, you receive the full amount, earning a profit.

While the promise of a 12% return is enticing, it’s essential to approach these options with extreme caution. The primary risk is the lack of transparency and the high probability of default. Unlike a bond from a publicly-traded company with a credit rating, the underlying assets and borrowers in P2P lending and invoice discounting platforms can be opaque. If a borrower defaults on their loan, you could lose your entire investment. The high returns are offered to compensate for this high risk.

These are high-risk instruments and should only be considered by seasoned investors who understand the risks involved and are prepared to lose their capital.

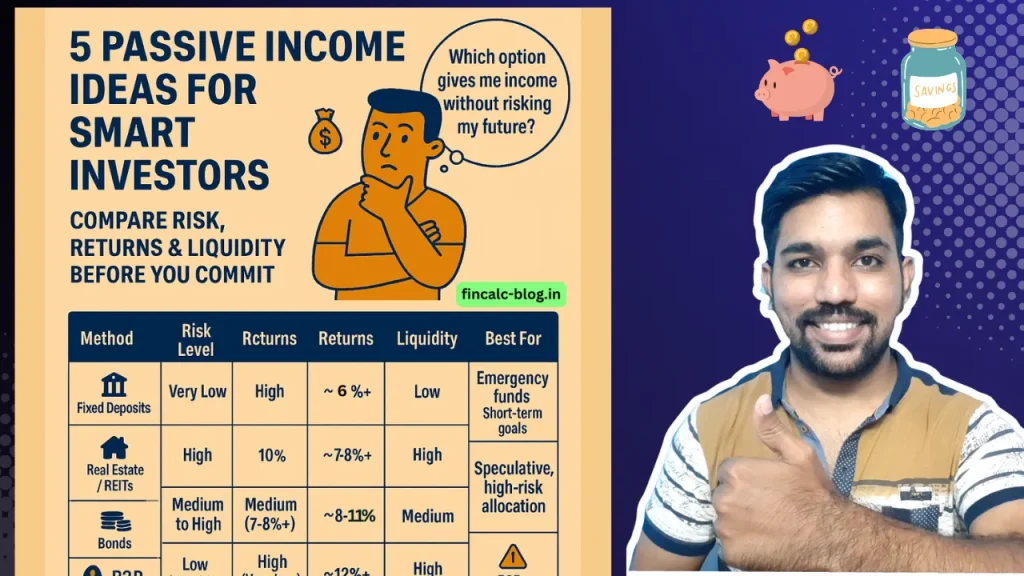

Comparison of Income-Generating Investment Options

| Feature | Fixed Deposits (FDs) | Equities (SWP) | Real Estate & REITs | Bonds | P2P Lending & Invoice Discounting |

| Required Capital | Low | Low to High | Very High (Direct) / Low (REITs) | Low to Medium | Low |

| Risk Level | Very Low | High | Medium to High (Direct) / Medium (REITs) | Low to Medium | Very High |

| Regular Income | Fixed & Predictable | Variable & Market-dependent | Rental Income / Dividends | Fixed & Predictable | Fixed (but risky) |

| Potential Return | Low (4-6%) | High (10%+ average) | Medium (7-8%+ average) | Medium (8-11%) | Very High (12%+) |

| Liquidity | Low (penalties for early withdrawal) | High (can be withdrawn easily) | Very Low (Direct) / High (REITs) | Medium | High (as marketed) |

| Inflation Beating | No | Yes | Yes | Yes (Generally) | Yes (but with high risk) |

| Best For | Emergency Funds, Short-term Goals | Long-term Wealth Creation & Retirement | Portfolio Diversification | Stable, Predictable Income | Speculative, High-Risk Allocation |

Conclusion

Generating a regular, predictable income from your investments is a powerful step towards achieving financial independence. While the world of finance offers a diverse array of options, from the safety of Fixed Deposits to the high-risk, high-return potential of P2P lending, there is no one-size-fits-all solution.

The key to success lies in understanding the core mechanics of each option, evaluating its alignment with your risk tolerance, and creating a diversified portfolio that can withstand market fluctuations while meeting your income needs. A well-constructed portfolio may include a blend of low-risk assets like FDs and bonds for stability, along with a growth-oriented allocation to equities and REITs.

Remember, the most valuable asset in your financial journey is your own knowledge. Take the time to educate yourself, read about different investment strategies, and understand the nuances of each instrument. By doing so, you take control of your financial future and transform your hard-earned savings into a powerful engine for generating consistent wealth and providing yourself with the ultimate gift of financial freedom. The journey begins with a single, well-informed step.

Some more Reading:

Frequently Asked Questions (FAQ)

Which is the best passive income option?

There is no single “best” option. The ideal choice depends on your personal financial situation, including your risk tolerance, your income needs, and your investment time horizon. For a conservative investor, a mix of FDs and high-quality bonds might be suitable. A younger investor with a long-term outlook might prefer a portfolio heavily weighted towards equities and REITs. The best strategy is often a diversified one that combines multiple options.

What exactly is the difference between an FD and a bond?

The fundamental difference lies in who you are lending money to and the associated risk. When you invest in an FD, you are lending money to a bank, which is highly regulated and provides a near-guaranteed return. When you invest in a bond, you are lending money to a company or government, and there is a risk of default, however small. While FDs typically offer a lower return, bonds often provide a higher return to compensate for this added risk.

Is it safe to invest in bonds?

Bonds can be a very safe investment, provided you do your due diligence. The most crucial step is to check the credit rating of the bond issuer. Sticking to bonds with an ‘A’ rating or higher significantly reduces the risk of default. It is also wise to diversify your bond investments across different companies and sectors.

How can I start investing in REITs and bonds without a large sum of money?

The accessibility of these instruments has increased dramatically with the advent of online platforms. You can invest in REITs by purchasing units through a broker, much like you would buy a stock. For bonds, platforms like Wint Wealth and GoldenPi have made it possible to buy individual bonds or bond baskets with relatively low minimum investments. You can start with just a few thousand rupees and build your portfolio over time.

What is the main danger of using a Systematic Withdrawal Plan (SWP) from an equity fund?

The primary danger is sequence of return risk. This means that if you start withdrawing money early in a bear market (when returns are negative), your capital can be depleted much faster than anticipated. This is because you have to sell more units at a lower price to get the same income. A prolonged downturn at the beginning of your withdrawal phase can be catastrophic for your long-term portfolio.

Save Home Loan Interest Amount!

Use Home Loan Excel Calculator that will help you to Save Interest Amount on Home Loan EMI.

Click below button to download Home Loan EMI and Prepayment Calculator in Excel:

Watch how Home Loan Calculator in Excel Works

Income Tax Calculator App – FinCalC

For Income Tax Calculation on your mobile device, you can Download my Android App “FinCalC” which I have developed for you to make your income tax calculation easy.

What you can do with this mobile App?

- Calculate Income Tax for FY 2025-26 and previous FY 2024-25

- Enter estimated Investments to check income tax with Old and New Tax Regime

- Save income tax details and track regularly

- Know how much to invest more to save income tax

- More calculators including PPF, SIP returns, Savings account interest and lot more

Use Popular Calculators:

- Income Tax Calculator

- Home Loan EMI Calculator

- SIP Calculator

- PPF Calculator

- HRA Calculator

- Step up SIP Calculator

- Savings Account Interest Calculator

- Lump sum Calculator

- FD Calculator

- RD Calculator

- Car Loan EMI Calculator

- Bike Loan EMI Calculator

- Sukanya Samriddhi Calculator

- Provident Fund Calculator

- Senior Citizen Savings Calculator

- NSC Calculator

- Monthly Income Scheme Calculator

- Mahila Samman Savings Calculator

- Systematic Withdrawal Calculator

- CAGR Calculator

I’d love to hear from you if you have any queries about Personal Finance and Money Management.

JOIN Telegram Group and stay updated with latest Personal Finance News and Topics.

Download our Free Android App – FinCalC to Calculate Income Tax and Interest on various small Saving Schemes in India including PPF, NSC, SIP and lot more.

Follow the Blog and Subscribe to YouTube Channel to stay updated about Personal Finance and Money Management topics.