Every month, when your salary gets credited, two deductions happen quietly in the background — your PF contribution and your employer’s PF contribution. Both go into your EPFO account. And sitting on top of all those accumulated contributions is an interest rate of 8.25% per year — better than most bank FDs — and fully tax-free in most cases.

But here is what most salaried employees never bother to check: how exactly is that PF interest calculated? When does it get credited? And how much will your PF balance actually be when you retire or when you need to withdraw?

I have explained PF interest calculation step by step below with real examples, the exact formula, current PF interest rate, and everything you need to know about PF withdrawal rules so you never have to guess about your own money.

You can also download the EPF Calculator in Excel to calculate the PF interest based on your PF balance and monthly contributions:

- What is PF – Provident Fund – and Why Does It Matter?

- PF Interest Calculation with Formula [VIDEO]

- PF Interest Rate – Current and Historical

- How is PF Contribution Calculated from Salary?

- PF Interest Calculation Formula

- PF Interest Calculation – Step by Step Example

- What is Your PF Balance – How to Check PF Balance

- PF Withdrawal Rules – When and How Much Can You Withdraw

- Tax on PF Withdrawal – What You Need to Know

- Is PF Interest Taxable?

- PF vs PPF – Key Differences

- Frequently Asked Questions on PF Interest Calculation

What is PF – Provident Fund – and Why Does It Matter?

PF stands for Provident Fund, also known as EPF — Employees Provident Fund. It is a mandatory retirement savings scheme managed by EPFO — the Employees’ Provident Fund Organization — under the Government of India.

If you work for a company with 20 or more employees, EPF is mandatory for you. Every month, both you and your employer contribute a fixed percentage of your salary to your EPF account. Over the years, these contributions build up into a retirement corpus — one that earns guaranteed interest every year, declared by EPFO.

Most employees just look at the PF deduction on their payslip and move on. Very few actually calculate what that corpus will look like in 10 or 20 years. When I show people the numbers, they are usually surprised at how large it gets.

You can watch below video on EPF Interest Calculation using the excel calculator I have mentioned above.

PF Interest Calculation with Formula [VIDEO]

Watch more Videos on YouTube Channel

PF Interest Rate – Current and Historical

The EPF interest rate for FY 2025-26 is fixed at 8.25% per annum. This rate applies to all contributions made between April 1, 2025 and March 31, 2026.

Here is how the PF interest rate has moved over the last several years:

| Financial Year | EPF Interest Rate |

|---|---|

| FY 2025-26 | 8.25% |

| FY 2024-25 | 8.25% |

| FY 2023-24 | 8.25% |

| FY 2022-23 | 8.15% |

| FY 2021-22 | 8.10% |

| FY 2020-21 | 8.50% |

| FY 2019-20 | 8.50% |

| FY 2018-19 | 8.65% |

- The EPF interest rate is reviewed every year by the Central Board of Trustees of EPFO in consultation with the Ministry of Finance

- Even in years when equity markets fell and bank FD rates dropped, EPFO has maintained a reasonably stable interest rate

- This consistency is what makes EPF one of the most reliable long-term savings instruments for salaried employees in India

How is PF Contribution Calculated from Salary?

Before we get to the PF interest calculation, let me explain how PF contribution itself works — because many employees are confused about what percentage goes where.

The employee’s EPF contribution is 12% of basic salary plus dearness allowance. The employer’s contribution of 12% is divided into two parts — 8.33% goes toward EPS (Employee Pension Scheme) and the balance 3.67% goes into the EPF account.

Example: Basic Salary + DA = Rs. 30,000 per month

| Contribution | Percentage | Amount |

|---|---|---|

| Employee contribution to EPF | 12% | Rs. 3,600 |

| Employer contribution to EPS | 8.33% (capped at Rs. 15,000 wage) | Rs. 1,250 |

| Employer contribution to EPF | 3.67% (capped at Rs. 15,000 wage) | Rs. 550 |

| Total into your EPF account per month | Rs. 4,150 |

- The wage ceiling for employer’s contribution calculation is Rs. 15,000 — so employer’s EPF and EPS are calculated on maximum Rs. 15,000 even if basic salary is higher

- Your own 12% contribution has no such cap — it is calculated on your actual basic + DA

- So if your basic salary is Rs. 50,000, your employee EPF contribution = Rs. 6,000 per month

- You can voluntarily contribute more than 12% — this is called VPF (Voluntary Provident Fund) and earns the same EPF interest rate

PF Interest Calculation Formula

PF interest is calculated monthly on the closing balance of your EPF account but credited to your account only once at the end of the financial year — on March 31.

