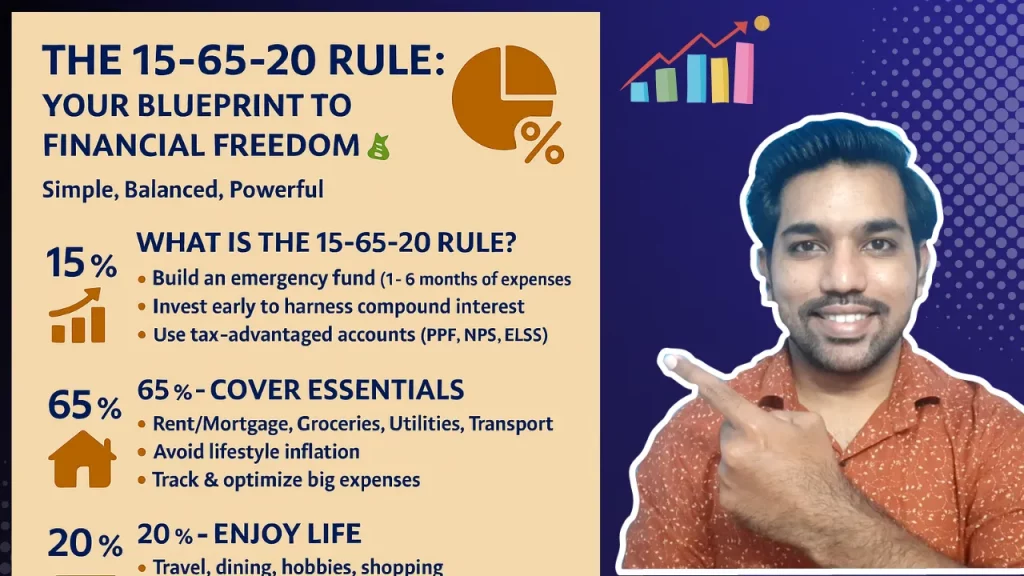

In today’s complex financial landscape, managing your money effectively can feel like an uphill battle. Many aspire to financial security and growth, but few truly understand the strategies employed by the financially savvy. This blog post delves into the revolutionary “15-65-20 rule,” a robust financial management approach inspired by the habits of high-net-worth individuals. The 15-65-20 Rule for Financial Freedom isn’t just about budgeting; it’s a holistic framework designed to empower you to manage your money like a true financial expert, paving the way for long-term security, sustainable living, and guilt-free enjoyment.

15% for Yourself: Building Long-Term Security and Growth

This initial 15% of your income is perhaps the most crucial, as it’s dedicated to securing your future and making your money work for you. This portion is divided into two vital components: building a peace-of-mind emergency fund and strategic investing.

1. The Emergency Fund: Your Financial Safety Net

Life is unpredictable, and unexpected expenses can derail even the most religiously planned budgets. A robust emergency fund acts as your financial safety net, providing a cash cushion for unforeseen events like car repairs, medical emergencies, or sudden job loss. The journey to building this fund should begin with a manageable goal: accumulating one month’s worth of essential expenses. This initial step provides immediate relief and a sense of security.

From there, the aim is to gradually increase your emergency savings to cover three to six months of your core living costs – this includes rent or mortgage, groceries, transportation, and utilities, excluding discretionary spending.

Having a well-funded emergency reserve offers immense peace of mind. It prevents you from taking high-interest debt during crises, allowing you to focus on resolving the emergency itself rather than struggling with financial stress. This proactive approach to financial resilience is a hallmark of sound money management and a foundational pillar of the 15-65-20 system.

It’s not just about having money set aside; it’s about the freedom and reduced anxiety that comes with knowing you’re prepared for whatever life throws your way.

