Monthly Income Schemes help you to get passive income regularly to meet your expenses. What can be better when you can go for a vacation without having to worry about the cash flows or your income? The monthly income schemes work for you behind the scenes to cover for your expenses, while you are not actively working. Based on your age and risk appetite you can select the best suited scheme for yourself and reap the benefits of your investments.

The plan should be to accumulate funds during the initial stage of your career and making use of these funds to generate interest or returns over long term to become financially independent. Moreover, these schemes can also be used during your retirement phase as well, which can be before you reach 60 years of age.

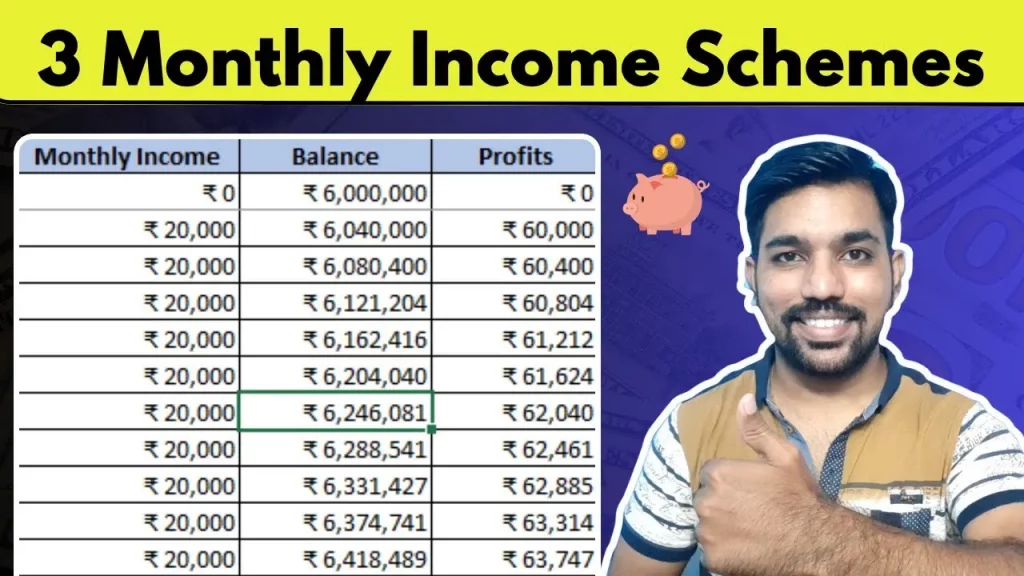

First, you can watch the video on these monthly income schemes that includes calculations using online and Excel Calculators

3 Monthly Income Schemes with Calculations [VIDEO]

Watch more Videos on YouTube Channel

Why Monthly Income Schemes are Essential for Financial Stability

In today’s dynamic economic landscape, creating and maintaining diverse income streams is more crucial than ever. Monthly income schemes offer a reliable way to supplement your primary earnings or provide a consistent income during retirement. They are designed to give you regular payouts, ensuring financial stability and peace of mind. We will see 3 monthly income schemes in this blog including, Post Office Monthly Income Scheme (POMIS), Senior Citizen Saving Scheme (SCSS) and Systematic Withdrawal Plan (SWP) and compare them to meet your needs.

Exploring the Top 3 Monthly Income Schemes

Let’s now understand the features and benefits of these monthly income schemes that can provide you regular payout.

1. Post Office Monthly Income Scheme (POMIS)

- Overview: A government-backed scheme, POMIS is a popular choice for risk-averse investors seeking guaranteed returns.

- Key Features:

- Tenure: 5 years

- Minimum Deposit: ₹1,000

- Maximum Deposit: Up to ₹9 lakhs for a single account and ₹15 lakhs for a joint account.

- Interest Rate: Currently offers 7.4% per annum, with interest paid out monthly. Interest rate is subjected to change on quarterly basis

- Premature Closure: Allowed, but with certain penalties.

- Principal Return: The entire deposited amount is returned to the investor upon maturity after 5 years.

- Returns: The returns or interest is calculated on monthly basis based on the interest rate set for that quarter

- Example Returns:

- A ₹1 lakh deposit can yield approximately ₹617 monthly income.

- A single account with the maximum ₹9 lakh deposit can provide ₹5,550 monthly.

- A joint account with ₹15 lakh deposit can generate ₹9,250 per month.

- Suitability: Ideal for individuals looking for a low-risk, steady monthly income with capital protection.