The formula for PF interest calculation is:

Monthly Interest = (Closing Balance at end of month × Annual Interest Rate) ÷ 12

At 8.25% per year, the monthly PF interest rate = 8.25 ÷ 12 = 0.6875% per month

So every month, 0.6875% of your closing EPF balance is credited as interest — but you see it in your account only at the end of March.

You can watch above video to know more about calculations.

Also you can use the EPF calculator online to quickly check the interest calculation and maturity amount:

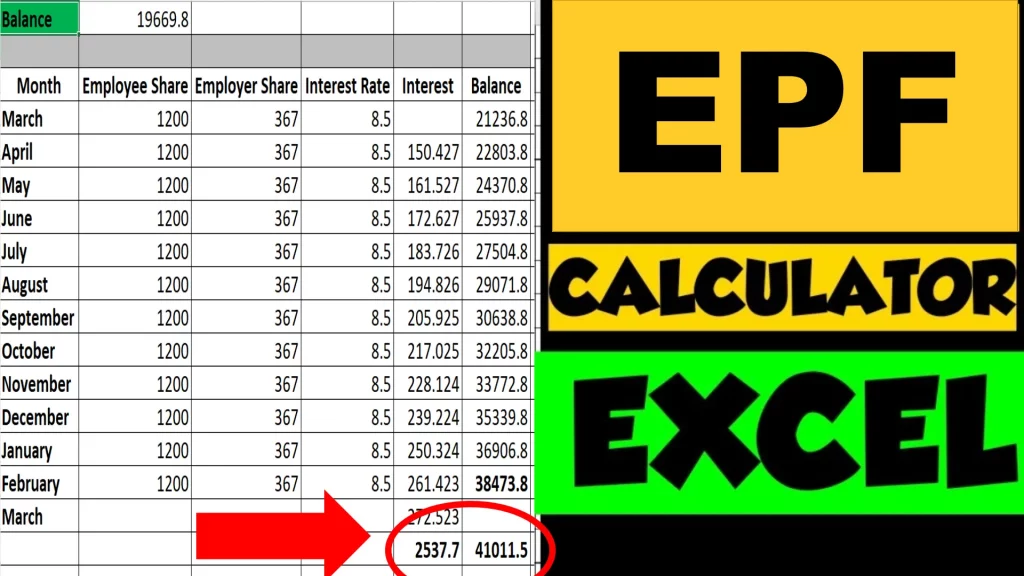

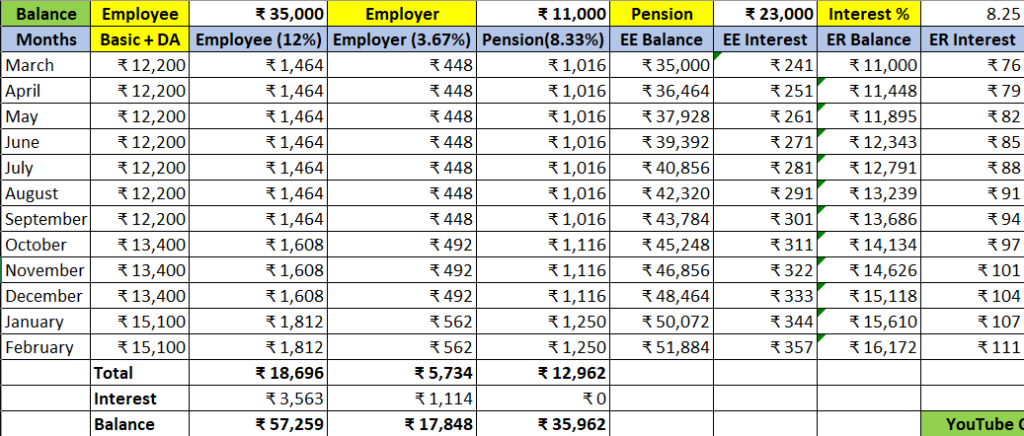

PF Interest Calculation – Step by Step Example

Let me walk you through a complete month-by-month PF interest calculation using the excel calculator at the top of this article

Assumption:

- Basic Salary + DA = Rs. 12,200 (Salary change in midway due to promotion or bonus)

- Employee contribution = 12% = Rs. 1,464 per month

- Employer EPF contribution = 3.67% on Rs. 12,200 = Rs. 448 per month

- Total monthly deposit = Rs. 1,912 (in EPF) and Rs. 1,016 (in EPS)

- Opening PF balance (April 1, 2025) = Rs. 35,000 (Employee) and Rs. 11,000 (Employer)

PF Interest Calculation Data – Month by Month:

- Interest keeps growing every month because your closing balance increases with each new deposit

- All 12 months of interest are added up and credited to your account in March 2026

- This is why your PF passbook may show no interest for most of the year — and then suddenly show a large credit in March or April

Total interest earned in FY 2025-26 (approximate) on Rs. 46,000 opening balance with Rs. 1,912 monthly contribution:

Approximately Rs. 4,600 for the full year — calculated by summing up 12 monthly interest amounts as your balance grows each month.