ALSO READ: 5 steps to build a Strong Emergency Fund

2. Making Your Money Work for You: The Power of Investing

Beyond the emergency fund, the remainder of your 15% is dedicated to investing, leveraging the incredible power of compound interest. The earlier you start investing, the more time your money has to grow exponentially. Consider the hypothetical scenario of Rahul and Rishab:

| Investor | Starting Age | Initial Investment | Monthly Contribution | Investment Period | Final Value (Illustrative) |

| Rahul | 25 | Rs. 5,000 | Rs. 2000 | 40 years | Rs. 2.38 Crore |

| Rishab | 35 | Rs. 5,000 | Rs. 2000 | 30 years | Rs. 70.8 Lakh |

As this simplified example illustrates, starting earlier, even with modest contributions, can lead to dramatically different outcomes due to the compounding effect.

Key Investment Avenues:

- Workplace Retirement Plans (e.g., EPF, NPS): These plans are often the easiest and most effective way to kickstart your investment journey. Your employer offers a match for the EPF and EPS contributions with your 12% monthly basic pay component, which makes such schemes more attractive. They also help in saving income tax with old and new tax regimes

- Simple Investment Strategy: For most individuals, a complex investment strategy is unnecessary and often counterproductive. The recommended approach is to keep it simple: invest in low-cost, passive funds that track the overall stock market. These are called Index Mutual Funds, in which a simple SIP of Rs. 1000 can be started for a long term, while your other workplace investments are working for you along with your active income.

ALSO READ: How EPF can help you Retire Early

65% for Fundamental Expenses: Keeping Core Living Costs in Check

The largest portion of your income, 65%, is allocated to fundamental expenses – your core living costs. This includes essentials such as rent or mortgage payments, groceries, utilities, and transportation. While this category covers your basic needs, it’s also where “lifestyle creep” can impact your financial progress. Lifestyle creep occurs when your expenses increase proportionally with your income, preventing you from saving or investing more.

To effectively manage this 65%, it’s crucial to regularly analyze your current spending habits. Large categories like housing and transportation often present the biggest opportunities for optimization. In many regions, housing can account for a significant portion of monthly expenditure (e.g., 40% in India), followed by transportation (e.g., 14%).

Strategies for Optimizing Fundamental Expenses:

- Housing: Explore options like negotiating rent, refinancing your mortgage (if applicable), or considering more affordable living arrangements if your current housing costs are disproportionately high

- Transportation: Look into carpooling, public transport, cycling, or even walking if feasible. Evaluate your car insurance and fuel consumption.

- Groceries: Meal planning, buying in bulk, and reducing food waste can significantly cut down on grocery bills.

- Utilities: Be mindful of energy consumption, consider energy-efficient appliances, and shop around for better utility rates.

The goal isn’t to live a life of deprivation, but to consciously manage these essential costs to create more breathing room in your budget. By setting a firm 65% limit, you maintain discipline and ensure that your core expenses don’t consume too much of your income, freeing up funds for your long-term goals and personal enjoyment.

20% for Fun, Enjoyment, and Personal Fulfillment: Living a Rich Life

Inspired by philosophies like “Die with Zero,” the final 20% of your income is dedicated to guilt-free spending on activities and experiences that bring you joy and personal fulfillment. This portion is not an indulgence; it’s a strategic investment in your well-being and a critical component of sustainable financial management.

Many traditional budgeting methods can feel restrictive, leading to a sense of deprivation and ultimately, burnout. By intentionally allocating funds for enjoyment, the 15-65-20 system helps prevent this. It acknowledges that a balanced life, incorporating leisure and personal interests, is essential for long-term adherence to financial goals. When you know you have a dedicated fund for fun, you’re less likely to feel deprived and more likely to stick to your overall financial plan.

Examples of Guilt-Free Spending:

- Treating yourself to nice dinners at your favorite restaurants.

- Purchasing desired items that enhance your life.

- Enjoying fun getaways or experiences with friends and loved ones.

- Pursuing hobbies or personal development courses

This 20% is about living a rich and fulfilling life now, without compromising your future. It promotes motivation, balance, and the energy needed to consistently adhere to your long-term financial plans. It’s a recognition that money is a tool for living, not just for saving.

