Imagine you are earning Rs. 12,00,000 a year. Your income tax is Rs. 0 — thanks to the Section 87A rebate under the new tax regime. Now imagine you get a small increment and your salary becomes Rs. 12,10,000. Without any protection, your tax would suddenly jump to Rs. 61,500. You earned Rs. 10,000 more, but you are paying Rs. 61,500 as tax. That means you actually take home less money than someone earning Rs. 12 Lakh.

This is exactly the unfair situation that Marginal Relief in Income Tax was designed to fix.

In this article, I will explain what marginal relief is, how it is calculated with real examples, who is eligible, and where it does not apply — so you know exactly where you stand.

- What is Marginal Relief in Income Tax?

- Income Tax Calculation with Marginal Relief Video

- Marginal Relief vs Section 87A Rebate – What is the Difference?

- Who is Eligible for Marginal Relief in FY 2025-26?

- How is Marginal Relief Calculated? (Step-by-Step)

- Marginal Relief Calculation Examples – FY 2025-26

- What Happens at Rs. 12,75,000 – The Cut-off Point

- Marginal Relief on Surcharge for High Income Earners

- Marginal Relief in Income Tax – Summary Table

- Does Marginal Relief Apply in FY 2026-27?

- Important Points to Remember About Marginal Relief

- Frequently Asked Questions on Marginal Relief

- Conclusion

What is Marginal Relief in Income Tax?

Marginal Relief is a provision in the Indian income tax system that ensures you never pay more tax than the extra income you earned above a tax-free threshold.

In simple words — if your income crosses the tax-free limit by a small amount, your additional tax cannot exceed that small additional income.

There are two situations where marginal relief applies in India:

- Situation 1 — When your taxable income is slightly above Rs. 12 Lakh under the new tax regime (FY 2025-26 and FY 2026-27)

- Situation 2 — When your taxable income is slightly above surcharge thresholds like Rs. 50 Lakh, Rs. 1 Crore, Rs. 2 Crore (both old and new tax regime)

Both situations follow the same core principle — you should never end up with less take-home money just because you earned a little more.

Income Tax Calculation with Marginal Relief Video

Watch more Videos on YouTube Channel

Marginal Relief vs Section 87A Rebate – What is the Difference?

Many people confuse these two. They are different things that work together.

- Section 87A Rebate — Available when your taxable income is up to Rs. 12 Lakh under new regime. The maximum rebate is Rs. 60,000. This makes your effective tax Rs. 0 if your taxable income is within Rs. 12 Lakh

- Marginal Relief — Kicks in when your taxable income exceeds Rs. 12 Lakh but only by a small amount. It limits your tax to only the amount by which your income exceeds Rs. 12 Lakh

Think of it this way — 87A rebate protects you up to Rs. 12 Lakh. Marginal relief protects you just above Rs. 12 Lakh, in the Rs. 12 Lakh to Rs. 12.75 Lakh range.

Who is Eligible for Marginal Relief in FY 2025-26?

- Resident individual taxpayers under the new tax regime

- Taxable income between Rs. 12,00,001 and Rs. 12,75,000

- Salaried employees, pensioners, and self-employed individuals all qualify

- Both FY 2025-26 and FY 2026-27 — the same rules apply since Budget 2026 made no changes to slab rates or rebate limits

Who is NOT eligible:

- Taxpayers under the old tax regime (marginal relief is not available in old regime)

- Non-Resident Indians (NRIs) are not eligible for Section 87A rebate and hence not eligible for this marginal relief either

- Income above Rs. 12,75,000 — marginal relief does not apply beyond this point

- Special income such as capital gains (STCG and LTCG) under sections 111A and 112A — these are taxed separately and are excluded

ALSO READ: Income Tax with STCG, LTCG and Salary Income

How is Marginal Relief Calculated? (Step-by-Step)

The formula is straightforward:

- Step 1 — Calculate your tax as per new regime slab rates on your actual income (without any rebate)

- Step 2 — Calculate the amount by which your income exceeds Rs. 12 Lakh

- Step 3 — Compare Step 1 tax and Step 2 excess income

- Step 4 — Marginal Relief = Step 1 Tax minus Step 2 Excess Income

- Step 5 — Your final tax = Step 1 Tax minus Marginal Relief = which equals the excess income from Step 2

In effect, your final tax equals exactly the amount by which your income exceeds Rs. 12 Lakh. Nothing more.