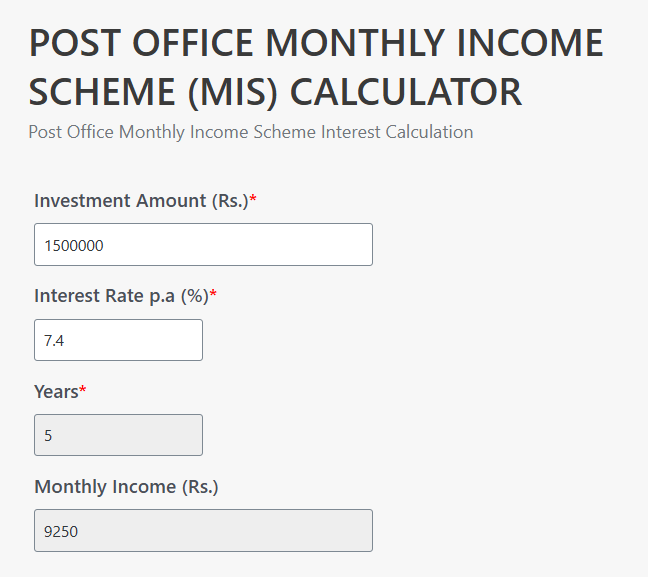

Below is the calculation using Post Office MIS Calculator:

2. Senior Citizen Savings Scheme (SCSS)

- Overview: Specifically designed for senior citizens, SCSS offers attractive interest rates and tax benefits.

- Key Features:

- Target Audience: Exclusively for senior citizens.

- Tenure: 5 years, with an option to extend for another 3 years upon maturity.

- Minimum Deposit: ₹1,000.

- Maximum Deposit: Up to ₹30 lakhs.

- Interest Rate: Offers a higher interest rate of 8.2% per annum, paid quarterly.

- Tax Benefits: Investments qualify for deductions under Section 80C of the Income Tax Act, up to ₹1.5 lakhs.

- Premature Closure: Permitted with penalties.

- Example Returns:

- A ₹1 lakh deposit yields ₹2,050 quarterly interest.

- A ₹5 lakh deposit can provide ₹10,250 quarterly.

- With the maximum ₹30 lakh deposit, you could receive ₹61,500 quarterly, translating to approximately ₹20,500 per month.

- Suitability: Highly recommended for senior citizens seeking regular income with attractive returns and tax advantages.

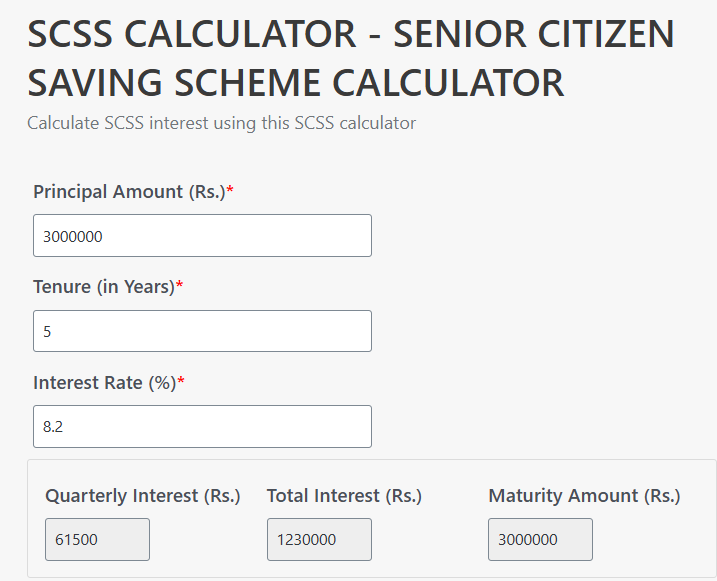

Below is the calculation done using SCSS Calculator

3. Systematic Withdrawal Plan (SWP)

- Overview: SWP is a flexible, market-linked option that involves withdrawing a fixed amount from your mutual fund investments. The returns are volatile since they are linked to market returns.

- Key Features:

- Type: An investment strategy within mutual funds.

- Withdrawal Frequency: Allows you to set up regular (e.g., monthly) withdrawals from your mutual fund corpus.

- Returns Potential: Offers potentially high returns over the long term, making it suitable for wealth creation and retirement planning.

- Flexibility: You can choose the withdrawal amount and frequency, and the remaining corpus continues to grow.

- Strategic Recommendation: You can Start a Systematic Investment Plan (SIP) in mutual funds during your earning years to build a substantial corpus. Once accumulated, this corpus can then be used for SWP to generate passive income.

- Example Returns (based on a 12% expected rate of return and 4% inflation):

- An initial investment of ₹50 lakhs with a monthly withdrawal of ₹20,000 can result in significant wealth appreciation. After 5 years, you could have withdrawn ₹12 lakhs, with the remaining balance potentially growing to around ₹59.79 lakhs.