ALSO READ: Bad Money Habits you Should Avoid

Why the 15-65-20 System Works

At its heart, the 15-65-20 system is about intentional allocation and mindful spending. It recognizes that financial well-being isn’t solely about saving every penny, but about strategically distributing your income to meet various needs: securing your future, covering essential living costs, and enriching your present.

This balanced approach helps prevent burnout often associated with overly restrictive budgets and promotes a sustainable path to financial success. By breaking down your income into three distinct categories, the system provides clarity, control, and a clear roadmap for your financial journey.

It’s a departure from traditional, often rigid, budgeting methods, offering flexibility while maintaining discipline. The system’s effectiveness lies in its simplicity and its focus on long-term financial health, mirroring the disciplined yet balanced approach seen in those who have achieved significant wealth.

Implementing the 15-65-20 System: Practical Steps

Transitioning to the 15-65-20 system requires a clear understanding of your current financial situation and a commitment to intentional change.

- Calculate Your Net Income: Start by determining your net income after taxes and deductions. This is the base figure for your allocations.

- Track Your Spending: For a month or two, meticulously track every penny you spend. This will give you a realistic picture of where your money is currently going and highlight areas for adjustment.

- Allocate Your Percentages:

- 15% to Savings/Investments: Set up automated transfers to your emergency fund and investment accounts immediately after you get paid. This “pay yourself first” strategy ensures you prioritize your future.

- 65% to Fundamental Expenses: Review your tracked spending and adjust your budget to fit within this 65% limit. Look for areas to optimize, especially in housing and transportation.

- 20% to Fun/Discretionary Spending: Create a separate fund or mental allocation for this portion. This is your guilt-free spending money.

- Automate and Monitor: Automate as many of your savings and bill payments as possible. Regularly review your spending to ensure you’re sticking to your allocations and make adjustments as needed.

- Be Patient and Flexible: Financial management is a journey, not a destination. There will be months where you might slightly deviate. The key is to be consistent over time and adjust the system to fit your unique circumstances while staying true to its core principles.

ALSO READ: Early Retirement in India with Rs. 1 Crore

Comparison: 15-65-20 System vs. Other Budgeting Methods

To further illustrate the benefits of the 15-65-20 system, let’s briefly compare it to some other popular budgeting approaches:

| Feature | 15-65-20 System | 50/30/20 Rule | Zero-Based Budgeting | Envelope System |

| Allocation | 15% Savings/Investments, 65% Needs, 20% Wants | 50% Needs, 30% Wants, 20% Savings/Debt Repayment | Every rupee assigned a job | Physical cash allocated to categories |

| Flexibility | High (within categories) | Moderate | Low (requires strict tracking) | Low (cash-based, less digital friendly) |

| Focus | Long-term security, sustainable living, enjoyment | Balancing needs, wants, and savings | Maximizing every dollar, preventing overspending | Visualizing spending, preventing overspending |

| Complexity | Low to Moderate | Low | High (detailed tracking required) | Moderate (physical management) |

| Key Advantage | Holistic, balanced, promotes guilt-free spending | Simple, easy to understand | Ensures no money is wasted | Prevents overspending in specific categories |

| Best For | Those seeking balanced financial growth and enjoyment | Beginners, those needing a simple framework | Disciplined individuals, debt repayment focus | Visual learners, those prone to overspending |

The 15-65-20 system stands out for its emphasis on intentional enjoyment while still prioritizing long-term growth and essential expenses. It offers a more better approach than simpler rules and more flexibility than highly detailed methods, making it adaptable for a wide range of financial situations.

FAQ Section: Your Questions Answered

What if my current expenses don’t fit the 65% for fundamental expenses?

This is a common challenge. The first step is to track your spending to identify where your money is going. Then, look for areas to optimize. This might involve negotiating bills, finding more affordable housing or transportation, or reducing discretionary spending in other areas until you can adjust your core expenses to fit the 65% target. It’s a process, and it might take time to realign.

Can I adjust the percentages in the 15-65-20 system?

While the 15-65-20 percentages are a recommended guideline, they serve as a starting point. The core philosophy is about intentional allocation. If your unique financial situation (e.g., high debt, specific short-term goals) requires a temporary shift (e.g., more towards debt repayment, less towards fun), you can adjust. However, always strive to return to or approximate the recommended percentages for long-term balance.

How often should I review my budget using this system?

It’s advisable to review your budget at least monthly or quarterly to ensure you’re on track. A more in-depth review quarterly or semi-annually can help you assess your progress towards long-term goals and make any necessary adjustments based on changes in income or expenses.

What kind of investments should I focus on for the 15%?

For most individuals, focusing on low-cost, diversified index funds or exchange-traded funds (ETFs) that track the overall market is an excellent strategy. These offer broad market exposure with minimal fees. Prioritize tax-advantaged accounts like workplace retirement plans (especially if there’s an employer match) and individual retirement accounts (IRAs) first.

Is the “20% for fun” truly guilt-free?

Yes, that’s the whole point! By intentionally allocating this portion of your income for enjoyment, you remove the guilt often associated with discretionary spending. It’s an investment in your well-being and motivation, ensuring you don’t feel deprived and are more likely to stick to your overall financial plan.

Conclusion

The 15-65-20 rule offers a refreshing and effective approach to personal finance. By strategically allocating your income into three distinct categories – 15% for long-term security and growth, 65% for fundamental expenses, and 20% for guilt-free enjoyment – you can build a robust financial foundation while still living a fulfilling life.

This system empowers you to take control of your money, move beyond mere budgeting, and adopt the disciplined yet balanced habits of those who truly excel in financial management. Embrace the 15-65-20 system, and unlock your potential for lasting financial freedom and peace of mind.

Some more Reading;

- Buy vs Rent a House in India with excel calculator

- SWP Calculation with Inflation for Monthly Income

- Home Loan Part Payments with Examples

Save Home Loan Interest Amount!

Use Home Loan Excel Calculator that will help you to Save Interest Amount on Home Loan EMI.

Click below button to download Home Loan EMI and Prepayment Calculator in Excel:

Watch how Home Loan Calculator in Excel Works

Income Tax Calculator App – FinCalC

For Income Tax Calculation on your mobile device, you can Download my Android App “FinCalC” which I have developed for you to make your income tax calculation easy.

What you can do with this mobile App?

- Calculate Income Tax for FY 2025-26 and previous FY 2024-25

- Enter estimated Investments to check income tax with Old and New Tax Regime

- Save income tax details and track regularly

- Know how much to invest more to save income tax

- More calculators including PPF, SIP returns, Savings account interest and lot more

Use Popular Calculators:

- Income Tax Calculator

- Home Loan EMI Calculator

- SIP Calculator

- PPF Calculator

- HRA Calculator

- Step up SIP Calculator

- Savings Account Interest Calculator

- Lump sum Calculator

- FD Calculator

- RD Calculator

- Car Loan EMI Calculator

- Bike Loan EMI Calculator

- Sukanya Samriddhi Calculator

- Provident Fund Calculator

- Senior Citizen Savings Calculator

- NSC Calculator

- Monthly Income Scheme Calculator

- Mahila Samman Savings Calculator

- Systematic Withdrawal Calculator

- CAGR Calculator

I’d love to hear from you if you have any queries about Personal Finance and Money Management.

JOIN Telegram Group and stay updated with latest Personal Finance News and Topics.

Download our Free Android App – FinCalC to Calculate Income Tax and Interest on various small Saving Schemes in India including PPF, NSC, SIP and lot more.

Follow the Blog and Subscribe to YouTube Channel to stay updated about Personal Finance and Money Management topics.