Let us understand marginal relief calculations with examples.

Marginal Relief Calculation Examples – FY 2025-26

Let me walk you through three real examples, the same ones CBDT has confirmed.

Example 1: Taxable Income = Rs. 12,10,000

| Items | Amount |

|---|---|

| Tax as per slabs (before rebate) | Rs. 61,500 |

| Income above Rs. 12 Lakh | Rs. 10,000 |

| Marginal Relief | Rs. 51,500 (Rs. 61,500 – Rs. 10,000) |

| Final Tax Payable | Rs. 10,000 |

| 4% Cess on Rs. 10,000 | Rs. 400 |

| Total Tax including Cess | Rs. 10,400 |

You earned Rs. 10,000 extra above Rs. 12 Lakh. You pay Rs. 10,000 as tax. Fair.

Example 2: Taxable Income = Rs. 12,50,000

| Amount | |

|---|---|

| Tax as per slabs (before rebate) | Rs. 67,500 |

| Income above Rs. 12 Lakh | Rs. 50,000 |

| Marginal Relief | Rs. 17,500 (Rs. 67,500 – Rs. 50,000) |

| Final Tax Payable | Rs. 50,000 |

| 4% Cess on Rs. 50,000 | Rs. 2,000 |

| Total Tax including Cess | Rs. 52,000 |

Example 3: Taxable Income = Rs. 12,70,000

| Amount | |

|---|---|

| Tax as per slabs (before rebate) | Rs. 71,500 |

| Income above Rs. 12 Lakh | Rs. 70,000 |

| Marginal Relief | Rs. 1,500 (Rs. 71,500 – Rs. 70,000) |

| Final Tax Payable | Rs. 70,000 |

| 4% Cess on Rs. 70,000 | Rs. 2,800 |

| Total Tax including Cess | Rs. 72,800 |

Notice what is happening — as your income approaches Rs. 12,75,000, the marginal relief shrinks. At Rs. 12,75,000, the slab-computed tax and the excess income become almost equal. Beyond that point, marginal relief no longer applies and you pay full tax as per slabs.

ALSO READ: Rs. 1000 Mutual Fund Returns Calculation for 15 Years

What Happens at Rs. 12,75,000 – The Cut-off Point

This is an important number for salaried employees specifically.

For salaried individuals who get a standard deduction of Rs. 75,000, a gross salary of Rs. 12,75,000 reduces to a taxable income of Rs. 12,00,000 — which is already fully covered under the Section 87A rebate, making tax Rs. 0.

But for those without standard deduction (like self-employed individuals or those with other income), Rs. 12,75,000 is the last point where marginal relief is available.

Beyond Rs. 12,75,000 of taxable income — whether you are salaried or not — full slab-rate tax applies with no marginal relief.

Use the Income Tax Calculator in Excel mentioned at the top of this Article, to calculate Income Tax with your ow numbers

Marginal Relief on Surcharge for High Income Earners

This is the second type of marginal relief that applies to higher income taxpayers — those earning above Rs. 50 Lakh.

When your income crosses a surcharge threshold, the jump in tax can be disproportionate. Marginal relief protects you here as well.