- Even with a higher monthly withdrawal of ₹30,000, the remaining balance can still exceed the initial investment if the investment profits outpace withdrawals.

- Suitability: Best for investors comfortable with market fluctuations, seeking long-term growth and a flexible income stream during retirement.

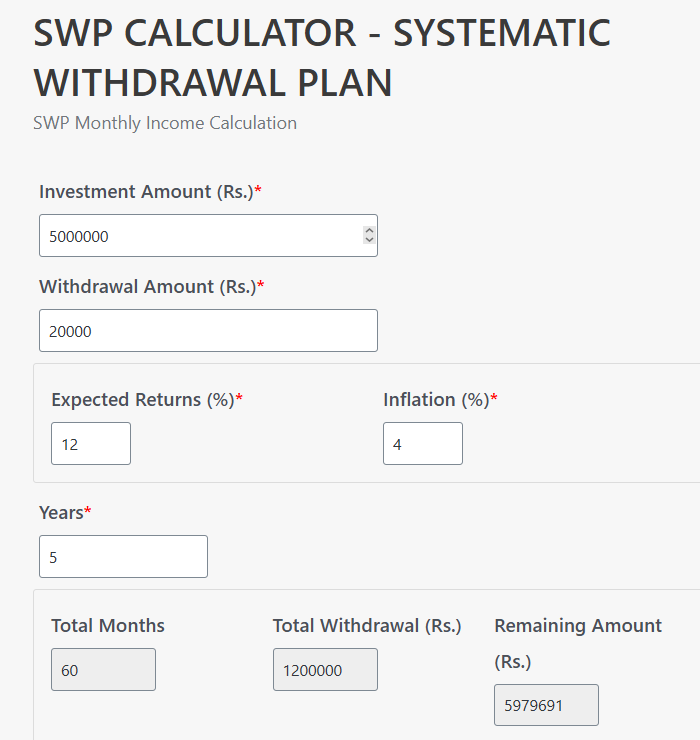

Below is the monthly withdrawal calculation using SWP Calculator:

Let us now compare above discussed monthly income schemes and decide which is better for you?

Post Office MIS vs Senior Citizen Saving Scheme (SCSS) vs Systematic Withdrawal Plan (SWP)

| Feature | Post Office Monthly Income Scheme (POMIS) | Senior Citizen Savings Scheme (SCSS) | Systematic Withdrawal Plan (SWP) |

| Risk Level | Low (Government-backed) | Low (Government-backed) | Moderate to High (Market-linked) |

| Target Audience | General Investors | Senior Citizens | All Investors (especially for retirement planning) |

| Interest Rate/Returns | Fixed (7.4% p.a.) | Fixed (8.2% p.a.) | Variable (Market-linked, potentially higher long-term) |

| Income Frequency | Monthly | Quarterly | Flexible (typically monthly) |

| Tax Benefits | No direct 80C benefits | Yes (Under Section 80C) | Taxation based on mutual fund type (equity/debt) |

| Flexibility | Low (Fixed tenure, penalties for early exit) | Low (Fixed tenure, penalties for early exit) | High (Flexible withdrawals, corpus continues to grow) |

| Growth Potential | Principal returned | Principal returned | High (Corpus grows with market performance) |

ALSO READ: Types of Mutual Funds in India

Making Your Choice: Key Considerations

When choosing a monthly income scheme, consider your:

- Risk Appetite: Are you comfortable with market fluctuations (SWP) or do you prefer guaranteed returns (POMIS, SCSS)?

- Age and Eligibility: SCSS is specifically for senior citizens. Other 2 schemes can be selected by non senior citizens considering the risk taking ability

- Liquidity Needs: How frequently do you need the income, and do you foresee needing access to your principal before maturity? SWP from mutual funds needs a longer duration initially until you reach a substantial amount, before starting the withdrawal process.

- Tax Implications: Evaluate the tax benefits and liabilities associated with each scheme. With new tax regime, no income tax need to e paid up to 12 lakh taxable income from FY 2025-26 onwards, and also the tax slab rates are low compared to old tax regime.

- Long-Term Goals: Are you looking for steady income or wealth appreciation? For stable guaranteed income MIS is better, for wealth appreciation, SWP is better.

By carefully assessing these factors, you can select the monthly income scheme that best aligns with your financial objectives and helps you achieve your passive income goals.

For more detailed information and financial planning insights, consider watching the full video on FinCalC TV posted at the start of this article.

Some more Reading: