What is Fund of Funds in Mutual Funds?

Fund of Funds in Mutual Funds is type of mutual fund that invest in other Mutual Funds. They diversify your investments across asset classes

Fund of Funds in Mutual Funds is type of mutual fund that invest in other Mutual Funds. They diversify your investments across asset classes

Ideal Portfolio of Mutual Funds.. Diversification with a mix of Equity Mutual Funds & Debt Mutual Funds can help achieve your Financial Goals

Index Funds in India are the type of Mutual funds that tries to mimic the indices such as BSE Sensex & NSE Nifty 50. Low Cost & Good Returns

Sector and Thematic Mutual funds are the type of Equity mutual funds that invest in specific sector or theme, high risk and less diversified

Life Term Insurance is simplest Life Insurance that provides Financial coverage to your family after your sudden death to pay for debts / expenses..

What is Life Term Insurance Plan, Benefits and Eligibility Read More »

Interval Fund is similar to Fixed Maturity Plan (FMP) mutual fund that is illiquid in nature with high fees and decent returns compared to debt funds..

NFO in Mutual Fund or New fund offer is a way of collecting funds by fund house to start a new mutual fund to accumulate wealth for investors

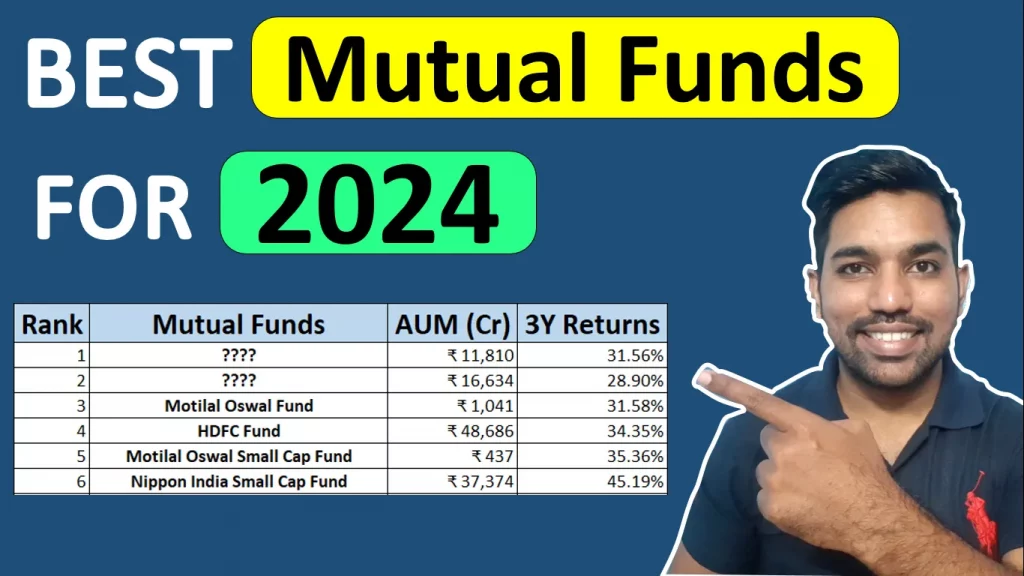

Best Mutual Funds for 2024 for your long term goals and high returns, SIP is the best way to invest in these Mutual Funds..

NAV in Mutual Fund.. NAV full form is Net Asset Value which is price of single unit of mutual fund. NAV is used to calculate fund units..

What is NAV in Mutual Fund? Net Asset Value Calculation Read More »

Main Difference between open ended and closed ended mutual funds is liquidity and the way we invest in these mutual funds..

Difference between Open Ended and Closed Ended Mutual Funds Read More »