Surcharge rates under new tax regime:

| Income Range | Surcharge Rate |

|---|---|

| Up to Rs. 50 Lakh | Nil |

| Rs. 50 Lakh to Rs. 1 Crore | 10% |

| Rs. 1 Crore to Rs. 2 Crore | 15% |

| Above Rs. 2 Crore | 25% |

How marginal relief works on surcharge — Example:

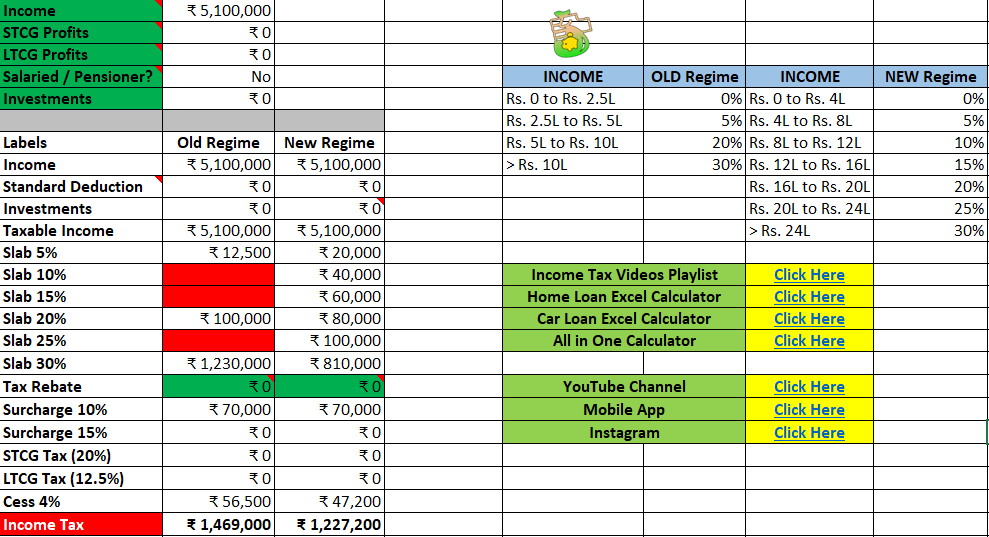

Suppose an individual earns Rs. 51 Lakh in FY 2025-26. With 10% surcharge applied, the total tax payable comes to Rs. 12,69,840. But if the same person had earned Rs. 50 Lakh, the tax would be Rs. 11,23,200. That means earning Rs. 1 Lakh extra results in Rs. 1,46,640 additional tax — which is more than the extra income earned.

This is where marginal relief on surcharge applies:

- Tax payable without marginal relief on Rs. 51 Lakh = Rs. 12,69,840

- Tax payable if income was Rs. 50 Lakh = Rs. 11,23,200

- Extra income earned = Rs. 1,00,000

- Extra tax without relief = Rs. 1,46,640

- Since extra tax (Rs. 1,46,640) is more than extra income (Rs. 1,00,000), marginal relief kicks in

- In this case when income is between 50 lakh to 1 crore, surcharge will be 70% of the difference between income minus 50 lakh, or tax calculated as per slab rates – whichever is lower

- Marginal Relief = Rs. 1,46,640 – 70% of Rs. 1,00,000 (Rs. 51 lakh – Rs. 50 lakh) = Rs. 76,640

- Final additional tax = Rs. ₹ 12,27,200

The same principle applies at the Rs. 1 Crore and Rs. 2 Crore thresholds as well.

Marginal relief is applicable in both the old tax regime and the new tax regime for surcharge purposes. In both regimes, surcharge rates increase when income crosses specified thresholds, and marginal relief limits the additional tax to the additional income earned above the threshold.

Marginal Relief in Income Tax – Summary Table

| Scenario | Income Range | Relief Available? |

|---|---|---|

| New Regime – Section 87A zone | Up to Rs. 12,00,000 | Full Rebate (Rs. 0 tax) |

| New Regime – Marginal Relief zone | Rs. 12,00,001 to Rs. 12,75,000 | Yes – tax capped at excess income |

| New Regime – Above cut-off | Above Rs. 12,75,000 | No marginal relief |

| Old Regime – Section 87A zone | Up to Rs. 5,00,000 | Full Rebate (Rs. 0 tax) |

| Old Regime – Marginal Relief | Not available | No |

| High Income – Surcharge threshold | Just above Rs. 50L / 1Cr / 2Cr | Yes – both regimes |

Does Marginal Relief Apply in FY 2026-27?