ALSO READ: SIP vs RD Calculator Which is Better

What is Your PF Balance – How to Check PF Balance

You do not need to wait for your annual PF statement to know your PF balance. EPFO provides multiple ways to check:

1. UMANG App — Download the UMANG app, log in with your UAN and check your PF balance instantly

2. SMS — Send a message from your registered mobile number: EPFOHO UAN ENG to 7738299899 — you will receive your PF balance by SMS

3. Missed Call — Give a missed call from your registered mobile number to 011-22901406 — EPFO will send you your PF balance details by SMS

4. EPFO Member Portal — Log in at member.epfindia.gov.in with your UAN and password to view your complete passbook including month-wise contribution and interest credit

5. DigiLocker — Your EPF passbook is also available on DigiLocker linked to your Aadhaar

- Make sure your UAN (Universal Account Number) is activated and your mobile number is registered with EPFO

- Your UAN is available on your salary slip — ask your HR if you have not received it

- If your Aadhaar, PAN and bank account are linked to your UAN, your PF passbook is fully accessible digitally

PF Withdrawal Rules – When and How Much Can You Withdraw

Most people think PF can only be withdrawn at retirement. That is not true. EPFO introduced significant updates to EPF withdrawal rules on October 13, 2025, aimed at simplifying procedures and increasing accessibility for over 7 crore subscribers.

Full PF Withdrawal – When is it Allowed:

- At retirement — on or after 58 years of age

- If you have been unemployed for 2 months or more — you can withdraw 100% of your EPF balance

Partial PF Withdrawal – Conditions and Limits:

Under the new EPFO rules, members can now withdraw up to 75% of their eligible EPF balance — including both employee and employer contributions — after 1 month of unemployment. The previous 13 reasons for partial withdrawal have been merged into three broad categories: essential needs such as illness, education and marriage; housing needs; and special circumstances.

| Purpose | Minimum Service | Withdrawal Limit |

|---|---|---|

| Medical Emergency | No minimum | Up to 6 months basic + DA or employee’s share, whichever is less |

| Marriage | 7 years | Up to 50% of employee’s share |

| Education | 7 years | Up to 50% of employee’s share |

| Home Purchase / Construction | 5 years | Up to 24 months basic + DA |

| Home Loan Repayment | 10 years | Up to 36 months basic + DA |

| Home Renovation | 5 years | Up to 12 months basic + DA |

- A minimum balance of 25% of total contributions must remain in the account to continue earning interest and grow the corpus

- Partial withdrawals can now be made after 12 months of service, standardised across all types — compared to up to 7 years earlier for certain withdrawal categories

Tax on PF Withdrawal – What You Need to Know

This is something many employees get wrong — not all PF withdrawals are tax-free.

- If you withdraw PF after 5 years of continuous service — the entire withdrawal including principal and interest is tax-free

- If you withdraw PF before 5 years — the withdrawal amount is added to your income and taxed as per your income tax slab

- No TDS is applicable if your withdrawal amount is less than Rs. 50,000. If it is more than Rs. 50,000 and you have PAN, TDS is deducted at 10%. If PAN is not submitted, TDS is at 30%.

- You can submit Form 15G (or 15H for senior citizens) to avoid TDS if your total income is below the taxable limit

Important: Changing jobs does not reset your 5-year clock — as long as you transfer your PF from the old employer to the new employer’s account using your UAN, the service is treated as continuous.

Is PF Interest Taxable?

This is one of the most asked questions — and the answer has changed in recent years.

- PF interest is tax-free up to a contribution of Rs. 2,50,000 per year by the employee

- Interest earned on employee contributions exceeding Rs. 2,50,000 in a financial year is taxable

- This rule was introduced from FY 2021-22 onwards to limit tax-free benefits for very high earners who were contributing large amounts to VPF

- For most salaried employees earning up to Rs. 15-20 Lakh, the 12% employee EPF contribution will be well within Rs. 2,50,000 — so the interest remains fully tax-free

- VPF contributions are included in the Rs. 2,50,000 limit — so high VPF contributors should be aware of this

PF vs PPF – Key Differences

Many readers confuse EPF and PPF. Let me clarify:

| EPF (Employee PF) | PPF (Public PF) | |

|---|---|---|

| Who can invest | Salaried employees only | Anyone |

| Interest Rate (FY 2025-26) | 8.25% | 7.1% |

| Contribution | Mandatory for salaried | Voluntary |

| Employer contribution | Yes | No |

| Lock-in | Till retirement (with conditions) | 15 years |

| Tax benefit | Section 80C — up to Rs. 1,50,000 | Section 80C — up to Rs. 1,50,000 |

| Tax on interest | Tax-free up to Rs. 2.5L contribution | Fully tax-free |

EPF is better than PPF on interest rate and because of employer contribution. PPF is open to everyone and has more flexible deposit options.

ALSO READ: Rs. 1000 to Rs. 12,000 PPF Interest Calculation for 15 Years

Frequently Asked Questions on PF Interest Calculation

What is the PF interest rate for FY 2025-26? The EPF interest rate for FY 2025-26 is 8.25% per annum. The monthly PF interest rate works out to 0.6875% per month.

When is PF interest credited to my account? PF interest is calculated monthly but credited to your account only once at the end of the financial year — in March or April. So your passbook may show no interest for most of the year and then a large credit in March.

How do I calculate my PF interest for the month? Multiply your closing EPF balance at the end of the month by 0.6875%. For example, if your EPF balance is Rs. 3,00,000, your interest for that month = Rs. 3,00,000 × 0.6875% = Rs. 2,062.50.

Can I withdraw my PF while I am still employed? No, you cannot withdraw full PF while employed. Partial withdrawal is allowed for specific purposes like medical emergency, home purchase, marriage or education — subject to minimum service conditions.

Does PF earn interest after I leave a job? Yes — your EPF account continues to earn interest even after you leave a job, for up to 3 years. After 3 years of no contributions, the account becomes inoperative and stops earning interest. Transfer your PF to your new employer or withdraw it to avoid this.

Is PF contribution tax deductible? Yes. Your employee contribution to EPF is eligible for deduction under Section 80C up to Rs. 1,50,000 per year.

Your PF account is silently working for you every month — earning guaranteed interest, growing with every salary increment, and building a retirement corpus you will one day be grateful for. The biggest mistake salaried employees make is withdrawing PF every time they change jobs. Even a single premature withdrawal can cost you lakhs in lost interest and tax-free compounding. Use the PF interest calculator above to see exactly how much your PF balance will grow over your remaining working years.

Save Home Loan Interest Amount!

Use Home Loan Excel Calculator that will help you to Save Interest Amount on Home Loan EMI.

Click below button to download Home Loan EMI and Prepayment Calculator in Excel:

Watch how Home Loan Calculator in Excel Works

Income Tax Calculator App – FinCalC

For Income Tax Calculation on your mobile device, you can Download my Android App “FinCalC” which I have developed for you to make your income tax calculation easy.

What you can do with this mobile App?

- Calculate Income Tax for FY 2025-26 and previous FY 2024-25

- Enter estimated Investments to check income tax with Old and New Tax Regime

- Save income tax details and track regularly

- Know how much to invest more to save income tax

- More calculators including PPF, SIP returns, Savings account interest and lot more

Use Popular Calculators:

- Income Tax Calculator

- Home Loan EMI Calculator

- SIP Calculator

- PPF Calculator

- HRA Calculator

- Step up SIP Calculator

- Savings Account Interest Calculator

- Lump sum Calculator

- FD Calculator

- RD Calculator

- Car Loan EMI Calculator

- Bike Loan EMI Calculator

- Sukanya Samriddhi Calculator

- Provident Fund Calculator

- Senior Citizen Savings Calculator

- NSC Calculator

- Monthly Income Scheme Calculator

- Mahila Samman Savings Calculator

- Systematic Withdrawal Calculator

- CAGR Calculator

I’d love to hear from you if you have any queries about Personal Finance and Money Management.

JOIN Telegram Group and stay updated with latest Personal Finance News and Topics.

Download our Free Android App – FinCalC to Calculate Income Tax and Interest on various small Saving Schemes in India including PPF, NSC, SIP and lot more.

Follow the Blog and Subscribe to YouTube Channel to stay updated about Personal Finance and Money Management topics.