Yes. Budget 2026 retained the same tax framework as Budget 2025 for FY 2026-27, with no changes to income tax slabs or rebate limits. The same marginal relief provisions continue to apply in FY 2026-27 as well

So everything explained in this article is valid for both FY 2025-26 and FY 2026-27.

Important Points to Remember About Marginal Relief

- Marginal relief is automatically calculated — you do not need to separately claim it while filing your ITR. The tax computation already accounts for it

- It is not a deduction. It is a reduction in the tax liability itself. You Save Tax due to Marginal Relief benefit

- Capital gains income such as LTCG and STCG are excluded from marginal relief — these are taxed at special rates

- If your taxable income is above Rs. 12,75,000, do not expect marginal relief — calculate your full tax using the slab rates

- You should always calculate your tax both ways — with and without marginal relief — to verify your liability, or simply use the income tax calculator in excel mentioned above at the top of this article

Frequently Asked Questions on Marginal Relief

What is marginal relief in income tax in simple words?

If your income crosses the tax-free limit by a small amount, marginal relief ensures your tax cannot exceed that extra income. So you never take home less money just because you earned a little more.

Is marginal relief available under the old tax regime?

Marginal relief on surcharge is available under both old and new regimes. But the marginal relief linked to Section 87A rebate (for income around Rs. 12 Lakh) is only available under the new tax regime.

Up to what income is marginal relief available in FY 2025-26?

Marginal relief under Section 87A is available for taxable income between Rs. 12,00,001 and Rs. 12,75,000 under the new tax regime. Beyond Rs. 12,75,000, full slab-rate tax applies, since this will make you pay less income tax compared to marginal relief way of calculation

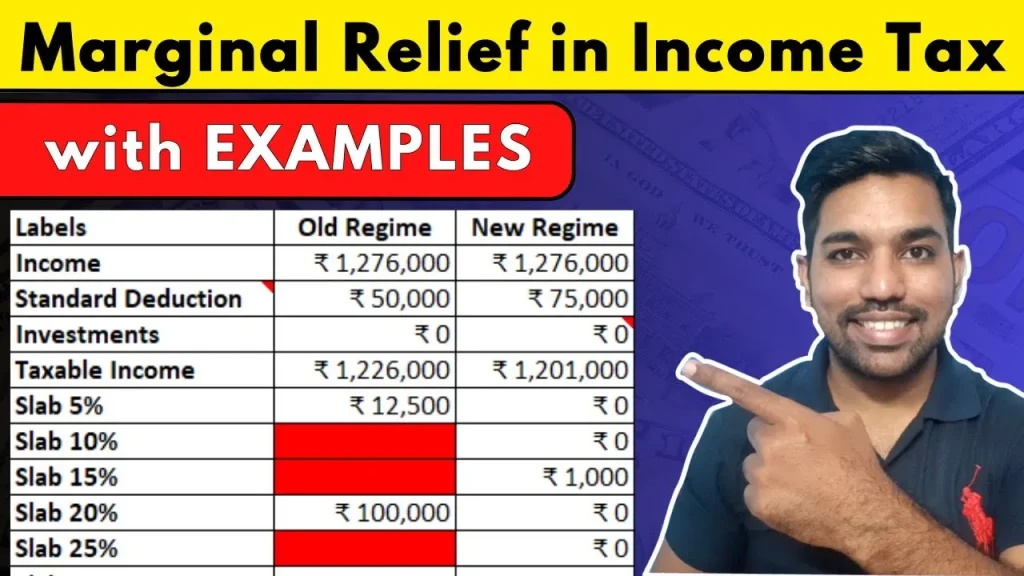

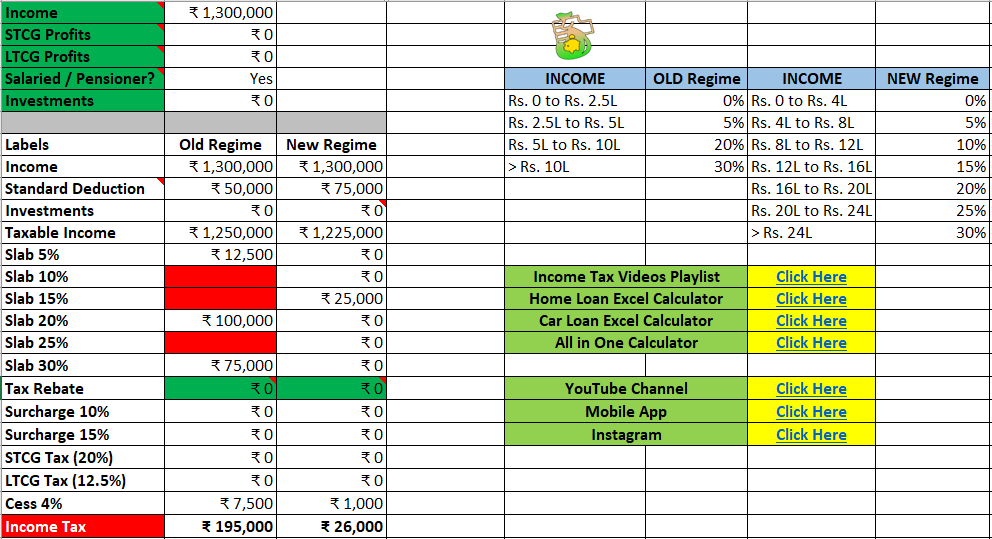

If my salary is Rs. 13 Lakh, do I get marginal relief?

If you are salaried, your taxable income after standard deduction of Rs. 75,000 is Rs. 12,25,000. Since this is between Rs. 12 Lakh and Rs. 12,75,000, marginal relief applies. Your tax will be limited to Rs. 25,000 (the amount by which Rs. 12,25,000 exceeds Rs. 12,00,000) plus 4% cess, so your effective income tax becomes Rs. 26,000 on Rs. 13 Lakh Income

Does marginal relief apply to capital gains income?

No. Capital gains under sections 111A, 112, and 112A are taxed at special rates and are excluded from the marginal relief calculation.

Conclusion

Marginal relief is one of those provisions that most salaried employees never hear about until they need it. If your income is in the Rs. 12 Lakh to Rs. 12.75 Lakh range this year, knowing about this provision can save you from unnecessarily paying higher tax than you should. Use the income tax calculator above to calculate your exact tax with marginal relief already factored in.

Save Home Loan Interest Amount!

Use Home Loan Excel Calculator that will help you to Save Interest Amount on Home Loan EMI.

Click below button to download Home Loan EMI and Prepayment Calculator in Excel:

Watch how Home Loan Calculator in Excel Works

Income Tax Calculator App – FinCalC

For Income Tax Calculation on your mobile device, you can Download my Android App “FinCalC” which I have developed for you to make your income tax calculation easy.

What you can do with this mobile App?

- Calculate Income Tax for FY 2025-26 and previous FY 2024-25

- Enter estimated Investments to check income tax with Old and New Tax Regime

- Save income tax details and track regularly

- Know how much to invest more to save income tax

- More calculators including PPF, SIP returns, Savings account interest and lot more

Use Popular Calculators:

- Income Tax Calculator

- Home Loan EMI Calculator

- SIP Calculator

- PPF Calculator

- HRA Calculator

- Step up SIP Calculator

- Savings Account Interest Calculator

- Lump sum Calculator

- FD Calculator

- RD Calculator

- Car Loan EMI Calculator

- Bike Loan EMI Calculator

- Sukanya Samriddhi Calculator

- Provident Fund Calculator

- Senior Citizen Savings Calculator

- NSC Calculator

- Monthly Income Scheme Calculator

- Mahila Samman Savings Calculator

- Systematic Withdrawal Calculator

- CAGR Calculator

I’d love to hear from you if you have any queries about Personal Finance and Money Management.

JOIN Telegram Group and stay updated with latest Personal Finance News and Topics.

Download our Free Android App – FinCalC to Calculate Income Tax and Interest on various small Saving Schemes in India including PPF, NSC, SIP and lot more.

Follow the Blog and Subscribe to YouTube Channel to stay updated about Personal Finance and Money Management topics.